Written by Matthew Westaway, CEO, Voyc

The Clock is Ticking…

The new Consumer Duty has raised demanding expectations for UK financial services businesses of all types – including IFAs.

By October last year, firms should have completed their implementation plans for compliance with the new rules. And the countdown is now well underway to the full implementation deadlines:

31st July 2023: for all existing and new products

31st July 2024: for products and services held in closed books

A recent review by the FCA showed that while firms are making good progress, there are many areas in which improvement is still needed before the deadlines.

What’s more, as a regulated firm, you’re required not only to follow the new rules covered by the Consumer Duty but also to provide clear evidence of compliance when the FCA asks for it.

Delivering good outcomes across 100% of your customer interactions

The Consumer Duty is based fundamentally on a new Consumer Principle that requires firms to: “act to deliver good outcomes for retail customers”.

The Duty specifies four outcome areas. All of these are highly relevant to the direct interactions that IFAs have with consumers – by phone, email and face-to-face.

At Voyc, we’ve compiled a series of tips that you can use to help ensure delivery within each of these outcomes in a way that also gives you solid evidence of compliance as and when you need it…

Outcome 1: Products and Services

The products and services offered by the firm should be designed to deliver benefits that suit the needs of the particular target markets they’re offered to.

Tip 1: Use open-ended questions to ensure (and can demonstrate) that you clearly understand the particular product or service needs of the individual customer.

“Drill down” with additional questions to arrive at the sharpest needs picture you can. As an example, if the customer says: “I want a savings plan”, keep going until you

get to the real need the customer feels: “I want to put aside regular amounts to deliver a valuable lump sum to my new grandchild on their 18th birthday in February 2041 – and I am happy to take a considerable share of investment risk”.

Of course, this step is very much in line with the rigorous fact-find process that all IFAs are fully familiar with. But it’s critical also to ensure that the specific need is identified for evidence purposes if needed under the Consumer Duty.

Outcome 2: Price and Value

Beyond requiring that products and services meet the needs of the firm’s specific target markets, the Consumer Duty expects firms to ensure that customers receive good value in relation to the costs involved.

Tip 2: Assess price and value in every aspect of the product or service delivery – based on the individual customer’s needs.

Taking the previous scenario of the child savings plan further – does the product offered deliver the best potential return over the required period, taking proper account of the customer’s investment risk and personal preferences? For example, the best value for this particular customer might involve higher charges than an alternative, cheaper, product that offers online servicing only – because this particular customer needs telephone or even in-branch support, due to their level of digital skill.

Outcome 3: Customer Understanding

It’s vitally important to the purpose of the Consumer Duty that customers fully understand the products and services that are offered to them. This includes not only the product benefits, but also important factors such as the duration of the contract, the risks involved, any penalties for missed payments or early exit, and the exclusions that might apply.

Tip 3: Ask the customer to confirm their understanding – and make sure their understanding is correct.

Under the Consumer Duty, a valuable habit is to ask every customer to restate in their own words the features of the product or service offered relating to their own specific needs. Ensure that they clearly confirm their understanding of the match between their personal needs and the benefits of the product or service.

In the same way, use open-ended questions to verify that they understand the risks and potential disadvantages that the product or service represents for them.

Outcome 4: Customer Support

The Consumer Duty requires every regulated form to support customers with levels of service and access that deliver good outcomes for them – taking account of their

circumstances and needs. This demands close attention to the particular characteristics of each firm’s target markets.

Many regulated firms serve customer groups with characteristics of vulnerability and the Consumer Duty gives special and repeated emphasis to delivering good outcomes for these groups.

It’s important for firms interacting with individual customers to have evidence of the steps they take to identify vulnerability and to respond accordingly, depending on need. The TEXAS approach is a proven way to help with this.

Tip 4: Use the TEXAS approach to understand and support customer vulnerability.

The TEXAS approach begins when the customer trusts the advisor sufficiently to disclose personal vulnerability – such as a physical impairment or, for example, a lack of confidence in handling financial matters.

At this point, the adviser follows the TEXAS sequence:

1. Thank the customer for disclosing information that will support a better outcome for them.

2. Explain how the information will be used and who it will be shared with.

3. Request their eXplicit consent to record the information and use it to deliver a good outcome for them.

4. Ask any reasonable additional questions about their situation that will help ensure the best outcome for them. For example: do they wish to involve a family member or anybody else in the decision? Do they require documentation in large print?

5. Signpost Support by offering information on any relevant sources of help such as debt counselling, bereavement services or, if appropriate, Samaritans.

Understanding and taking full account of customer vulnerability is a major and growing priority for financial services firms and also for us at Voyc. Our popular white paper on Vulnerable Customers provides extensive insight into this important topic.

Other important requirements for customer interactions

In addition to the four outcomes I’ve discussed above, the Consumer Duty details two key areas that it requires firms to prioritise. At Voyc, we refer to these as the Consumer Duty control functions:

Control Function 1: Culture and Governance.

The FCA wants every regulated firm to embrace the Consumer Duty fully at the highest level and throughout all operating areas.

The Duty requires all firms to foster an open culture that consistently supports good customer outcomes and empowers all individual staff members to contribute to that culture at all times.

Tip 5: Facilitate open dialogue between customer-facing team members on the customer interactions they handle and encourage collaboration on ways to improve outcomes consistently.

Taking these actions will undoubtedly involve a major cultural shift in many financial services firms – but it is essential to deliver the full purpose of the Consumer Duty.

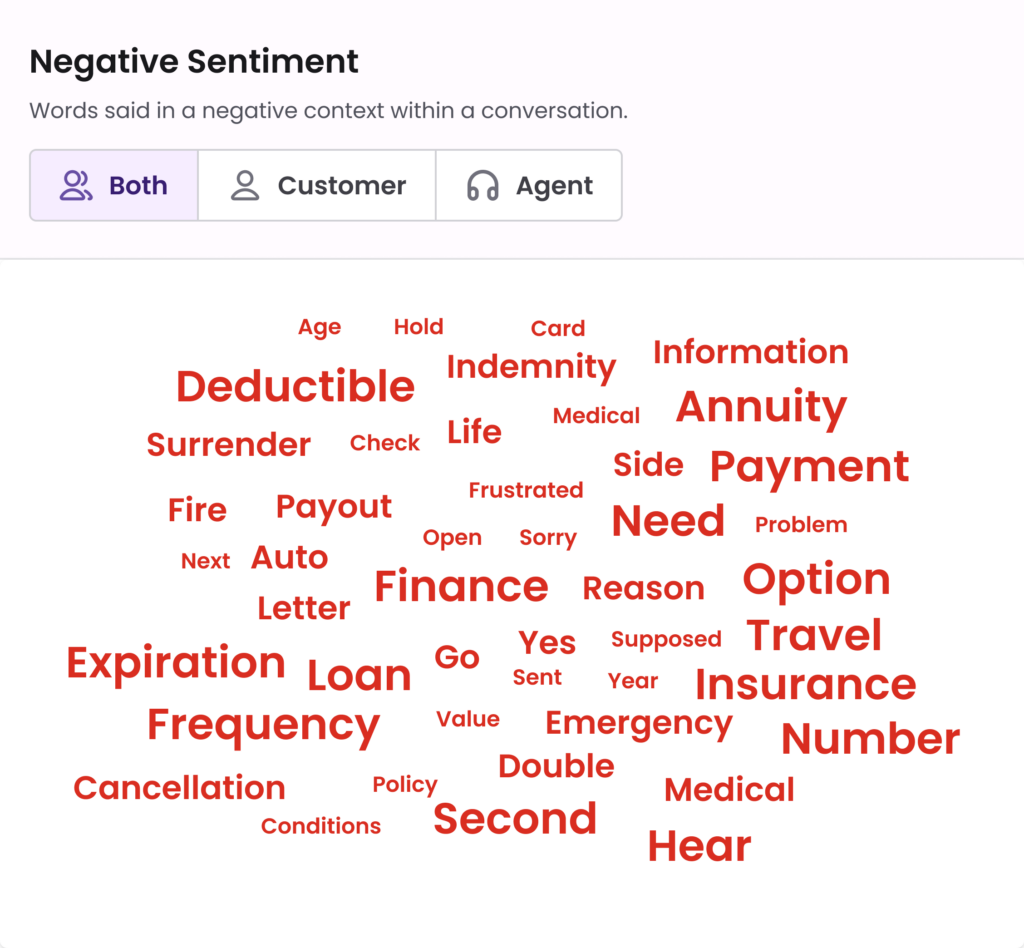

At Voyc, we’ve found that generating word clouds based on the phrases frequently used in customer conversations can stimulate lively and productive participation and ideas.

Control Function 2: Monitoring Outcomes

The need for effective monitoring applies to everything I’ve covered in this article – and it is emphasised throughout the Consumer Duty.

Tip 6: Ensure that robust processes and systems are in place to monitor customer interactions for compliance and quality across the four Consumer Duty outcomes at all times.

This may be through Quality Assurance teams physically auditing call recordings and other interactions – or enhanced to 100% monitoring levels using an advanced software solution. What’s essential is that firms must monitor their interactions in a way that drives good outcomes – and in a way that can be clearly evidenced as required.