Crowdfunding is a fast-growing sector and Julia Groves, Head of Crowdfunding at Downing, believes advisers shouldn’t be missing out.

When Nesta published the UK Alternative Finance Industry Report earlier this year, it detailed some impressive statistics. During 2015, the crowdfunding market grew to £3.2 billion in size, involving more people, projects and businesses in funding and fundraising – the popularity of joining ‘the crowd’ appeared infectious. The number of funders in the UK reached 1.09 million with some 254,721 individuals, projects, not-for-profits and businesses raising finance via online alternative finance platforms. The market has continued to grow in 2016 and we believe it is now too big for advisers to ignore, which begs the question – is there a place for intermediaries to give advice and possibly add value to client portfolios via crowdfunding?

Not all crowdfunding is the same

Crowdfunding typically finances projects or businesses by raising contributions from direct investors via an online platform. In return, investors can receive shares in a company or earn interest. It is a very diverse market ranging from equity-based crowdfunding, which is similar to angel investing, all the way through to secured bonds, which are possibly transferable and asset-backed. Much of the UK crowdfunding market has now moved towards debt-based crowdfunding, lending to more mature businesses with established revenue streams; in 2015, the vast majority of the UK market at 88% was debt-based, and almost £1.49 billion was loaned to UK SMEs via peer-to–peer (P2P) business lending.

As a long-standing supporter of UK businesses, a natural progression for Downing has been to move into the debt-based crowdfunding market. We launched our crowdfunding platform in March, offering bonds secured on a business’ existing, operational assets. Over the six months since March, we have launched a further six bonds. We are delighted to have raised over £12 million to support the growth of smaller UK businesses, predominantly in the renewable energy space. To date the bonds issued have offered between 5% and 7% returns over 1-2 year terms and have attracted more than 700 investors.

Key considerations around a crowdfunding investment

There is no such thing as a ‘typical’ crowdfunding investor given the scope of the sector and the variation in the risks associated with each specific crowdfunding raise. There is a world of difference between an investment in an early stage business that has yet to prove it can generate revenue (never mind profit) and an investment in mature, established or asset-backed businesses. With any fundraise, there are some key questions that need to be answered:

- Where is the money raised going – is it going to a person or a company?

- How well established is the company, and what is the risk associated with the actual end asset?

- What type of vehicle is being used – is it equity or a bond, secured or unsecured, junior or senior debt?

- And what happens if things go wrong?

Finally, the platform it sits on and what that platform does to protect investors needs to be explored. Whether they are acting as security trustees or agents needs to be established, along with the level of due diligence that has been carried out on the company.

For example, each bond on the Downing Crowd platform goes through Downing’s full due diligence process, drawing on over 20 years of investment management experience. A full Offer Document is issued for each fundraise, outlining the risk and returns and independent analysis is available through an in:review report.

So, is crowdfunding advisable?

Despite the compelling attraction of certain types of crowdfunding, it has not traditionally been considered advisable for a number of reasons, not least because of scepticism of the quality of the offers/valuations, issues with regulation and permissions. However, we are seeing an increasing number of enquiries from advisers interested in the opportunities for their clients, which suggests the tide is turning on how intermediaries view of this area of the alternative finance market.

We believe that the key challenges for advisers are evaluating each client’s overall portfolio and appetite for risk, understanding the crowdfunding opportunities available and the levels of risk involved, and then assessing whether the returns are sufficiently acceptable for the level of risk taken.

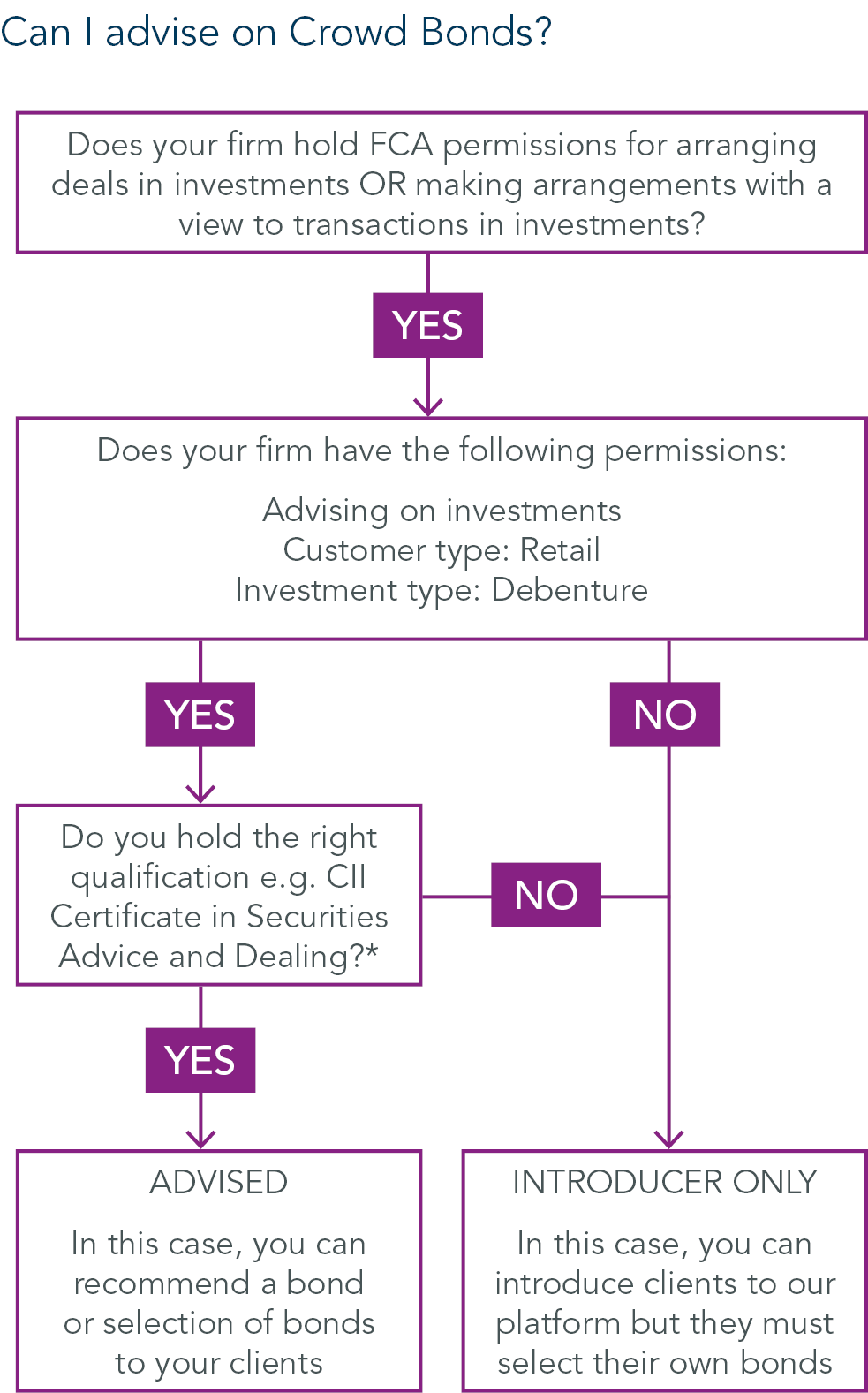

Debt-based crowdfunding is regulated by the FCA, which gives a further layer of investor protection. So as long as firms have the correct permissions to advise on these investments and advisers have the appropriate qualifications (see below), they are permitted to give advice on these opportunities.

A valuable addition to a balanced portfolio

Severe fluctuations in financial markets following the global financial crisis, and more recently following the Brexit vote, have resulted in a low interest rate environment that shows no sign of improving in the short term. This has had a significant influence on how investors and providers consider different investment solutions. Diversification within a balanced portfolio is the holy grail for most investors – so a valuable addition to their mainstream holdings could be an investment in an unlisted, mature company with established assets and cash flows. As such, an uncorrelated portfolio might contain investments that are unlisted and therefore not exposed directly to the highs and lows of the stock market.

Legislation and widening parameters of the IFISA and pension freedoms

The new Innovative Finance ISA (IFISA), introduced in April this year, offers an opportunity for advisers to introduce clients to the diversification benefits of crowdfunding. Draft legislation on widening the parameters of the new IFISA has been published revealing that, from November, investors will be able to put some of their ISA allowance into bonds and other debt securities made through P2P and crowdfunding sites.

Another boost to this sector is expected to come from SIPPs as more retirees take advantage of pension freedoms. Additionally, new regulations capping HNW individuals’ pensions contributions will mean that investors look for other vehicles to improve their returns and manage their tax relief.

Investors’ ability to place this type of bond within these tax wrappers may prove attractive to income hungry investors.

Conclusion

With interest rates at all-time lows, a number of clients will be unhappy with the returns they’re getting from their savings. As people seek better returns and companies become more creative in how they raise money, we believe the debt-based crowdfunding proposition should continue to grow. Crowdfunding may give financial advisers an opportunity to advise on a portion of their portfolio that they don’t already. This may become increasingly attractive when an investment is made through a SIPP or ISA wrapper. Clients may not have the time or the ability to differentiate between the myriad of crowd offers – advisers have a valuable role to play in guiding their clients in this new and innovative market.