By Ian Lance of RWC Partners

As the prices of nearly everything have soared over the last year, the world’s major central banks have been assuring investors that this is just a temporary blip or as Jerome Powell, Chairman of the US Federal Reserve, had repeatedly said, inflation is just ‘transitory’. The Bank of England had also been singing from the same hymn sheet.

“The Committee’s central expectation is that current elevated global and domestic cost pressures will prove transitory.”

For the moment, most investors seem to believe this narrative given that bond yields in most countries are several percentage points below the current levels of inflation (incredibly, 85% of US junk bonds now yield less than US CPI!) and, in many parts of the world, equities sport some of the highest valuations witnessed in stock market history.

The market has been remarkably trustworthy about these assurances given the poor forecasting records of the central banks.

“All that said, given the fundamental factors in place that should support the demand for housing, we believe the effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system,” Ben Bernanke in May 2007.

“The Federal Reserve is not currently forecasting a recession.” Ben Bernanke 10 Jan 2008 (it was later determined the recession had started in December 2007).

“The GSEs are adequately capitalized. They are in no danger of failing.” Ben Bernanke July 20, 2008 (the GSE’s were placed into conservatorship in September 2008).

It should also be obvious that central banks are talking their own book as they need the current levels of inflation to be transitory having painted themselves into a corner by blowing one of the biggest asset bubbles of all time. This now requires continuous money printing to stop it from collapsing and a sustained increase in inflation would put pressure on this strategy.

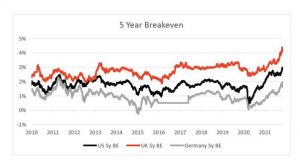

In the last few weeks, however, something appears to have changed. Firstly, as inflation figures have continued to surprise on the upside, central banks have been forced to admit that maybe it wasn’t going away. In the US, the year-on-year change in the CPI index was 5.4% in September 2021, whilst the producer price index (PPI – a measure of the prices that producers pay, and therefore a leading indicator of where consumer prices may be heading) change came in at 8.6%. The Bank of England’s new economist, Huw Pill, has said he would “not be shocked” to see UK inflation reach 5% or above in the coming months.

The idea that inflation will remain at elevated levels has begun to be reflected in market expectations of inflation as shown by the breakeven (chart below) which are at 11-year highs.