")

A recent IFA Magazine survey, conducted in partnership with Pru, examined readers’ thoughts and perceptions of intergenerational advice. The vast majority of respondents labelled this as important, and that the future of advice – as well as business continuity – relies on advisers engaging effectively with younger generations.

Intergenerational planning is becoming a particularly hot topic in the world of financial advice. In light of this, IFA Magazine recently conducted a survey in partnership with Pru, to explore readers’ perceptions of intergenerational planning – and if they believe there to be real merit to it.

So, what did IFA Magazine’s audience reveal?

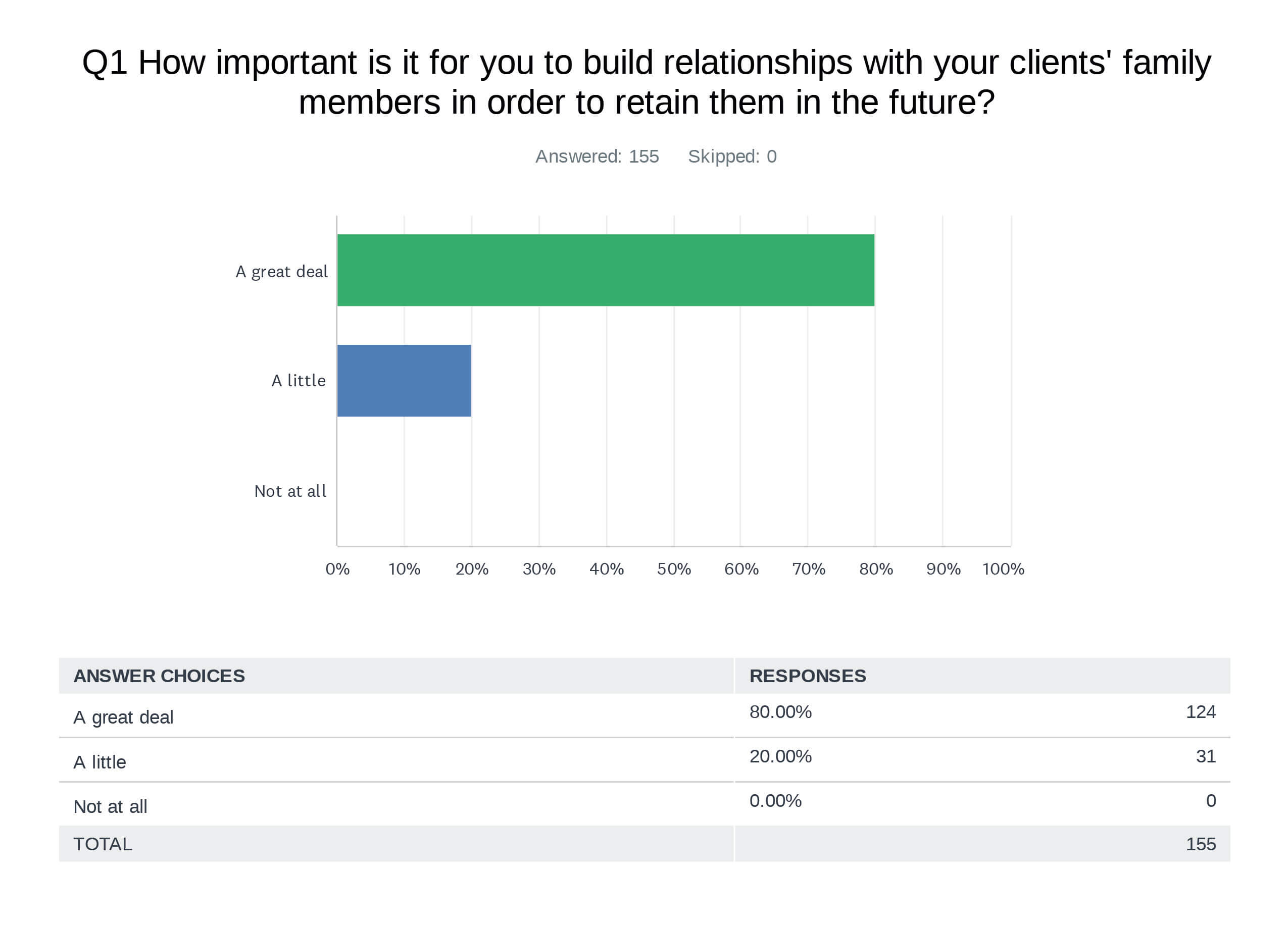

Perhaps most notably, Figure 1 highlights that when asked how important it is for advisers to establish relationships with clients’ family members, and thus lay the foundation for future business, all survey respondents indicated this to be important to some extent. Furthermore, the vast majority of respondents – an impressive 80% – assigned “a great deal” of importance to relationship building with family members (see fig 1).

Mind the gap

These results leave little confusion about survey respondents’ thoughts on building relationships with clients’ family members – the general mood is clearly that this is a must.

Although the consensus is very much that building relationships across the generations is crucial – many respondents highlighted key areas of Intergenerational Planning in which they felt they could benefit from further support (see Figure 2 ).

IHT Planning, Later Life Planning, and Gifting were the three most identified areas where advisers say that they need support, with IHT Planning being a particularly weak point for respondents; 79% of those surveyed indicated that they would welcome support in this area. Two-thirds (66%) responded that they also required further support for Later Life Planning, and a similar proportion (65%) signalled this for Gifting. School and University Fee planning was another recurring area for support at 33%. Finally, 12% also cited other areas where further support would be beneficial – a few examples included: pension and ISA planning for children, mortgages, and basic financial planning for young adults. These results show some scope for development in the world of intergenerational advice – as our respondents have conveyed a lack of confidence in multiple associated areas.

Figure 1

The impact of technology

The third section of our survey asked respondents if, and how, they anticipate the future of advice changing in terms of the technology used. The results were striking, with less than 1% stating they do not see technology affecting the profession in any capacity in the future. The majority (52%) expressed that they expected technology to alter the future of advice “a moderate amount”, and 47% felt that it would have “a great deal” of influence.

In addition, a broad range of scenarios, detailing if and how technology will change the future of advice, was highlighted by respondents. A common answer was that technology will improve the technical aspects of advice, for example by speeding up the documentation of advisers’ processes, increasing integration between tools, and through the efficiency of digital onboarding. In addition, one respondent cited the “increasing regulatory burden” as a reason why greater efficiency, afforded by technology, is needed.

Multiple respondents predicted that there would be greater digital engagement in the future – with a heavier reliance on social media, for example. In addition, respondents often characterized the younger generations as more “tech-savvy” and, therefore, likely to use apps for financial advice, rather than advisers.

Figure 2

Human touch

Human touch

Human touch

Human touchArguably, one interesting point to emerge from our survey responses was the debate regarding whether meetings with future generations of clients would be carried out virtually or in person. Several respondents voted on the side of virtual meetings, with some individuals stating that they believe the likes of Zoom and Teams would continue to rise in popularity with advisers. Furthermore, one respondent went a step further adding that “the days of face-to-face are limited” due to the time constraints of modern life.

Nevertheless, several respondents disagreed with this sentiment – arguing that, ultimately, clients still want face-to-face interaction with their advisers. Financial Planning is about building relationships based on trust and we all know that having meetings face to face certainly works. According to one of our respondents, a key reason for this is that financial planning is emotive. Therefore, the human touch, that comes with meeting in person, can be a great source of comfort and truly invaluable to clients. Another respondent stated that the sheer complexity of intergenerational planning makes certain that clients’ family members and future generations will have to meet with advisers in person.

Finally, following the theme that we have seen post-pandemic, one respondent anticipated that we would continue to see a combination of face-to-face and virtual meetings in the future.

What we can gather from this, is that almost all respondents believe technology to be a significant part of the future of advice. However, whether respondents think this will actually lead to the end of traditional, face-to-face meetings, is a more contentious aspect.

Under the advice bonnet

We were keen to find out whether advisers, as a matter of course, recommend clients complete a Lasting Power of Attorney. A strong majority – 94% – of our respondents said they did indeed advise clients to set up an LPA, compared to a minimal 6% who said they did not. These compelling results illustrate the all-encompassing role of advice and advisers’ responsibility to express clients’ financial and health-related wishes.

In addition, we were also interested to hear our survey audience’s thoughts on educational funding. We asked respondents whether they considered the use of international bonds for clients saving for their children’s education, with 65% reporting they did not (compared to 35% who answered ‘yes’ to this question). This perhaps reveals an untapped opportunity for advisers looking to help clients fund their children’s education.

Resources and tools to support advice process

We also asked our survey audience if they were aware of Prudential’s Trust range. The answer was a definite yes – with 63% stating that ‘yes’, they were familiar with the range, compared to only 38% who were not.

Our survey also highlighted that the majority of our audience was not aware of a number of other helpful resources available from Pru. 55% of respondents were unaware of 1) Prudential’s comprehensive Trust and IHT planning modelling tool – which provides a useful shortcut for advisers and 2) the support and educational materials available on the Prudential website. However, with regards to the latter, 45% said they did have knowledge of these educational materials and one respondent highly commended the technical guidance and its value to clients.

It seems our survey audience believes that intergenerational planning is the key to the future of advice – and that increasingly the use of technology will play a significant role in determining what that “future” looks like!

Access to expert technical resource at your fingertips

Finally, 60% of our respondents also noted that they did not know they could speak to M&G Wealth’s technical team via their account manager. This could be hugely beneficial to advisers – and currently, the majority are not taking advantage of the opportunity.

Survey details IFA Magazine’s survey, entitled ‘Understanding intergenerational advice’, received 155 responses from our readers and ran from 1st – 13th June 2022.

Helpful tools

Advisers and paraplanners can access a range of helpful resources from Pru that will help them navigate the complex, but evidently increasingly important, world of intergenerational advice.

For more information on this, click here