Laith Khalaf, Head of Investment Analysis at AJ Bell:

“Inflation is on the rise, but the jury is out on how sustained price rises will be, as there are compelling arguments on both sides of the inflationary divide. Huge amounts of fiscal and monetary stimulus stand a good chance of coaxing the inflationary genie out of the bottle, but at the same time there are seemingly valid reasons why the Bank of England is holding off hiking rates, in the belief that inflation is transitory.

“Economic distortions that occurred last year will gradually fall out of the picture, which should have a moderating effect on the headline inflation rate. In particular, rising fuel costs and high wage growth don’t look repeatable year on year. We should also be mindful that the Chancellor’s stimulative giveaways in the March Budget were also accompanied by a tax grab starting in 2023, taking money out of the pockets of consumers and businesses to balance the books, and hence acting as a brake on inflation.

“Probably the clincher for the central bank is the highly asymmetric nature of its firepower. With interest rates at historic lows, and £895 billion of QE on the books, the Bank has plenty of ammunition to fight inflation if required. If it needs to stimulate the economy on the other hand, it’s got hardly anything left in the locker. For the Bank of England, it therefore makes sense to err on the side of stoking inflation rather than risk undermining the economy.

“Inflation poses a different puzzle to investors than it does the central bank though. Many of the assets that have swelled in portfolios over the last decade have been those that prosper in a low inflation environment, and conversely will struggle if price rises take hold. Investment portfolios are therefore likely to be underprepared for an inflationary environment without some adjustment, and if the weight of evidence starts tipping towards sustained price rises, investors may rue not having rebalanced their investments.”

Why the Bank of England is looking through inflation

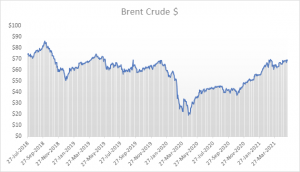

Oil prices

The oil price is a key component of inflation, but if we look at the oil price today, it is little changed from two years ago. Compared to one year ago however, it is significantly higher because of the huge fall in fuel demand following global lockdowns last spring and summer. Indeed at one point some oil contracts started trading at negative prices, so distressed was the market. Headline inflation is an annual figure, comparing prices today with prices one year ago. It’s therefore not just a picture of what is happening today, but how that compares to what was happening last year. In order to continue to exert a similar upward force on inflation over the coming year, we would need to see another dramatic rise in the oil price, and it seems highly unlikely we will see a demand or supply shock as significant as the mothballing of major economies which we witnessed in 2020.

Source: Refinitiv