Idanna Appio, portfolio manager and senior research analyst at First Eagle Investments, examines the Supreme Court’s ruling against the Trump administration’s tariff powers and the shift to new trade measures. Noting that while tariff uncertainty and litigation risks persist, the decision reinforces US institutional checks and balances.

As the US Eastern Seaboard digs out from a storm that dumped as much as two feet of snow in major metropolitan centers, investors and business leaders worldwide are unpacking the latest flurry of activity in the Trump administration’s efforts to recast global trade.

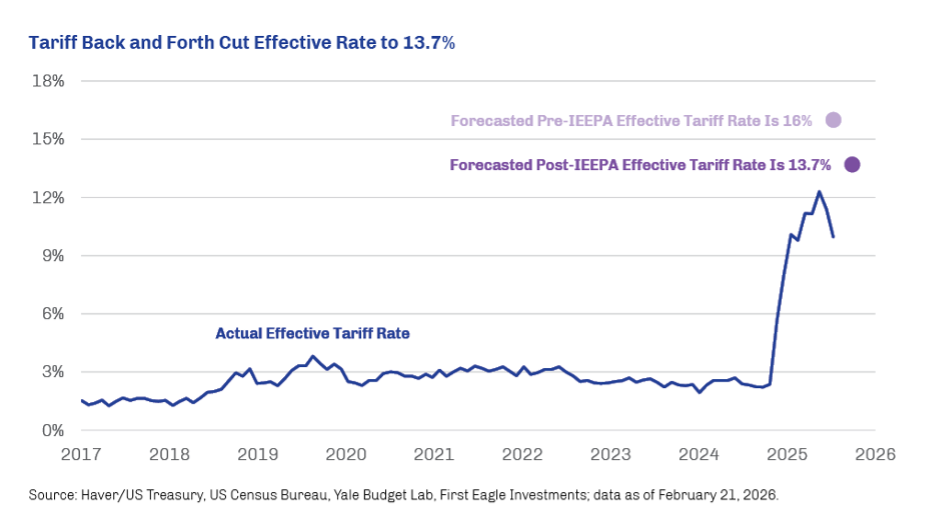

The Supreme Court on Friday ruled 6-3 against the Trump administration’s use of the International Economic Emergency Powers Act (IEEPA) to impose the fentanyl-related and “reciprocal” tariffs announced in the first few months of 2025. As anticipated, Trump was quick to respond to this rebuke, immediately announcing a new 10% global tariff under Section 122 of the Trade Act of 1974, a rate he raised to 15% a day later. The Yale Budget Lab estimates that these actions reduced the effective tariff rate to 13.7% from 16% previously. As of December 2025, the actual tariff rate (based on customs revenues/imports) was 10%.1

Section 122 of the Trade Act of 1974 allows the imposition of tariffs up to 15% for up to 150 days, during which time the Trump administration is expected to seek justification under more permanent statutes. One commonality among the potential alternative statutes is the need for investigations and hearings, which will serve as bottlenecks to implementation. Further, the restrictions inherent in these statutes and the skepticism evident in the Supreme Court’s ruling suggest to us that the future likely holds less tariff revenue and more litigation.

The issue of IEEPA refunds went unaddressed in the Supreme Court decision, but many businesses have already filed lawsuits. We estimate nearly $100 billion of the $195 billion in customs revenue collected in fiscal 2025 could be refunded—slowly, in all likelihood—which implies that last year’s fiscal deficit was 6.2% of GDP as opposed to the reported 5.8%.2

Though tariff uncertainty will persist, the Supreme Court’s ruling is an important reaffirmation that both the rule of law and checks and balances still exist in the US, even if their execution is delayed.

1Source: Haver/US Treasury, US Census Bureau, Yale Budget Lab, First Eagle Investments; data as of February 21, 2026.

2Source: US Treasury; data as of September 30, 2025 (most recent available).

By Idanna Appio, Portfolio Manager and Senior Research Analyst, First Eagle Investments