The FTSE AIM market has experienced a more prolonged and sharper decline than seen in previous cycles. For private investors, this has prompted understandable questions about whether the current downturn reflects a typical market cycle or a more structural shift.

This period has been notably different from previous downturns. The scale and duration of the weakness stem not only from geopolitical and macroeconomic uncertainty, but also from government policy changes that have disproportionately affected smaller quoted companies listed on AIM.

With many AIM‑listed businesses now trading at what we view as once‑in‑a‑generation valuations, the potential for recovery is significant. Understanding the factors behind the recent decline is therefore essential when evaluating both the risks and the opportunities that currently exist.

Where are we?

AIM share prices have faced a sustained downturn since the market peak in October 2021. This weakness reflects several external factors, but it is largely not due to poor operational performance. In fact, the strength of delivery is reflected in earnings growth across the FTSE AIM 50—the market’s largest constituents— which has risen by more than 70% over this period, while their collective market value has declined by over 40%.

These dynamics have left AIM companies trading on exceptionally low valuation multiples, particularly relative to their growth prospects.

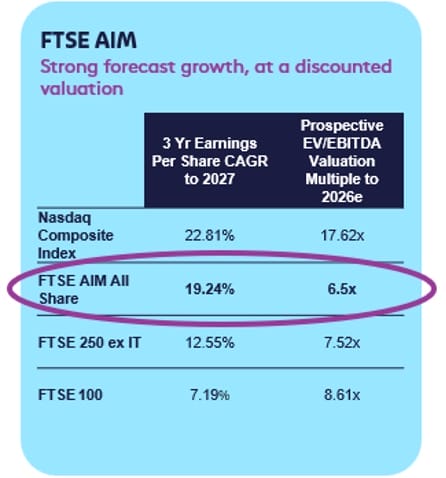

The table below shows Earnings Per Share (EPS) on a compound annual growth rate basis (CAGR), and prospective valuation multiples using EV/EBITDA. Despite the FTSE AIM Index being forecast to deliver nearly 20% annual earnings growth through to 2027, it currently trades at a significant discount to both the similarly high‑growth Nasdaq Composite and the slower‑growing FTSE 250 ex‑IT and FTSE 100.

Although FTSE AIM’s forecast EPS CAGR is broadly comparable to Nasdaq, the FTSE AIM index currently trades at less than one‑third of Nasdaq valuation multiples, highlighting the substantial disconnect between growth prospects and current valuations on AIM.

How did we get here?

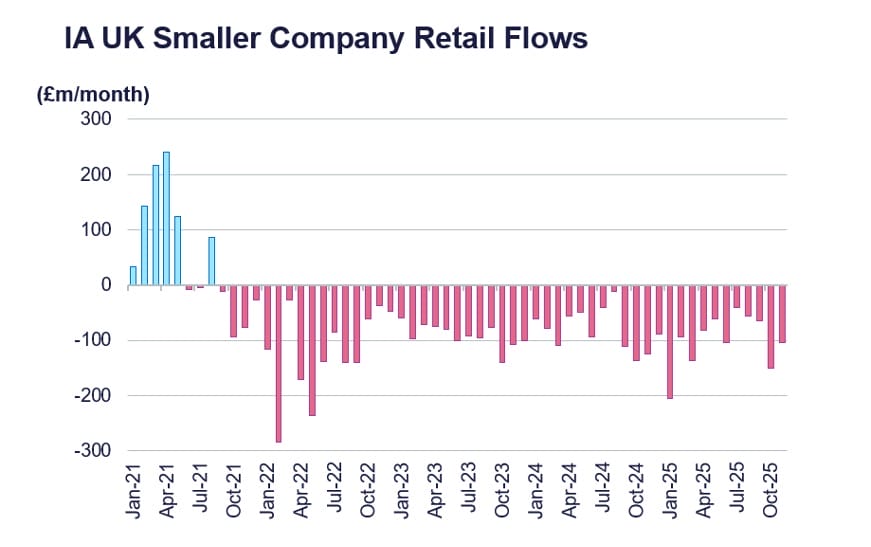

A combination of macroeconomic, geopolitical, and policy‑driven factors has contributed to significant outflows from UK equities. As widely highlighted across financial media, UK equity flows have been consistently negative in recent years, affecting all investor groups—from pension funds to retail investors.

Since 2021, the IA UK Smaller Company sector alone has experienced c£4bn of net outflows and now represents AUM of only £7.8bn.

Pension funds and large asset managers have increasingly shifted towards global equities and private markets, while retail investor participation has also declined. At the same time, higher interest rates have had a disproportionate impact on AIM companies. Many AIM‑listed businesses are long‑term growth focused, making their valuations highly sensitive to the discounting of future earnings. The sharp rise in inflation and interest rates has therefore reduced the present value investors place on those future profits.

AIM has also been affected by upcoming changes to inheritance tax relief, with Business Relief (BR) for qualifying AIM shares falling to 50% from April 2026, weighing on flows into AIM BR products.

Despite these headwinds, it remains important for private investors to separate short‑term issues from long‑term fundamentals. Extended periods of weakness often create attractive entry points, particularly when high‑quality businesses are trading at meaningful discounts to their intrinsic value. Historically, AIM recoveries tend to build gradually, driven by improving confidence, liquidity, and underlying company performance.

Why AIM matters?

Despite recent weakness in AIM share prices, the market remains one of the most successful global growth platforms. It is home to more than 600 companies and, over the past 30 years, has enabled over £138 billion of capital to be raised for more than 4,000 businesses.

According to a recent LSE/Grant Thornton report, AIM‑listed companies are almost 50% more productive than private company peers, export more than four times as much as their private counterparts, and support close to 800,000 jobs across the UK. For a government focused on growth, strengthening AIM has therefore become an increasingly explicit policy priority.

Any initiatives designed to support UK growth companies and long‑term investment have the potential to materially improve sentiment and help revitalise valuations across many AIM‑listed businesses. With fundamentals remaining strong and AIM’s economic contribution widely recognised, such policy momentum could act as a powerful catalyst for recovery.

What is the opportunity going forward?

Looking ahead, several factors could help improve conditions. Interest rates are now declining, and a sustained shift toward lower rates would support valuations and encourage investors to re‑engage with growth assets. Even modest institutional inflows—particularly those aligned with the Mansion House Accord of 2025—could have a meaningful impact on valuations given today’s subdued levels. Policy measures aimed at strengthening UK growth companies and long‑term investment would also provide an additional tailwind.

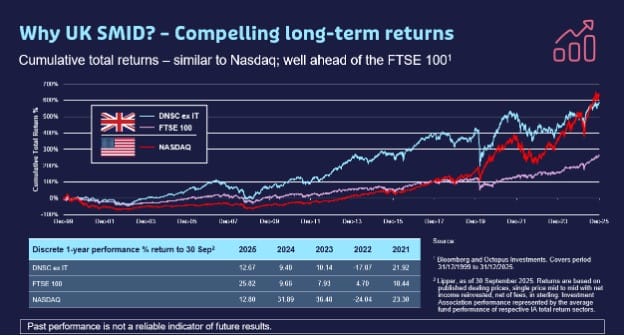

While recent commentary has understandably focused on AIM’s near‑term challenges, it is important to recognise the strong long‑term track record of UK growth companies. Since the start of the century, the Deutsche Numis Index (the smallest 10% of companies listed on the main list of the FTSE) has delivered cumulative returns of almost 600%, comparable to the Nasdaq and materially ahead of the FTSE 100. This history of sustained strong performance by growth companies underscores the long‑term opportunity and highlights why a recovery from current levels could be significant.

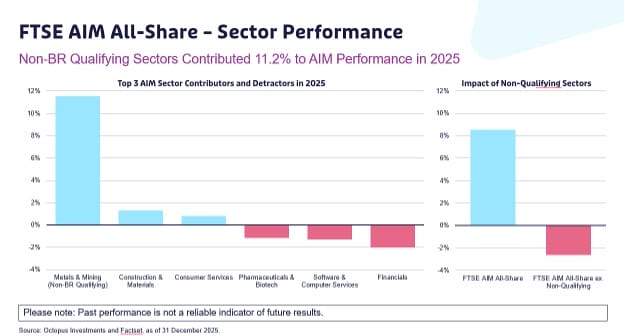

After several years of UK equity underperformance, we are beginning to see early signs of recovery in some parts of the market. In 2025, a commodity‑driven rally in Energy and Materials supported strong performance among companies in those sectors. Although resource stocks do not qualify for Business Relief, their strength contributed in part to the FTSE 100’s +21.5% return for the year. FTSE AIM also delivered a credible +8%, though it is notable that non‑qualifying metals and mining companies accounted for over +11% of that performance.

We note that previous recovery cycles have followed a similar pattern, with non‑qualifying resource and mineral‑focused companies leading the initial rebound following the last significant market pullback after the Global Financial Crisis in 2008/2009. As conditions improved and inflation eased, the recovery broadened, and higher‑quality growth sectors such as pharmaceuticals and technology, ultimately outperformed.

Encouragingly, IPO activity has also begun to return, with several high‑profile companies listing in the final quarter of last year and a growing pipeline expected in the months ahead.

In conclusion, our conviction in the long‑term value of investing in AIM-listed companies remains strong. We continue to engage actively with policymakers to emphasise AIM’s significant contribution to UK GDP, and we are encouraged by the increasing recognition of its importance. While the current AIM downturn has lasted longer than anticipated, it largely reflects broader factors that have weighed on capital flows—many of which are now showing signs of easing. While this has been a challenging period for investors, it reinforces the importance of selectivity, diversification, and maintaining a long‑term perspective. For those focused on quality and growth fundamentals, the AIM market currently offers highly attractive potential returns as part of a balanced portfolio.

By Chris McVey, Deputy Head of Quoted Companies, Octopus Investments

To learn more about the world of tax-efficient investments, be sure to check out our recent Tax-Efficient Investment Insights!