Global bond markets continue to offer some of the most attractive income levels in over a decade, but investors can no longer treat fixed income as a simple, passive allocation, says Julien Houdain, Head of Global Unconstrained Fixed Income at Schroders.

Yields are at near multi-decade highs and though central banks are moving in different, and sometimes opposing, directions, the opportunity set remains compelling. More now than ever, success depends on actively managing duration, geography, and credit risk.

A new era for fixed income

2022 marked a seminal year for bond markets. A supply side shock caused by the pandemic and exacerbated by Russia’s invasion of Ukraine triggered a sharp rise in inflation and led to the fastest global monetary tightening cycle in history. This period effectively ended the era of ultra-low rates and fundamentally reshaped how bond markets behave today.

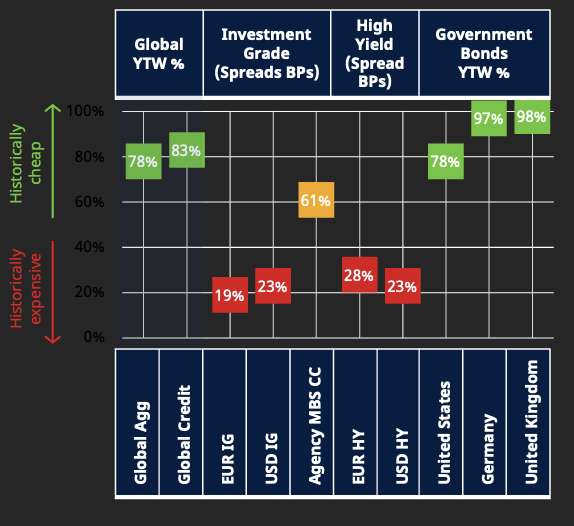

Figure 1: Credit spreads are tight but all-in yields are attractive

With credit spreads (the premium paid for holding additional credit risk) tight from historical standards

– and more of a corporate bond’s overall return coming from interest rates – it’s necessary to pay a lot more attention to what central banks are doing. The chart below illustrates that even though credit spreads are tight, (albeit not as tight as they have been recently), all-in-yields are very attractive.

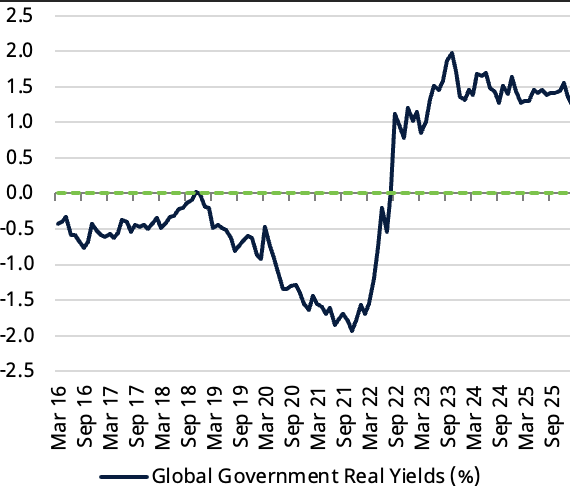

Unlike 2022, today’s income levels provide a strong starting point for investors. Real yields (when adjusted for inflation) illustrated below are significant once again and that yield helps protect against market volatility. Even in a fairly conservative portfolio – with limited exposure to higher-risk sectors – it is still possible to generate around 5–6% of yield.

Figure 2: Inflation adjusted government bond yields %

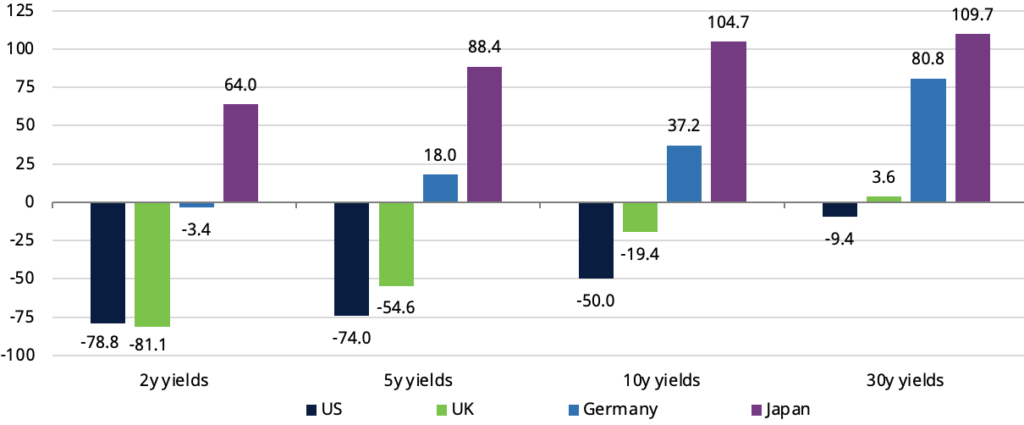

Diverging policy cycles create opportunity One of the defining features of the current environment is the divergence we’re seeing across countries and at various points of the yield curve. If you look at the moves in major rates markets in 2025 for example the results are very different. We saw long end yields in Germany and Japan punished for pursuing fiscal stimulus. However, the story behind the rates move in the US and the UK was more about easing inflation pressures and softer labour market dynamics, with shorter dated yields falling as additional monetary policy easing was priced in.

With this divergence expected to continue – and events unfolding in the Middle East having the potential to exacerbate this trend – it’s important to be agile as the narrative changes. When constructing portfolios, choosing the right market and the correct point of the yield curve can significantly improve investment outcomes.

Figure 3: Yield moves across country and curve over 2025

Our ability to separate interest exposure from credit exposure is a key advantage when managing global portfolios. We might like the story in Europe for instance because there is fiscal room in Germany and companies that could benefit from stimulus; often under-researched, non-listed names where we think we can generate alpha. But that doesn’t mean we would necessarily want the sensitivity to European rates. So, we can buy European corporates, but isolate the credit spread impact by hedging the interest rate risk.

This is very different from simply buying European investment grade or buying European high yield. There is no such thing as just ‘income’ anymore.

Where do the fiscal vulnerabilities lie?

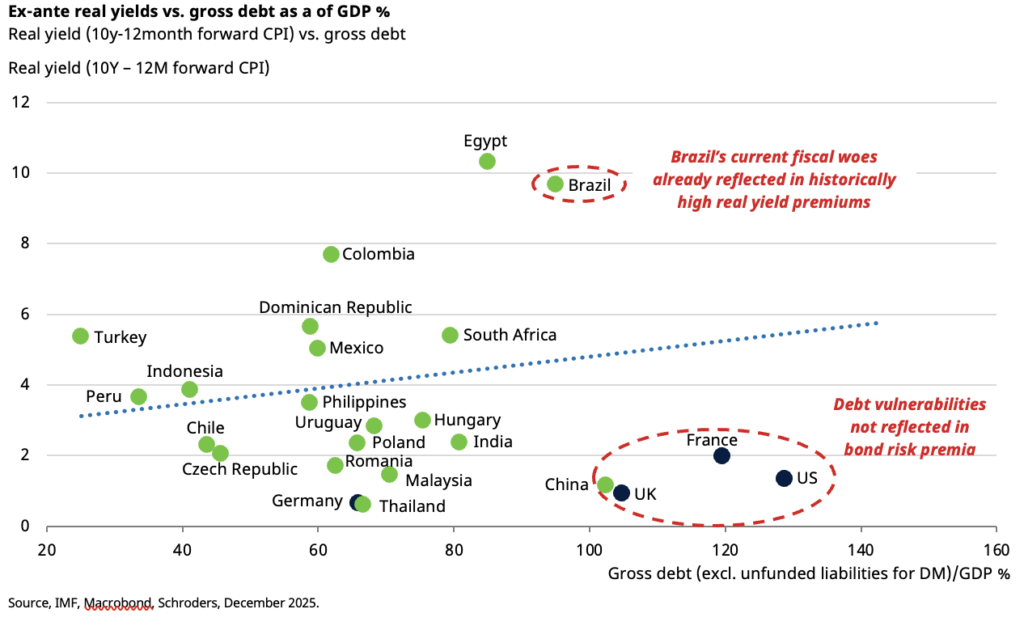

A global perspective quite literally opens up a world of opportunity. One of the trends we’re currently able to capitalise upon across our global strategies is the relative attractiveness of emerging markets versus developed markets.

While emerging markets are perceived as riskier, actually it’s in developed market economies where fiscal vulnerabilities are increasingly concentrated.

In fact, when considering a country’s debt-to-GDP versus its real yield, investors are well compensated for holding EM debt compared to the developed world, where debt is high

and real yields are much lower in comparison.

As with developed markets, when allocating to emerging markets the ability to allocate to a specific country and point on the yield curve is important. For example, currently we would be more comfortable allocating to emerging markets in shorter maturities (zero-to-five-year part of the curve) where central banks have more control over what happens if deficits remain large. It also reinforces the need to be disciplined on duration, and cautious about excessive

long-duration exposure.

Figure 4: Fiscal concerns largely a DM concern, while attractive real yields can be found in EM

Starting yields: a built-in buffer

Despite geopolitical tensions and policy uncertainty, starting yields today can provide meaningful downside protection

across a range of macro scenarios.

Running through different scenarios for the next 12 months – ranging from below trend growth and central banks cutting aggressively to the other tail risk where growth is unsustainably strong – it’s difficult to build a scenario where fixed income does not contribute to portfolios.

But to really benefit from shifting narratives, it’s only by comparing our own level of conviction with the market consensus that we can truly understand where the real opportunities lie. Attractive levels of income only get you so far – and they provide a safety net – but to reap the benefits the bond market offers, it’s much more complicated than simply buying bonds.

This feature was part of our 2026 Fixed Income Insights. For deeper analysis on bond markets and rates strategy for advisers, explore IFA Magazine’s latest Fixed Income Insights publication.

About Julien Houdain

Julien Houdain is Head of Global Unconstrained Fixed Income at Schroders. He runs a number of alpha focused strategies including benchmark relative, total return and income orientated products, combining qualitative forward-looking strategy with quantitative techniques in portfolio construction. He joined Schroders in 2019. Before Schroders, he worked at Legal & General Investment Management, most recently as Head of Global Bond Strategies.