The UK General Election in July sailed through without even so much of a bump in markets. When it comes to politics, attention now turns to the US presidential election and who will control Congress. I’ll touch on the potential implications of the US election for investors in the last section.

It wasn’t politics that spooked markets in the third quarter, but recessions and the yen carry trade. As a quick primer, a carry trade involves borrowing in a country with low interest rates and investing the proceeds in another country where yields are higher. Therefore, investors borrow a low-interest currency – such as the Japanese yen – and sell it to buy a higher-yielding foreign currency to then invest in assets denominated in that currency. Investors profit from the difference between the higher returns on their investments and the lower borrowing costs, assuming the currency exchange remains stable. Due to Japan’s very low interest rates, investors have sold large amounts of Japanese yen to invest abroad. Some estimate the amount to be into the trillions of dollars, with significant leverage involved. Consequently, when the Japanese yen strengthened in early August, it triggered significant volatility in asset prices as investors rushed to unwind their yen carry trades. And when leverage is involved, many traders become forced sellers, which perpetuates the fall in asset prices.

Alongside this volatility, market pricing also suggested that recession risk has returned. It was a sudden shift in focus as investors deemed a recession as the greater concern over that of rising inflation. This is significant given where we are with central bank interest rates across Europe and the US as they are at a level that is intended to restrict economic activity.

Therefore, the key topic for this quarter is one of recession and central bank response to this potential risk. Then for multi-asset investors, how we can mitigate this risk in portfolios.

Predicting Recessions

Predicting recessions is hard. Many people try, and many people fail. Even the stock market gets it often wrong, leading to the old saying that the stock market has predicted nine out of the last five recessions.

Only back in November 2022, the Bank of England warned that the UK was facing its longest ever recession since records began. Specifically, that the country entered a downturn in the summer of 2022, and it was expected to last until the first half of 2024. This prediction came with an expectation that the unemployment rate would double by 2025. Figure 1 shows what actually happened over this time period.

Figure 1: UK Gross Domestic Product (GDP) growth on a quarterly basis from 2019 showing the pandemic recession and the shallower recession at the end of 2023. A recession is defined as a sequence of two or more quarters of negative growth.

The scale of the pandemic-induced recession does skew the above chart due to how much the UK economy contracted in the second quarter of 2020. However, the Bank of England’s prediction for a recession starting in 2022 was not for it to be this deep, but for the recession to last longer. We now know the UK did enter a recession back in the third and fourth quarters of 2023, which is just about visible in Figure 1. Although this certainly isn’t the longest recession on record. For reference, the recession during the financial crisis of 2008/09 lasted for five quarters.

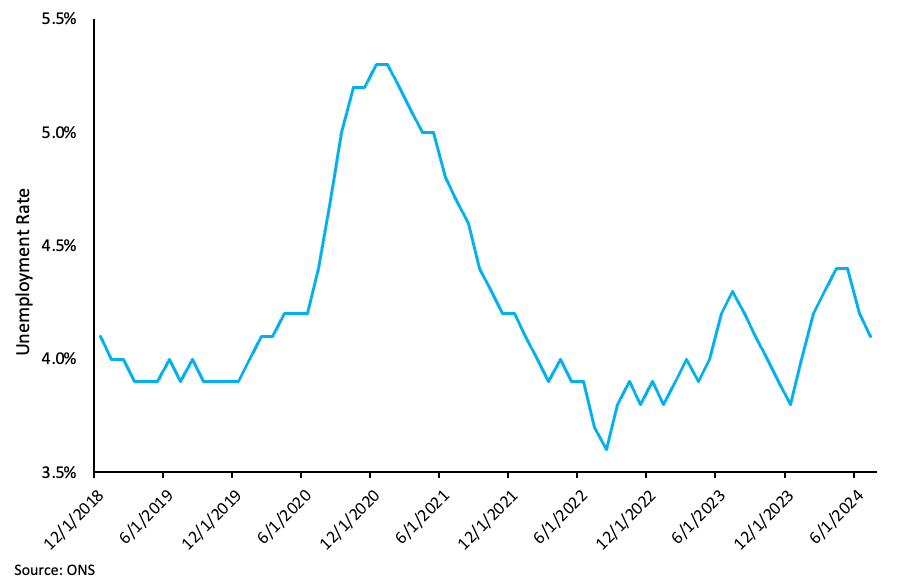

The Bank of England also expected the unemployment rate to double by 2025, which would result in a rate of unemployment of about 8%. Figure 2 suggests that this is not likely to happen, at least in the next three months. Again for reference, the last time the UK experienced an 8% unemployment rate was during the financial crisis and its aftermath.

Figure 2: The unemployment rate from the end of 2018. The rate of unemployment would have to increase significantly in the coming quarter to reach the Bank of England’s 2022 prediction of it doubling by 2025.

Many economists, business leaders and media outlets were forecasting recessions to come during 2022, so the Bank of England was not alone. Indeed, the ‘hard landing’ versus ‘soft landing’ analogy that has permeated market debate for over two years now stems from recessionary predictions; a hard landing is one where a central bank brings inflation under control but with a consequent recession, whereas a soft landing avoids the recession altogether.

Thinking back to the bout of volatility in August, it was, in part, caused by another recessionary signal known as the Sahm rule, as related to the US labour market. It states that when the three-month moving average of the US unemployment rate rises by 0.5% or more over the minimum of this rate from the previous 12 months, a recession usually ensues. This is a bit of a mouthful, but it essentially means that when people are losing their jobs at pace, a recession is very likely. The rule is logical and has been a good predictor of recession in the past, but it is not infallible.

The Sahm rule was triggered in August for the first time post-pandemic as the US employment rate ticked up to 4.3% in July, from a previous 4.1%. This uptick triggered the Sahm rule two days after the Federal Reserve (Fed) held interest rates at a cycle high. Stocks fell while bonds rallied as the market priced that the Fed was going to cause a recession by keeping interest rates in restrictive territory for too long. I’ll come back to the bond market in the following section.

Since this August volatility and worry about a recession, the market has calmed. Further data has shown that the US labour market is cooling from what has been a historically tight period for job creation and wage growth, yet remains a market that the Fed calls ‘full employment’.

Hence, there does not seem to be a recession on the horizon for the fourth quarter of this year in the US, nor the UK. Particularly not at the extremes the Bank of England predicted which was on a scale last experienced during the financial crisis. Although my prediction for no recession in the fourth quarter may be just as bad as most others.

However, multi-asset investors can now take advantage of what is a compelling bond market to mitigate some of these recessionary risks.

There is Opportunity in the Bond Market Again

Equity markets fell during the August volatility, with the S&P 500, a measure of the largest companies’ share prices in the US, down 6% in the first week of the month. It wasn’t the same across all asset classes as certain bonds rallied when focus turned to recessions. As an example, the exchange-traded fund (ETF) tracking long dated US government bonds rose 4% at a time when the US stock market fell 6%.

This inverse relationship of bond prices rising and stocks falling, or negative correlation to use the mathematical term, was not apparent during the last major sell-off in financial markets back in 2022. Indeed, across that year, the same US government bond ETF that weathered the recent August volatility much better than stocks, crumbled 33%. During this period, the S&P 500 ETF only fell 19.5%. At times, US government bonds may not be the safe haven asset class in which they are often classified.

It raises the question, why did bonds fare much better versus stocks in August than they did in all of 2022? The answer comes down to the economic environment. During 2022, an inflation shock weighed on bond prices due to the fixed nature of the income that investors earn from owning bonds. Fixed interest pays for less and less when inflation is accelerating. Central banks then raised interest rates aggressively, placing more pressure on certain parts of the bond market. Furthermore, rising interest rates tend to have an inverse relationship with asset valuations, and this led to declines in equity markets as stocks became cheaper.

However, when markets are responding to recessionary risks, rather than inflationary risks, bonds can act as the diversifiers we want them to be. Hence during August, as we saw the balance of risk shift towards a potential recession and away from inflation, bond prices rose but stocks moved lower. The reaction of the bond market was good news for investors in more defensive asset allocations with greater weightings to bonds as these holdings provided the diversification we craved in 2022.

But back to predicting recessions for a moment. As mentioned, we don’t think a recession is around the corner for this quarter. Neither in the UK or the US. Corporate earnings still look robust, the private sector has been deleveraging since the pandemic, and the labour market in both countries still looks healthy and is enabling consumers to spend. Yes, the US labour market has cooled significantly, but from very tight levels as the pandemic has unwound, although this remains an area to monitor. Nevertheless, it is inevitable that a recession will hit eventually, with the consolation that bonds should act as diversifiers again when it happens.

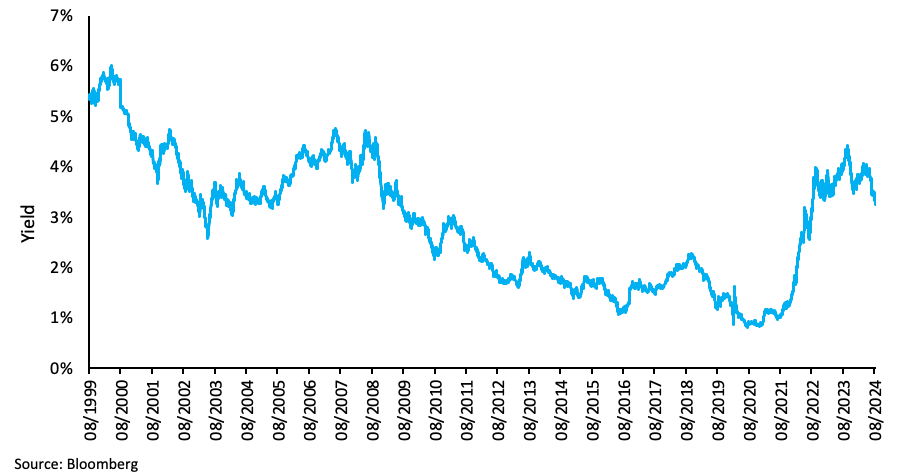

In the meantime, investors can now take advantage of bond yields that we haven’t seen since the mid-noughties (Figure 3). We can see the aggressive repricing of yields across this broad measure of the bond market from late-2021 to 2023 as inflation rose, which has left behind a bond market that is ripe for investment.

One other interesting statistic shows that there was over $18 trillion of global debt with negative yield at the end of 2020. Today, that same measure shows there is zero. Given that there is now a very different inflation and interest rate regime, it is hard to believe we are heading back to negative bond yields. But for now, we can buy high quality bonds and generate real yields again while we wait.

Figure 3: The Bloomberg Global Bond Market Index showing aggregate yield across global investment grade fixed income, including government bonds.

A Quick Note on the US Election

Much like recessions, elections are very difficult to predict. The upcoming US election is no different. In addition, polling has been spectacularly wrong over recent times, including Trump’s last presidential win. As such, we cannot call what the result will be on the 5th November.

Adding further to the uncertainty surrounding the presidential vote in November is that both chambers of Congress are also up for election. Prediction markets expect the House to swing to Democratic control, with the Senate shifting to the Republicans, which would leave a divided government and therefore a president that will struggle to pass any legislation through Congress. During Trump’s first two years as president, the Republicans controlled both the House and Senate, enabling the smooth passing of the Tax Cuts and Jobs Act. However, Trump failed to repeal the Affordable Care Act (or Obamacare), even with his party in control of Congress.

With a divided government, we should expect to see greater use of executive orders and focus on areas where a president has discretionary authority, such as foreign policy. Therefore, a return to trade wars under a Trump presidency becomes a high probability as he has threatened a blanket 60% tariff on Chinese imports, and a 10% tariff elsewhere.

The good news is that the election shouldn’t matter for investors over the long term. Still, volatility is to be expected in and around the election. A study by Research Affiliates shows that US stocks are usually down in the lead up to an election, yet recover strongly in the weeks after, regardless of who wins. A week is a long time in politics, as the saying goes, such that the outlook for inflation, recessions and monetary policy are likely to be the biggest drivers for markets this quarter and beyond.

By Dr Dan Appleby, CIO of Blackfinch Group.