Bond market behaviour has shifted, forcing investors to reassess where to source income and how to build diversified portfolios. Sharing the following analysis, Ninety One’s Werner Gey van Pittius, Co-CIO Fixed Income, and Grant Webster, Co-Head of Emerging Market Sovereign & FX, explain why they believe that Emerging market debt offers a compelling choice – and why and how it’s moving into the mainstream.

Bond markets are in a new regime

Current geopolitical turmoil makes it easy to overlook a seismic shift in financial markets – but the implications for investors are profound.

Government bonds have historically been considered a reliable investment staple, cushioning against losses when stock markets behaved badly. However, in recent years, this narrative has shifted. Varying dynamics have increased volatility in the bond market, its behaviour now aligning more closely with other portfolio investments.

But not all bond markets look or act the same in this new regime, and debt issued by developing (or ‘emerging’) market economies stands out in this regard. Emerging market (EM) debt today offers some of the benefits that UK gilts and other bond markets no longer provide, with investors increasingly taking note.

Investor preferences are shifting

A shift in perceptions put EM debt firmly on investors’ radars last year, with a blurring of lines between emerging markets (EM) and developed markets (DM) a key catalyst for this.

While in major government bond markets – such as the UK gilts market – mounting concerns over the health of public finances jostled yield curves, the EM debt market proved to be a maturing and increasingly resilient asset class, standing firm against headwinds such as President Trump’s ‘Liberation Day’ tariffs and the more recent oil-price volatility that has rattled global financial markets.

Meanwhile, signs of a different regime for the US dollar – a headwind for EM local currency assets for over a decade – provided further incentive for investors to take a closer look at the asset class.

A powerful diversifier

Offering powerful diversification benefits, EM debt is particularly relevant in a world where traditional asset classes have become more closely correlated. Spanning local and hard (typically dollar-denominated) currency markets, and sovereign and corporate issuers, it is a vast and diversifying investment universe and a flexible portfolio building block.

EM debt can provide diversification in a variety of ways – from local currency debt markets giving exposure to different yield sources, to hard currency debt markets providing an attractive alternative growth fixed-income allocation, offering a higher yield for similar credit quality to developed market debt. EM FX represents a distinctive return driver that has historically contributed meaningfully to total returns over the long run; for investors who prefer to isolate the rates opportunity, local currency debt can also be accessed on an FX-hedged basis.

| EM debt component | Drivers |

| Local currency bonds (FX hedged) | Rate market moves: inflation, monetary policy, fiscal policy |

| EM FX | Balance of payments, monetary policy, growth, interest rate differentials |

| Hard currency bonds | Credit spread moves: growth, external balances, balance of payments, fiscal policy |

Source: Ninety One.

Positioning portfolios for tomorrow’s world

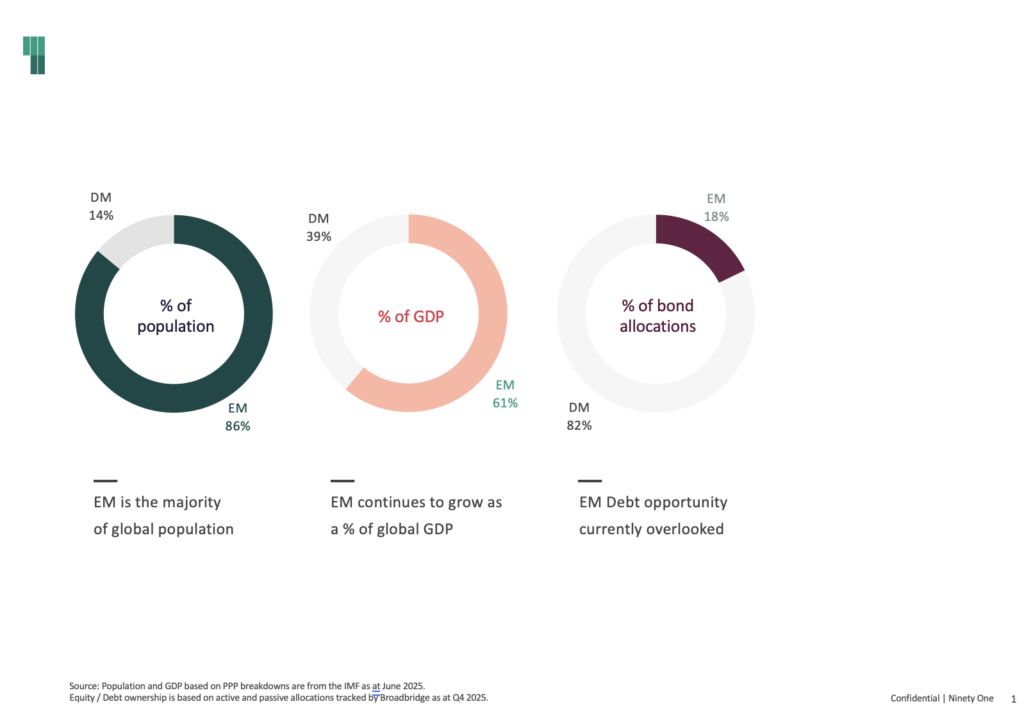

Longer-term global economic momentum is shifting away from developed markets, with emerging markets constituting a larger share of the world’s economic activity. Yet the asset class remains underrepresented in investors’ portfolios. This disconnect is a key consideration for investors looking to align with global macroeconomic and investment trends.

In addition, developments in the last several years paint a picture of a maturing and fundamentally robust investment opportunity set, helping explain the blurring of lines between developed and emerging bond market behaviour. Increasing uncertainty around policymaking in some of the world’s most developed economies contrasts starkly with the adoption of more orthodox monetary policy – from Brazil to Turkey – and improving fiscal restraint in many EM economies – from Egypt to Argentina. While exceptions remain, credible policymaking and fiscal reform have become defining features of the EM landscape, underpinning greater resilience and prompting credit rating upgrades. These are the economies to watch, and EM debt provides access to growth and development opportunities within such markets.

A useful – and liquid – source of income

History has shown that EM debt provides a return premium over developed bond markets which has far exceeded the relative risk.

In the hard currency sovereign market[1], the JPMorgan EMBI index yields almost 7%, outperforming the US high-yield market in terms of income while providing superior diversification across investment-grade and high-yield sovereign bond issuers while avoiding concentrated single-issuer risk. Meanwhile, in the EM corporate bond market[2], compensation for risk (credit spreads) remains higher than in markets with comparable credit quality, as country-specific concerns typically overshadow robust company fundamentals, meaning higher yields do not translate to proportionally higher volatility.

In recent years, investors have increasingly turned to developed market private market investments, predominantly in the US, in search of a return premium. However, concerns around illiquidity (divesting is proving more challenging than expected) and risk (high-profile failures have signalled greater underlying risk than investors had previously assumed), EM debt can offer a compelling alternative providing ample liquidity.

Pointers for investors

Even in 2025 – a strong year for the asset class overall – wide disparities between top and bottom performing market returns show that EM debt is not a homogenous asset class. Significant and rising diversity across and within markets reinforces the value of an active approach to investing while also meaning that index exposure alone will not capture the full opportunity set. For investors able to differentiate, the potential rewards are significant. Much of the EM debt investment universe, especially smaller ‘frontier’ markets, remains under-researched. This allows active investment managers to take advantage of market mispricing and a dislocation between valuations and fundamentals.

This feature was part of our 2026 Fixed Income Insights. For deeper analysis on bond markets and rates strategy for advisers, explore IFA Magazine’s latest Fixed Income Insights publication.

About Werner Gey van Pittius

Werner Gey van Pittius is Co-Chief Investment Officer, Fixed Income at Ninety One. In this role he jointly oversees the firm’s global fixed-income platform, shaping strategy, portfolio management and research across the asset class. He is co-portfolio manager of the Emerging Markets Hard Currency and Local Currency strategies. Werner has been instrumental in developing Ninety One’s sovereign and foreign exchange platform.

About Grant Webster

Grant is Co-Head of Emerging Market Sovereign & FX within the Emerging Markets Fixed Income team at Ninety One. He is co-portfolio manager for the Emerging Market Blended Debt and Sustainable strategies and also contributes to regional analytical research for CEEMEA, as well as Top-Down asset allocation. concentrating on investments and quantitative finance. He is a CFA® Charterholder and qualified as an Associate of the Institute of Actuaries (AIA, designation currently not held).

[1] Debt issued by EM governments and companies that are 100% state-owned. Denominated in US dollars (or, e.g., euros).

[2] Debt issued by companies based in EM economies, usually denominated in US dollars