With high inflation and possible base rate cuts ahead, savers could miss out on the best returns if they wait too long. Moneyfactscompare.co.uk reveals the state of play in the fixed bond market for savers.

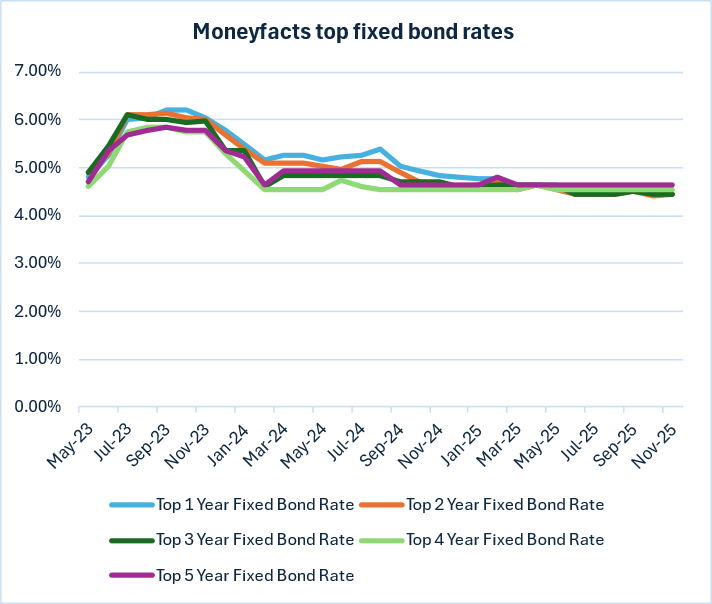

Top fixed bonds

- The top one- and two-year bonds rose, while the top three-year fell and the top four- and five-year bonds remained unchanged.

- The top one-year fixed bond rose to 4.46% gross, which is 0.18% lower than the top five-year fixed bond at 4.64%. The top five-year bond rate was higher than the top one-year bond a month prior by 0.19%.

- In May 2025, the top one-year bond paid 4.65% and the top five-year paid 4.64%.

- A year ago, the top one-year bond paid 4.85%, with the top five-year bond paying 4.64%, a gap of 0.21%.

| Savings market analysis – top fixed bond rates | |||||||

| May-23 | Nov-23 | May-24 | Nov-24 | May-25 | Oct-25 | Nov-25 | |

| Top one-year fixed bond rate | 4.82% | 6.05% | 5.18% | 4.85% | 4.65% | 4.45% | 4.46% |

| Top two-year fixed bond rate | 4.91% | 6.00% | 5.05% | 4.65% | 4.54% | 4.43% | 4.45% |

| Top three-year fixed bond rate | 4.90% | 5.97% | 4.85% | 4.72% | 4.61% | 4.45% | 4.44% |

| Top four-year fixed bond rate | 4.60% | 5.75% | 4.54% | 4.54% | 4.54% | 4.54% | 4.54% |

| Top five-year fixed bond rate | 4.71% | 5.80% | 4.95% | 4.64% | 4.64% | 4.64% | 4.64% |

| Top interest rates based on a £10,000 deposit as at the start of the month. | |||||||

| Source: Moneyfactscompare.co.uk | |||||||

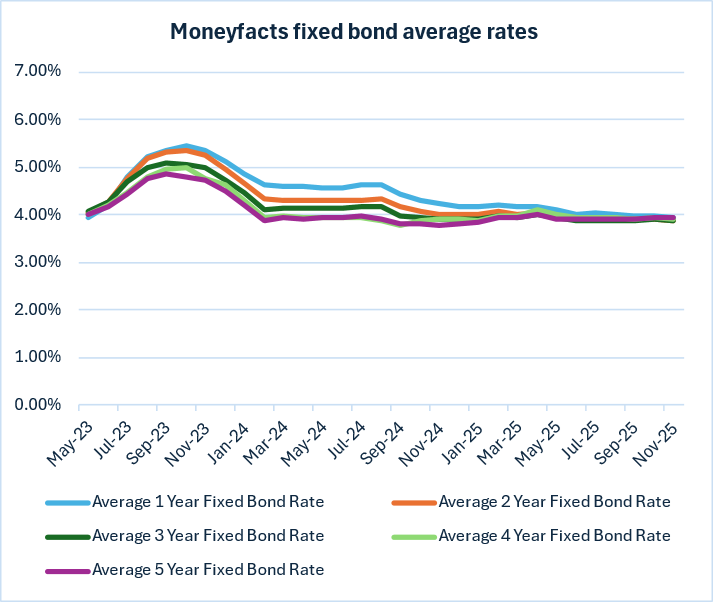

Average fixed bonds

- The average one-year fixed bond rate at 3.95% gross is now 0.02% higher than the average five-year fixed bond at 3.93%. The rate gap was 0.03% a month prior.

- In May 2025, the rate gap between the average one- and five-year bonds was 0.21%, as they sat at 4.12% and 3.91%, respectively.

- A year ago, the average one-year bond paid 4.24%, while the average five-year bond paid 3.79%, a rate gap of 0.45%.

| Savings market analysis – average fixed bond rates | |||||||

| May-23 | Nov-23 | May-24 | Nov-24 | May-25 | Oct-25 | Nov-25 | |

| Average one-year fixed bond rate | 3.96% | 5.36% | 4.58% | 4.24% | 4.12% | 3.99% | 3.95% |

| Average two-year fixed bond rate | 4.03% | 5.27% | 4.30% | 4.02% | 3.99% | 3.90% | 3.89% |

| Average three-year fixed bond rate | 4.06% | 4.98% | 4.13% | 3.90% | 3.94% | 3.92% | 3.87% |

| Average four-year fixed bond rate | 4.01% | 4.78% | 3.96% | 3.91% | 4.00% | 3.94% | 3.92% |

| Average five-year fixed bond rate | 4.02% | 4.73% | 3.93% | 3.79% | 3.91% | 3.96% | 3.93% |

| Average interest rates based on a £10,000 deposit as at the start of the month. | |||||||

| Source: Moneyfactscompare.co.uk | |||||||

Caitlyn Eastell, Spokesperson at Moneyfactscompare.co.uk, said:

“The top one-year bond has risen for the first time since July, however, it’s still a far cry from the highs of two years ago, when the best rates exceeded 6%. Savers who locked away £10,000 in the top two-year bond would now be enjoying over £1,000 in interest. This is compared to just £888 if they had an ‘average’ paying account. However, with many rates trending downwards or stagnating, savers risk seeing their real returns diminished, as under 500 fixed bonds can outpace inflation.

“If it is to be believed that inflation has peaked, this may not bode well for savers, as the chances of a base rate cut in December rise significantly. Understandably, savers may not be thrilled by the news of a base rate cut, but any hesitation to lock in their rates now could mean they miss out in real terms. Although it typically impacts variable rates in the first instance, it wouldn’t be surprising if providers factored this into their pricing for fixed rates.

“The latest Bank of England Money and Credit stats revealed that £5.8 billion was put into easy access accounts during September. This points to many savers adopting a ‘wait and see’ approach, and unwilling lock away their cash until after the Autumn Statement when more certainty is expected. However, depending on what changes, it’s not guaranteed that markets will react favourably, so it may be best to secure the market-leading rates now.”