Recent Budget announcements have brought inheritance tax (IHT) and estate planning into sharp focus for a much larger proportion of the population. By Siobhan Griffin, Director of Regional Business Development, TIME Investments, shares her insights.

The idea of an “estate” conjures up imagery of luxury superyachts and vintage car collections. This is sometimes the case, but the reality of the current environment is that many clients find themselves “accidental millionaires”: asset rich through property, pensions or long-term investment growth, but increasingly exposed to IHT without having made proactive estate planning decisions.

As the sector starts to grapple with the circa £5tn of wealth that will be transferred between generations by 2050, understanding IHT and how to navigate it has become a time-critical necessity.

The cost of uncertainty

Many advisers have reported seeing people delaying financial decisions and planning because of uncertainty around these changes.

While nervousness is understandable, the cost of delaying outweighs any challenges that come with proper estate planning. Fortunately, there are several measures in place that can help people avoid this and instead, mitigate the impact of IHT to leave more of their estate to their loved ones.

The power of Business Relief

Business Relief (BR), a longstanding and well-established tax relief designed to support UK businesses, has been part of the tax system since 1976. It has been widely used as an effective strategy for reducing IHT. For instance, when qualifying investments are held for at least two years and still owned at death, they can reduce IHT by 50% or even 100%, depending on the assets held.

For investors who want to plan ahead without locking money away indefinitely, BR qualifying investments can play an important role in estate planning. While recent changes have adjusted how unquoted BR assets can be used – up to £2.5 million per person (or £5 million for a couple) can now benefit from full relief – it continues to play an important role. It can’t be seen as an investment substitute for high-growth investment, but as a planning tool that can reduce reliance on lifetime gifting or trust planning for some clients.

Our flagship solution, TIME Advance, has been running since 2013 and currently manages around £1.7billion of client assets. It targets returns of 3–4.5% per annum after tax and charges, while maintaining access to capital, subject to liquidity.

Navigating BR conversations with clients

For advisers, the key takeaway is not that BR portfolios are “better” than traditional investing, but that they answer a different question.

“What outcome does my client want for their beneficiaries, and how quickly do they need to get there?”.

Clients may naturally assume that a higher annual return will always lead to a better outcome for their beneficiaries. However, when assets are potentially subject to IHT at 40%, headline growth figures can be misleading if not considered alongside investor profile, risks, time horizon and liquidity.

By moving away from the headlines and instead anchoring client conversations in practical estate planning objectives, advisers can reposition BR as a complementary solution within the wider estate planning toolkit.

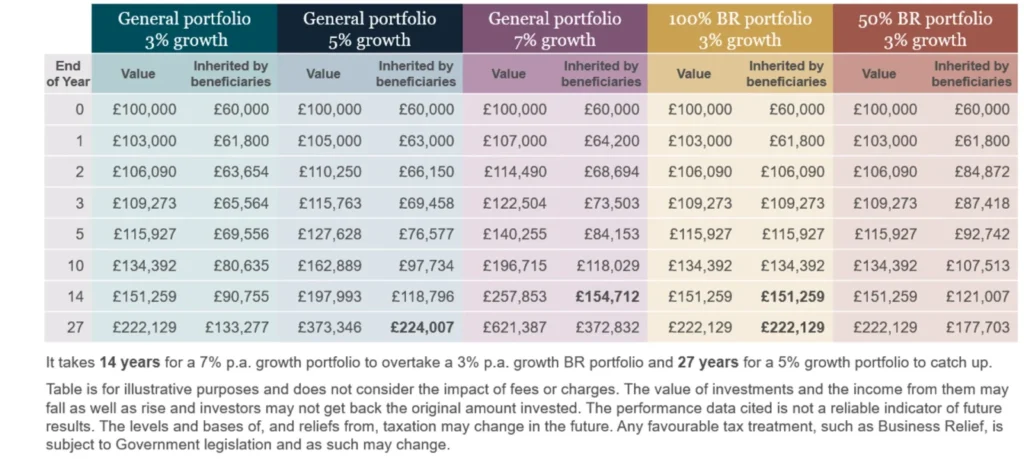

At TIME, we like to use one comparison in particular to help advisers bring this discussion to life with their clients: how long it can take for a conventional investment portfolio to overcome the advantage created by BR.

We use a comparison (illustrated below) between three simplified portfolios:

- Growth portfolio yielding 7% per annum

- Balanced investment portfolio yielding 5% per annum

- AND a BR-qualifying portfolio yielding 3% per annum

Tools like these help visualise how much longer it takes for higher growth from an investment portfolio to compensate for IHT. This in turn supports advisers in overcoming objections around the comparatively modest returns achievable via unquoted BR assets.

N.B. All portfolios assume the same initial investment and are shown on a like-for-like basis purely to demonstrate the impact of IHT, not to predict returns.

Because qualifying BR assets may be passed on free from IHT after two years (subject to legislation and individual circumstances), the BR portfolio retains its full value on death in this illustration. By contrast, the general and higher-growth traditional portfolios are shown net of a 40% IHT charge.

Even with a significantly higher assumed growth rate, in this scenario, the traditional portfolio would take around 14 years to outperform the lower-growth BR portfolio in IHT-adjusted terms.

This is a powerful way to reframe your client conversations, as it shows that higher growth does not automatically mean a higher legacy. In fact, time horizon matters as much as risk appetite in these scenarios, due to the fact that IHT can materially delay the point at which conventional investments come out ahead.

For older clients, or those already thinking in terms of estate planning rather than accumulation, this difference in timing can be critical.

The potential impact on vulnerable customers

Another important aspect of this conversation is the potential impact on vulnerable customers who are seeking estate planning products. As financial planning often happens during times of change, such as divorce or bereavement, advisers should be mindful about the additional strain on vulnerable customers, such as retirees and recent widows/widowers, as they are forced to grapple with a complex and distressing new environment.

In these scenarios, framing conversations clearly around objectives, and supporting their new reality is key. At the outset of any such client relationship, advisers should also consider any additional appropriate measures, that they can implement to offer support.

Important considerations

As always, Business Relief investing is not without risk. Returns are not guaranteed, portfolios can fall in value, and BR qualification depends on legislation remaining in force. Liquidity, diversification and suitability remain central to any recommendation.

However, when used appropriately, BR can offer advisers a way to align investment strategy with estate planning outcomes — especially in a post-Budget environment where “doing nothing” is increasingly costly.

Planning ahead matters more than ever. While estate planning can be challenging to navigate, taking appropriate steps to mitigate the effects of these changes can make a big difference to the legacy you’re able to pass on to your loved ones.

For Financial Advisers only

Issued in the UK by TIME Investments (‘TIME’) which is the trading name of Alpha Real Property Investment Advisers LLP, registered address 80 Strand, London, WC2R 0DT, which is authorised and regulated by the Financial Conduct Authority. More information available at https://time-investments.com. Issued May 2026