Aneeka Gupta, director of macroeconomic research at WisdomTree, looks at how the return of El Niño could affect global food production and agricultural commodity markets.

The last time a major El Niño hit (2023–2024) markets were watching. Cocoa rallied 250%[1]. Sugar hit its highest price in over a decade[2]. Rice exporters shut their borders[3]. Those events felt dramatic at the time, but they unfolded before the US Iran war, before the fertiliser crunch, before the warming baseline had climbed another notch.

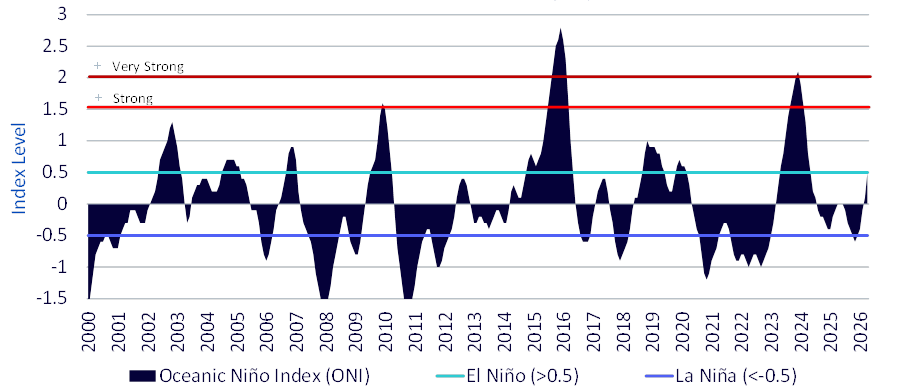

The US National Oceanic & Atmospheric Administration (NOAA) has now confirmed El Niño is back, and the signal is strengthening. The Oceanic Niño Index which represents the three-month running average of sea surface temperatures in the east-central Pacific, is trending toward what forecasters describe as a strong or very strong event. NOAA has assigned a 63% probability of a ‘very strong’ El Niño. On its own, that would already be worth watching. Layered on top of the Strait of Hormuz disruption, which has throttled fertiliser flows from the Middle East at precisely the moment farmers need to be securing inputs, this event arrives at a moment of unusual fragility for global food production.

Figure 1: Oceanic Niño Index (ONI)

Not your average weather event

El Niño is a recurrent climate phenomenon, but its effects are not static. The mechanism is well understood. Trade winds weaken, warm water pools in the central and eastern Pacific, and weather patterns reorganise across much of the globe. Drought where monsoons should fall. Flooding where skies are usually dry. Heat stress arriving weeks early in critical growing regions. The 1997–98; 2015–16 and 2023-24 episodes each left significant marks on agricultural output and commodity prices.

What is different now is the baseline on which this event is unfolding. The past 11 years are the warmest on record. The Intergovernmental Panel on Climate Change (IPCC) is clear that every additional degree of warming raises both the likelihood and the severity of extreme weather events, not just their frequency. The World Meteorological Organisation (WMO) notes that El Niño Southern Oscillation (ENSO) events now occur in a warmer atmosphere and a warmer ocean. That means soils dry out faster, evapotranspiration rates are higher, and crops hit water-deficit conditions earlier in the growth cycle.

Crucially, El Niño’s impact on agriculture does not arrive immediately. The most acute effects tend to lag the event peak by six to twelve months, meaning the pressure on crop cycles and food prices is still building.

Which commodities are likely to be impacted

El Niño does not hit everywhere equally. The geography matters enormously.

South and Southeast Asia carries the heaviest exposure. Weaker monsoon rainfall and above-normal temperatures are the classic El Niño signature for this region, with direct implications for rice, sugar and coffee. Indian and Thai rice production has declined sharply in prior strong events, and there is a real risk that supply stress brings export restrictions back into play, tightening global balances further.

West Africa faces variable rainfall, intensified Harmattan winds and periodic heat stress. As was the case in 2023/24, cocoa crops could decline. Since the start of the crop year last October, arrivals at Ivory Coast’s ports totalled 1.883mn tons, an 18% increase versus the same period last year. However, the increase could decline over the coming weeks. Cocoa farmers in the Ivory Coast are reporting above average rainfall which could lead to flooding and diseases, impacting the mid-harvest which runs through August. Cocoa is a perennial tree crop. Unlike wheat or corn, you cannot plant your way out of a bad season in 90 days. Damage accumulates across years.

Australia is expected to see planted wheat area fall sharply, with production potentially down approximately 9mn tonnes in 2026/27[4], a significant reduction for one of the world’s major wheat exporters. The already tightening wheat market could face further pressure if crop losses materialise in Australia. In the past, El Niño has likewise brought excessive heat and drought towards the end of the year.

Not every region faces the downside. Argentina is one of El Niño’s few structural beneficiaries, with above-average rainfall typically supporting soybean, corn and wheat output. Parts of the southern United States also tend to see improved growing conditions. These are real counterweights but they are unlikely to fully absorb what Asia and Africa may give up.

| Region | Typical El Nino Impact | Commodity exposure | Impact on Growing Conditions | Price Impact |

| South & Southeast Asia | Hotter and drier conditions, weaker monsoons | Rice, Sugar, Palm Oil, Coffee | Negative | |

| Australia | Drier and Hotter Weather | Wheat, Livestock, Sugar | Negative | |

| Southern Africa | Drought | Livestock, Maize | Negative | |

| West Africa | Variable Rainfall, Heat Stress | Cocoa, Coffee | Negative | |

| Argentina | Wetter growing conditions | Soybeans, Corn, Wheat | Positive | |

| North America | Wetter conditions in the South, Milder winter in the north | Grains and Oilseeds | Mixed | |

| Europe | Typically near to slightly wetter | Wheat | Small/indirect impact |

Why soft commodities have historically been sensitive to El Niño

Historically, soft commodities have often shown heightened sensitivity. Soft commodities have consistently been the strongest performers during El Niño episodes, three of the five soft commodities (cotton, coffee, and sugar) moved to multi-year highs in 2022–23, and in late 2024 orange juice and cocoa reached record highs while coffee reached a record high in 2025[5]. Every strong El Niño in the past 55 years has reduced global cocoa production[6], with Ecuador and Indonesia the most exposed origins and significant risks in West Africa (where most of the world’s production is now concentrated).

Conclusion

El Niño has historically moved agricultural commodity prices. What makes 2026 different is the environment it is walking into. A warming baseline that amplifies weather impacts, a geopolitical disruption that has already weakened the fertiliser supply chain, and biofuel demand competing more aggressively with food uses for the same underlying commodities.

The investment case is not that every agricultural market will rise. It is that the distribution of outcomes has shifted. The balance of risks could favour higher prices for several key soft commodities, and some of the risks may not yet be fully reflected in market pricing. Perennial crop deficits in cocoa and coffee appear increasingly structural rather than cyclical. Sugar’s exposure to the ethanol diversion story may create tighter downside protection than raw stock levels suggest. Wheat and corn carry more resilient global inventory positions, but regional disruptions, particularly in Australia and South Asia, remain capable of generating significant volatility.

1 Source: Macrobond, June 2026.

2 Source: Barchart, 21 January 2024.

3 Source: US Department of Agriculture Economic Research Service, 18 October 2023

4 Source: United States Department of Agriculture as of 29 May 2026.

5 Source: Bloomberg Finance L.P. as of 31 March 2026.

6 Source: WisdomTree, International Cocoa Organisation, June 2026.