Mobeen Tahir, Associate Director, Research, WisdomTree explores if there is coherent way to think about the equity markets and outlines a potential strategy for investing in equities this year

“We have just concluded a tumultuous year for asset markets. In March, equities endured volatility reminiscent of levels previously seen during the global financial crisis. What followed thereafter was an equity rally that many touted as being disconnected with the economic reality. The recovery in markets, however, was not evenly distributed and returns were not stellar across the board. While the NASDAQ Composite Index was up over 43% last year, the Euro Stoxx 50 Index ended the year down 5%[1] (in USD and EUR respectively).

“Investors are intrigued by the possibilities and opportunities in the year ahead. Was the strength in the tech sector transient or will the dominance continue? Are we going to see a reincarnation of value after the challenges faced by a multitude of sectors last year? And most importantly, how do all the different pieces come together?

“Here we offer one approach for conceptualizing these problems and developing a cohesive example framework for investing in equities this year. Every investor should make their own decision in establishing their investment needs and constraints to determine how this, or any other framework, can aid their decision making.

The proposed framework

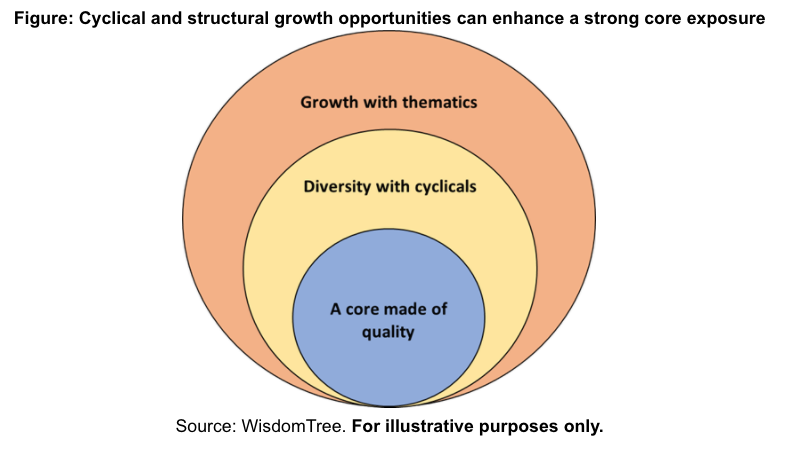

The framework is comprised of three key components (see figure below) which together add diversity and balance. Each component has an important role to play.

A core made of quality:

“Quality is an ‘all-weather’ factor that promises balance i.e. the ability to protect against market downturns without foregoing participation in the upside. ‘Quality’ refers to strong and stable businesses that are profitable and typically have relatively low leverage. This enables them to better withstand downside shocks. Since such businesses can exist in any sector, quality does not cause the core of the portfolio to lose its diversity if it supplements or replaces a pure beta exposure.

“With many major economies including the US and those in Europe still reeling from the pandemic, the desired economic recovery this year cannot be anticipated entirely without perils. Bankruptcy, in the face of economic challenges, remains one of the key risks facing businesses in the year ahead. Those companies that entered the pandemic with a strong balance sheet and have stayed profitable enough through the ordeal, make a case to constitute the core exposure.

Diversity with cyclicals:

“Pockets of the global equity market that are poised to benefit from an economic upswing, that may already have started or is impending depending on where you look, can add diversity and growth potential to the portfolio. Numerous avenues can be explored within this component.

“Small caps are one of those avenues. Small-cap stocks typically have a high beta with the underlying economy. The buoyancy in stock markets since vaccine news took center stage in November has helped small caps outpace large caps in various markets, e.g. the Russell 2000 Index has overshadowed the S&P 500 Index since the start of November[2]. As the economic recovery gathers steam, small caps are likely to pick up pace too.

“The notion of ‘diversity’ in equity markets is almost incomplete without emerging markets, particularly China. The country’s success in overcoming the pandemic and swiftly putting its economic recovery on track stands in stark contrast with other major economies. China has recently reiterated its growth ambitions with a new five-year plan and is reaffirming its global stature through trade and investment deals with partners in the Asia Pacific region as well as the European Union. China’s strength is expected to permeate into emerging markets more broadly which may find additional support from a weak US dollar. ‘Value’, if defined as businesses or sectors that have faced headwinds from the pandemic and the resulting economic downturn, have an improving outlook as we emerge from the crisis. Within this framework, whether value will outperform growth is not a critical question as the two can coexist in separate buckets.

Growth with thematics:

“The notion of growth is increasingly shifting away from stocks with positive momentum to businesses that align more closely with megatrends. Structural shifts in markets offer investment opportunities that promise growth and offer a potentially longer shelf life. Investors appear to be placing their faith in such themes as they are built on the principle of ‘market-creating innovation’, i.e. a process that creates new demand which stems from doing things that have not been done before.

“Tech-related themes fall neatly within this bracket because of the innovation they bring and how they continue to positively disrupt the status quo. The advent of the smartphone just over a decade ago created a whole new economy of applications and instilled growth which would have been difficult, if not impossible, to foresee. For this reason, future innovation becomes challenging to price in and comes as a positive surprise when it happens. Growth potential is also why markets might not necessarily anguish over elevated valuation multiples for the tech sector. In some cases, like Tesla, the valuation multiples may even be absurd and defy conventional finance wisdom.

“Many investors who sought such themes last year reaped attractive rewards, e.g. some cloud computing strategies more than doubled in value over the year. The growing interest in thematic investing is therefore unlikely to be transitory and may accelerate as a trend itself this year. Having a thematic component in the example framework to complement the core and the diversifiers can add an exciting element of growth potential.

Conclusion

“How to weight the different components and how the equity allocation fits within a broader portfolio are all important considerations for an investor to make. The framework illustrated here is a first step in that discussion and should help synthesize an equity strategy in a year that might present many opportunities for investors.”