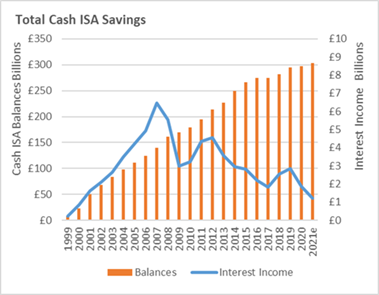

The Cash ISA was introduced in April 1999, by the end of 2000 the total Cash ISA balance stood at £22.2bn, by the closes of 2020 the UK’s cumulative cash ISA balance stood at £297bn.

The median Cash ISA balance in 2000 was £1000, in 2020 it was £11,842.

Despite these increases, the interest income grew from £41.22 in 2000 to just £47.85 in 2020. In the same time frame, the 20% tax relief has gone from £8.24 to £9.57.

James de Sausmarez, Director and Head of Investment Trusts at Janus Henderson Investors said: “Nobody will be popping the champagne to celebrate all the tax they’ve saved on their cash ISAs this year, not least because the tax relief wouldn’t even pay for half a bottle.”

Bank of England data shows variable rate ISAs earn 0.35% including any bonus, and fixed rates for the year will earn 0.49% – these are the lowest rates ever since ISAs were introduced.

Banks, building societies and NS&I will pay cash ISA savers just £1.22bn this year, the lowest since 2000.

Janus Henderson Investors compared the interest made in cash ISAs to the same amount put into UK equity investment trusts over 2020.

If the average cash ISA were transferred into the average UK equity income investment trust, it would earn dividends of £486.04, and save its owner £97.21 in income tax.

James de Sausmarez suggested banks are giving a clear signal – they simply do not want any more cash deposits, Sausmarez continued, “when someone sends a message this loadly it pays to listen.”

Sausmarez emplores savers to turn to investment trusts. He concluded, “If you had invested £1000 in the average investment trust in December 1999 and reinvested your dividends, you would now have a holding worth £5,755, without ever adding another penny. If you’d saved the same £1000 in cash, you would only have £1,705 today.”