IFA Magazine’s latest survey analysis [i] offers a clear snapshot of how UK advisers are approaching fixed income in today’s uncertain market environment. The findings reveal a profession that remains confident in fixed income’s role, but increasingly selective and client-led in how it is used. Matt Williams, Content Editor at IFA Magazine, brings you the details, covering balancing income needs, inflation concerns and interest rate uncertainty with a more nuanced, case-by-case approach.

The majority of respondents to the survey were financial advisers (69%), with investment managers accounting for 13%, wealth managers 7% and paraplanners 3%. Together, their responses paint a picture of how fixed income is currently viewed across UK client portfolios.

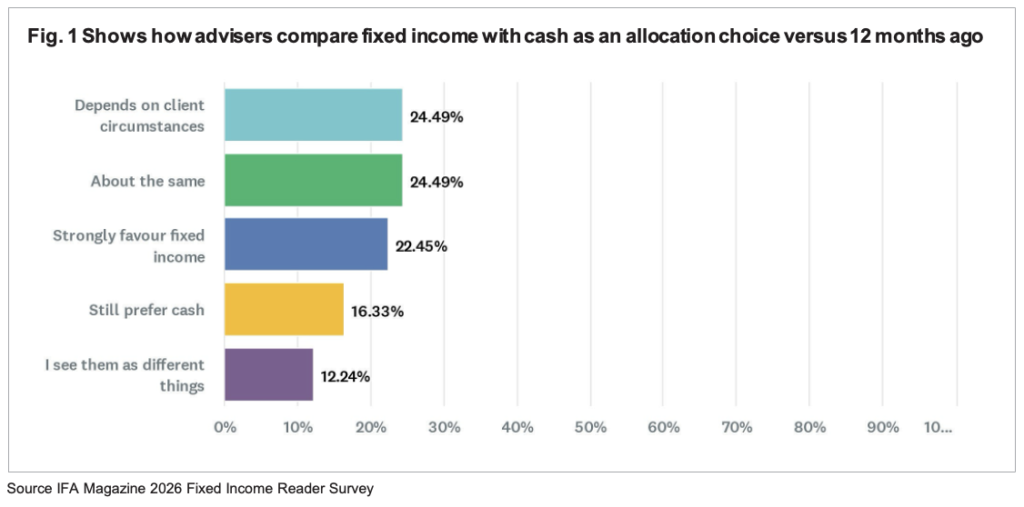

Fixed income versus cash

When asked to compare fixed income with cash as an allocation choice relative to 12 months ago, opinions were noticeably split. As shown in Fig. 1, just under a quarter (24.5%) said the balance between the two remains largely unchanged, while an identical proportion said the answer depends entirely on individual client circumstances.

That is reflected elsewhere in the results. While 22% now strongly favour fixed income over cash, 16% still prefer cash as an allocation choice. A further 12% view the two as entirely different tools, each serving distinct portfolio objectives.

This range of views suggests that rather than a unanimous shift away from cash, advisers are increasingly weighing needs on a case‑by‑case basis.

Allocations remain moderate

Fixed income allocations within balanced portfolios remain measured, reflecting a disciplined and considered approach from advisers. The most common allocation range reported was 11–25%, according to 39% of respondents, closely followed by 26–40% at 35%, suggesting a solid core role within portfolios.

At the lower end, 18% said fixed income makes up just 0–10% of a typical balanced portfolio, while a smaller group is leaning more heavily into the asset class, with 6% allocating 41–60% and 2% allocating more than 60%.

Looking back over the past year, the majority of advisers (61%) said their clients’ exposure to fixed income has remained broadly stable. However, there are clear signs of renewed momentum, with almost a quarter (24%) reporting increased allocations, compared with 14% who have reduced exposure.

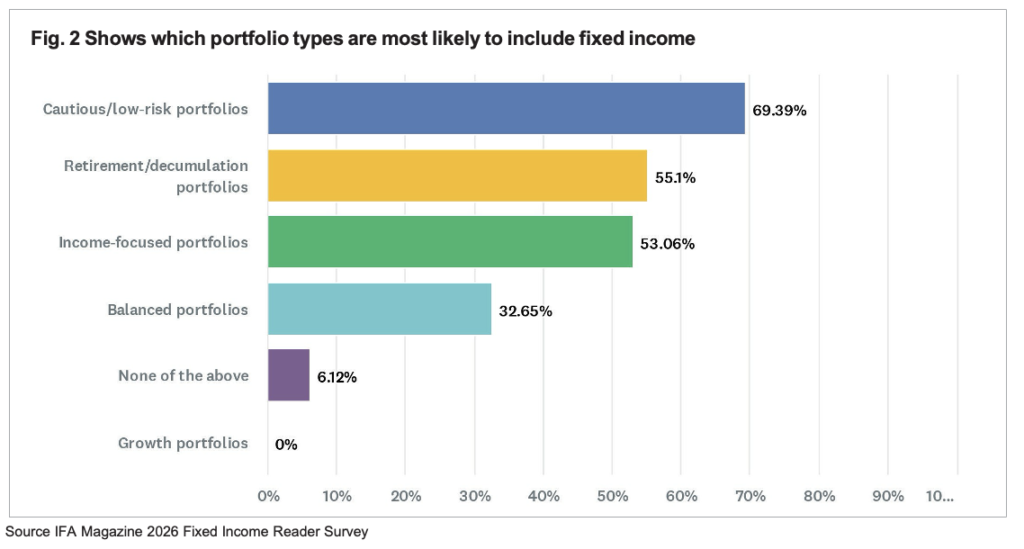

Fixed income continues to play a particularly important role in more defensive and outcome-focused strategies. As you can see in Fig. 2, the majority (69%) highlighted cautious or low-risk portfolios, followed by retirement or decumulation portfolios (55%) and income-focused portfolios (53%). Meanwhile, 33% also incorporate fixed income within balanced portfolios, underlining its versatility across a wide range of client needs.

The core attractions of fixed income

When it comes to why advisers use fixed income, traditional benefits continue to dominate. Portfolio diversification was the most common appeal, selected by 55% of respondents. Capital preservation followed closely at 53%, reinforcing fixed income’s enduring role within portfolios.

Attractive yield levels were highlighted by 27%, while 16% pointed to the predictability of returns. A further 10% cited an improved risk‑adjusted return outlook as a reason for using fixed income more widely.

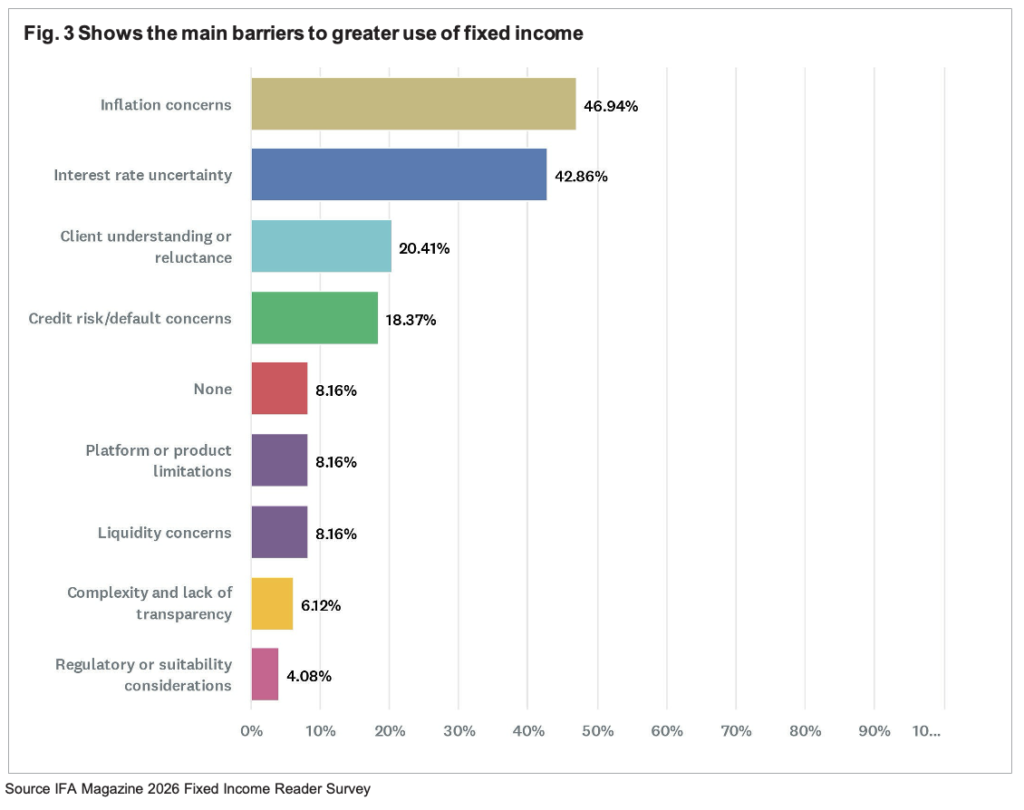

However, our adviser audience still harbours some concerns. According to Fig 3, 47% identified inflation as the biggest barrier to greater fixed income use, while 43% pointed to ongoing interest rate uncertainty. Client understanding and reluctance were cited by 20%, and 18% suggested concerns over credit risk and default. Other barriers mentioned included liquidity issues, complexity, lack of transparency and product limitations.

How advisers are accessing fixed income

In terms of implementation, advisers clearly favour diversified structures. Dedicated fixed income funds (OEICs or unit trusts) were the most commonly used vehicle, selected by 56% of respondents.

Alongside this, 31% said they use model portfolio services or other outsourced solutions, while 29% rely on multi‑asset funds to provide fixed income exposure. ETFs are also gaining traction, used by 24%, while 22% invest via direct bonds. Investment trusts and companies were used by 16%.

When choosing between active and passive strategies, the preferred approach is balanced (Fig. 4). 44% of those surveyed favour a blend of active and passive, while 29% lean towards active strategies, whereas a purely passive approach is the ideal solution for 11%.

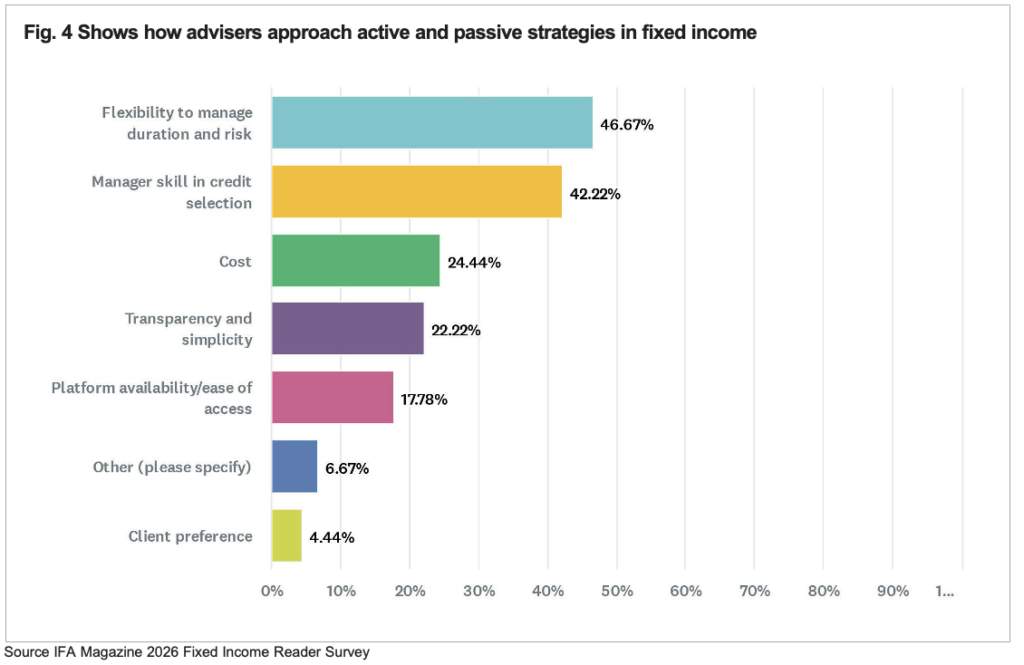

The decision between active and passive is driven primarily by flexibility and expertise, as seen in Fig. 5. Almost half (47%) pointed to the ability to actively manage duration and risk, while 42% noted that manager skill in credit selection makes a big difference. Cost was a key consideration for 25%, while transparency and simplicity influenced 22%. Platform availability and ease of access were mentioned by 18%.

Confidence remains high

Encouragingly, advisers appear confident in their understanding of fixed income dynamics. 51% described themselves as fairly confident, while 18% said they are very confident.

In terms of any concerns, the most common cause for concern is understandably the geopolitical instability, according to 36%. This is followed by heightened inflation at 27%, extended periods of high interest rates at 20%, and rising corporate defaults at 9%.

Advisers were also asked how geopolitical developments affect their approach to fixed income. Almost half (49%) said they become more cautious due to inflation and interest rate risks, while 27% believe such conditions increase the need for selective and active management. Just 7% said geopolitical risks make them more positive, and 17% reported no change to their approach.

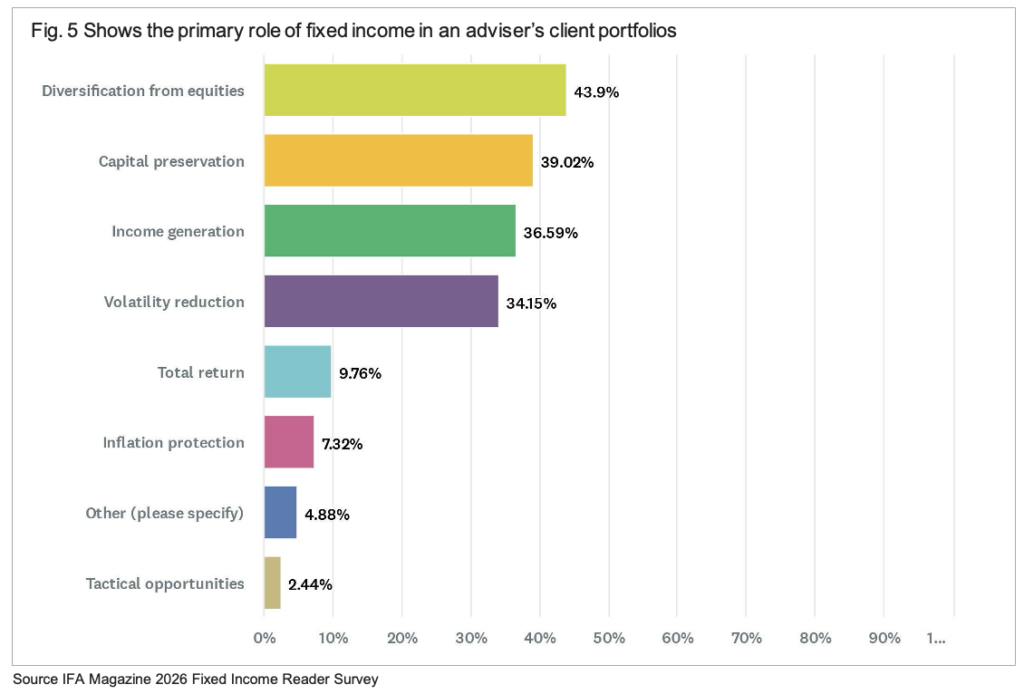

The evolving role of fixed income in portfolios

When asked to define the primary roles of fixed income, diversification from equities came out on top (Fig. 5), according to 44% of respondents. Capital preservation followed closely at 39%, while 37% highlighted income generation. A further 34% pointed to volatility reduction as a key risk.

Other considerations were less prominent but still relevant. 10% cited total return objectives, 7% pointed to inflation protection, and 2% said tactical opportunities play a role.

Looking ahead, advisers are most likely to increase fixed income exposure when clients need predictable income (49%) or when yields rise (41%). Approaching retirement was also a key factor according to 34%, while periods of heightened equity volatility (32%) and rising recession risks (22%) were additional catalysts.

Trusted providers and the impact of geopolitics

When asked which firms they trust most to deliver fixed income solutions, Royal London Asset Management topped the list, featuring in the top five of 44% of respondents. L&G followed at 37%, with M&G Investments and Vanguard both cited by 27%. BlackRock rounded out the top five at 20%.

In conclusion

Overall, the findings suggest that fixed income is being approached with discipline. Advisers clearly value its role, but remain highly conscious of uncertainty, especially surrounding inflation, rates and geopolitical tensions. While fixed income might not be making dramatic claims on portfolios, it is very much seen as an essential part of the conversation.

This feature was part of our 2026 Fixed Income Insights. For deeper analysis on bond markets and rates strategy for advisers, explore IFA Magazine’s latest Fixed Income Insights publication.

[i] About the Survey. Important Information; “Adviser perspectives on fixed income investments”: IFA Magazine’s 2026 Adviser Survey was carried out online from 5th March – 13th April and gathered 72 responses.