Russ Mould, investment director at AJ Bell, looks at how the war in the Middle East has knocked the FTSE 100 into correction territory and sharpened concerns about inflation, interest rates and the outlook for equities.

AJ Bell investment director, Russ Mould, comments:

“The FTSE 100’s closing all-time high of 10,911, reached on 27 February, the day before war broke out in the Middle East, is more than 10% away at the time of writing, to signify that the UK’s headline stock market index is now officially in ‘correction’ territory. From the narrow perspective of financial markets, the war has (at least) three potential implications:

- First, any sustained increase in oil and gas prices could stoke fears of inflation, and in turn drive up interest rates, in a repeat of the oil shocks of the 1970s and, to a lesser degree, 2022.

- Second, higher interest rates could prompt an economic slowdown or recession, and hit near-term corporate earnings, albeit in exchange for putting a lid on inflation and the long-term damage that causes.

- Finally, higher interest rates might affect equity valuations in two ways. One is that higher interest rates mean higher discount rates in discounted cash flow (or DCF) models, and that in turn is potentially a challenge for the valuations attributed to growth stocks, such as technology companies. The other is that increased bond yields can lessen the relative attraction of equities compared to fixed income as a source of yield.

“This mathematical thought process helps to explain the FTSE 100’s March retreat, even as economists, analysts and investors cling to the hope that the war will be a short one for so many different reasons, while analysts’ forecasts are yet to reflect a hit to company profits or dividends.

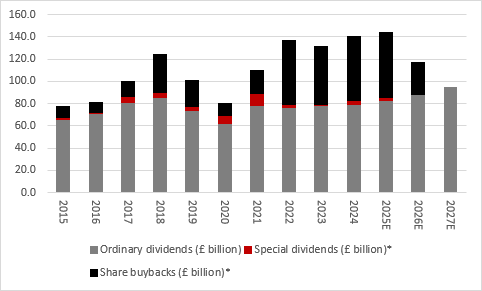

“Forecasts for aggregate FTSE 100 dividend payments for 2026 are up slightly over the last three months, at £88 billion compared to £86 billion in December, and 2027 estimates are a fraction higher than at the turn of the year as well. As a result, consensus analysts’ estimates suggest that 2018’s all-time high FTSE 100 dividend payment of £85.2 billion will finally be exceeded in each of this year and next.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts. *Announced in aggregate as of 18 March 2026.

“Share buybacks could yet supplement this total. The FTSE 100’s members have already declared cash returns worth £29.4 billion via this mechanism for 2026. Add that to the forecast dividend and the total cash return from the FTSE 100 is currently expected to be £117.4 billion in 2026, or 4.4% of the FTSE 100’s total £2.7 trillion stock market valuation. That cash yield beats inflation and the Bank of England base rate but not the 10-year gilt yield, which, at 5% at the time of writing, stands at its highest level since 2008 thanks to inflation worries.

“That cash yield may therefore not look quite as certain as it did a year ago. As of March 2025, FTSE 100 firms had already outlined buyback plans worth £38.9 billion. HSBC, Intertek, NatWest, Centrica and BP have all flagged pauses in their buybacks, for company-specific reasons, and a worsening macroeconomic outlook could yet prompt other firms to reassess their buyback schemes.”

Profit forecasts show welcome resilience

“One potential warning sign for forecast dividends and buyback declarations would be a drop in corporate profit forecasts. Any sustained increase in oil and gas prices would be a danger, given the impact on profit margins thanks to higher input costs and also potentially revenues for many industries if consumers feel obliged to spend less on discretionary items because they are forced to lay out more to cover bills.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts. Data as of 18 March 2026.

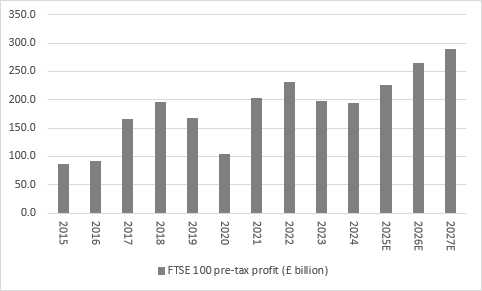

“The good news is that profit forecasts are not showing any strain yet. In the first three months of this year analysts have actually upgraded their profit forecasts for 2026 and 2027. Each year is expected to set a new all-time high for pre-tax income, at £264 billion in 2026 and £288 billion in 2027, well ahead of 2022’s peak of £231 billion.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts. Data as of 18 March 2026.

Dividend growth still very concentrated

“For income-seekers, the FTSE 100’s yield may be a key part of the UK stock market’s appeal, but investors must be aware of how the forward yield is lower than in the past few years, owing to the strong gains made by the index this decade, right up to the end of February. Quite simply, the index has gone up faster than dividends, so the available dividend yield has contracted.

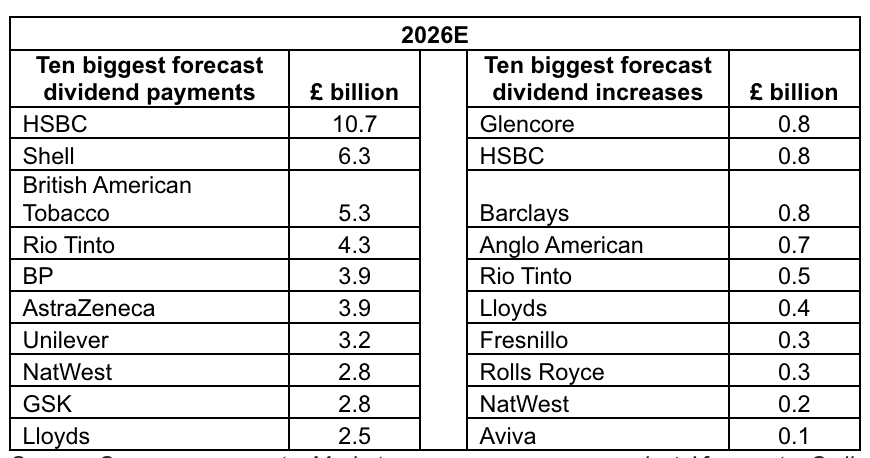

“There also remains a fair degree of concentration risk within the UK’s headline index. Just 10 companies are expected to pay out 52% of the forecast total for 2025, at £45.7 billion, while the top 20 are expected to chip in £60.8 billion, or 69% of the estimated total.

“The top 10 list includes three stocks in the Banks sector and two apiece from Oil, Pharmaceutical and Consumer Staples sectors, as well as one from Mining.”

Source: Company accounts, Marketscreener, consensus analysts’ forecasts. Ordinary dividends only. Data as of 18 March 2026.

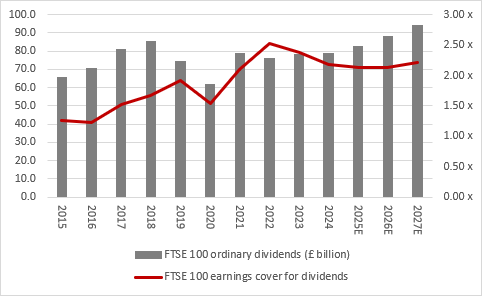

Dividend cover remains above two

“Those investors who are of a nervous disposition may look to earnings cover for the FTSE 100’s aggregate forecast dividend.

“For 2026 and 2027, analysts see earnings cover coming in at 2.14 times and 2.21 times, respectively. This is not as high as 2022’s reassuring 2.55 times, but it does still exceed 2.00 times, the mark traditionally seen as one that offers comfort and protection in the event of any unforeseen economic setback.

“Even so, there have been 132 dividend cuts across the FTSE 100 in the past decade. More than half of those may have hailed from the Covid-19 blighted years of 2019 and 2020, but both Mondi and Diageo have cut their dividend already this year.

“As a result, investors will need to keep checking earnings cover and free cash flow cover, as well as balance sheets and interest cover in the profit and loss account, as part of their research to check out how secure dividends may be in the event of any unexpected economic downturn, oil-related or otherwise.”

Source: Company accounts, Marketscreener, consensus analysts’ forecasts. Data as of 18 March 2026.

Many dividend yields compare less favourably to gilts

“For the second quarter in a row, the life insurers Legal & General and Standard Life (Phoenix Group, as was) offer the highest forecast dividend yields within the FTSE 100.

“In fact, the 10 highest dividend yields on offer within the FTSE 100 all come from financial services companies or real estate plays. They represent 9% of the index’s total forecast dividend payment for 2026.

“A sustained increase in the 10-year gilt yield could tempt some investors to look toward government bonds and away from equities in their search for reliable income, although they will still need to consider the danger posed by inflation to the real-terms value of gilt coupons and weigh up the potential for capital gains from stock markets, as well as dividends.

| 2026E | ||||

| Company | Dividend yield (%) | Dividend cover (x) | Pay-out ratio (%) | Cut in last decade? |

| Legal & General | 8.8% | 1.44 x | 69% | No |

| Standard Life | 8.2% | 0.67 x | 149% | 2016, 2018 |

| Land Securities | 7.0% | 1.79 x | 56% | 2019 |

| M&G | 6.9% | 1.17 x | 85% | No |

| LondonMetric Property | 6.7% | 1.51 x | 66% | No |

| British Land | 6.5% | 2.06 x | 49% | 2019, 2020 |

| Aviva | 6.4% | 1.23 x | 81% | 2019 |

| NatWest | 6.1% | 1.98 x | 51% | 2019 |

| ICG | 5.9% | 1.98 x | 51% | No |

| Tritax Big Box REIT | 5.5% | 2.32 x | 43% | 2020 |

| AVERAGE | 6.8% | 1.61 x | 62% | |

Source: Company accounts, Marketscreener, consensus analysts’ forecasts, LSEG Refinitiv data. Based on ordinary dividends only. Data as of 18 March 2026.

“A further rule of thumb states that any dividend yield which exceeds the risk-free rate by a factor of two may turn out to be too good to be true. The 10-year gilt yield is a good proxy for the risk-free rate. A dozen years of interest rates at near zero rendered the rule pretty useless but now monetary policy is returning to something akin to ‘normal’ it may regain some of its former relevance.

“For the record, not one FTSE 100 stock currently offers a forecast dividend yield of 10% or more, or twice the 5% 10-year gilt yield that prevails at the time of writing, and that is probably no bad thing.”

Who are the serial dividend growers?

“A really fat dividend yield is not necessarily a good sign anyway, as it can mean that investors are demanding such a juicy return to compensate themselves for what they see as substantial risks at a company, either in terms of its business model, balance sheet or boardroom acumen. The list of FTSE 100 firms which, on paper, were offering a 10%-plus dividend yield only to then deliver nothing of the sort as investors’ worst fears were realised is not a short one, and over the past decade it includes Centrica, Marks & Spencer, Shell, Imperial Brands, Persimmon and Vodafone.

“If anything, history suggests it is dividend growth that is the real secret sauce for a share price, as a growing pay-out will drag it higher over time.

“After the delisting of Ashtead (or Sunbelt Rentals as it is now, following its primary list switch to the USA), and demotion to the FTSE 250 of Hikma Pharmaceuticals, 16 FTSE 100 members are nurturing an unbroken dividend streak of a decade or more. Coca-Cola HBC is the latest entrant to this hallowed grouping. Severn Trent and LondonMetric Property are also closing in as they can point to nine consecutive increases each.

“This grouping has, on average, provided premium capital returns and total returns relative to the FTSE 100 – 11 of the 16 have generated premium capital returns and 10 have done so in terms of total returns (including dividend reinvestment). However, the number of underperformers has increased in the past two to three years, as previously highly valued stocks such as Croda, DCC and the now-demoted Hikma have suffered a de-rating, to show that valuation really does matter in the end.

“Moreover, only half of the 16 could be found in the FTSE 100 a decade ago. Any investor looking for the next generation of dividend growth winners may therefore need to dig into the FTSE 250 (or below).”

| Total return | Dividend CAGR | Dividend | Growth | ||

| 2016-26 | 2016-25 | 2026E | 2027E | ||

| 1 | Diploma | 781.3% | 13.1% | 5.0% | 5.0% |

| 2 | ICG | 476.2% | 14.2% | 6.0% | 5.4% |

| 3 | Halma | 374.7% | 7.2% | 9.5% | 6.9% |

| 4 | Scottish Mortgage | 308.2% | 4.8% | 5.3% | 7.0% |

| 5 | London Stock Exchange | 279.8% | 15.3% | 9.2% | 12.3% |

| 6 | F&C Investment Trust | 228.8% | 5.6% | 5.4% | 4.3% |

| 7 | RELX | 221.3% | 8.6% | 7.4% | 8.2% |

| 8 | Coca-Cola Hellenic Bottling | 218.2% | 14.4% | 10.1% | 9.8% |

| 9 | Alliance Witan | 212.5% | 9.9% | 2.4% | 3.4% |

| 10 | Spirax Group | 160.3% | 9.4% | 5.2% | 7.0% |

| 11 | SEGRO | 120.2% | 7.1% | 5.5% | 4.9% |

| 12 | Sage | 119.5% | 5.2% | 6.8% | 6.8% |

| 13 | British American Tobacco | 118.2% | 4.5% | 2.0% | 6.0% |

| 14 | United Utilities | 101.0% | 3.4% | 3.0% | 2.5% |

| 15 | Croda | 24.9% | 4.9% | 1.4% | 3.6% |

| 16 | DCC | 11.0% | 9.6% | 3.9% | 4.0% |

| AVERAGE | 234.7% | 8.6% | 5.3% | 5.8% | |

| FTSE 100 | 127.1% | 3.3% | 6.6% | 7.0% |

Source: LSEG Refinitiv data, company accounts, Marketscreener, consensus analysts’ forecasts. Ordinary dividends only. Data to 18 March 2026.

DIVIDEND DASHBOARD EXPLAINED:

Each quarter, AJ Bell takes the forecasts for the FTSE 100 companies from all the leading City analysts and aggregates them to provide the dividend outlook for each company and the entire index. The data relates to the outlook for 2026 and 2027. Data correct as of 18 March 2026.