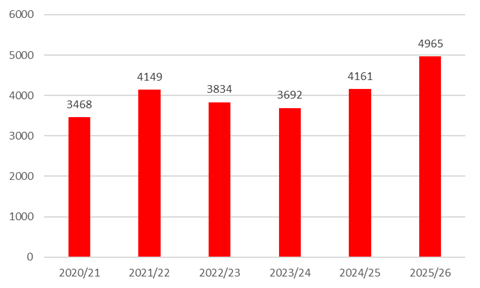

HM Revenue & Customs (HMRC) opened 4,940 formal Inheritance Tax (IHT) enquiries in 2025/26, an 18 per cent increase over the previous year, and the highest number in six years, according to data obtained by Price Bailey, the chartered accountants.

Price Bailey explains that HMRC can open a formal enquiry when it believes there is a risk that an IHT return may be incomplete or inaccurate. The process gives HMRC wide powers to request documents, valuations, correspondence and explanations from executors or advisers.

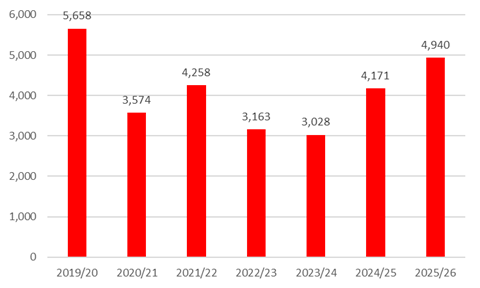

HMRC’s risk assessors also referred 4,965 IHT returns to the compliance team in 2025/26, the highest number in five years. This is an upstream triage stage, distinct from a formal enquiry. Referrals to the compliance team can lead to no action, a minor amendment, or a formal enquiry.

Price Bailey points out, however, that the proportion of IHT returns referred to the compliance team that result in amendments has continued to fall. In 2025/26, just 40 per cent of compliance checks referred by risk assessors led to an amendment, down from 45 per cent in 2024/25 and well below the levels seen during the pandemic era (for example, in 2020/21, 83 per cent of IHT accounts referred to compliance were subsequently amended). This suggests HMRC is casting the net more widely but with diminishing returns.

Nikita Cooper, Director at Price Bailey, comments: “HMRC is coming under increasing pressure to clamp down on non‑compliance and boost the tax take. IHT was historically a very small component of HMRC’s overall revenues, but many more estates are being caught in the tax net every year, so it is becoming a higher priority for HMRC.”

“For taxpayers, a formal enquiry can mean months of additional work at a time of bereavement. The process can entail providing detailed evidence of asset values, lifetime gifts and relief claims. Crucially, many formal enquiries do not lead to any additional tax, but they still impose a significant administrative and emotional burden on families who have already complied with the rules.”

She adds: “HMRC is becoming less discriminating as it casts its net wider. Just 40 per cent of compliance checks resulted in any amendment to returns, which suggests that the customer compliance team needs to take a more targeted approach. This is unfair on the taxpayers who are coping with bereavement and are doing the right thing by making full and accurate disclosures.”

Number of formal IHT enquiries opened by HMRC

Price Bailey notes that, unlike most other taxes, IHT returns must still be submitted on paper and processed manually by HMRC staff. Only limited data from these forms is digitised, and HMRC does not hold the information in a format that supports modern analytics or AI‑driven risk‑modelling. This severely restricts HMRC’s ability to target enquiries effectively, which helps explain why the strike rate has fallen even as the number of formal enquiries has risen.

Nikita Cooper says: “The IHT reporting system is very archaic, with paper forms being processed manually. By stepping up the number of formal enquiries, HMRC’s strike rate has fallen sharply. The backwardness of the system means that HMRC cannot even tell us how much tax was collected from these enquiries. In an increasing number of cases, the answer is almost certainly nothing.”

According to Price Bailey, the number of staff in HMRC’s Customer Compliance Group has increased significantly in recent years. The declining proportion of amendments to IHT returns suggests, however, that newer staff may be taking time to get to grips with the complexities of IHT, or that HMRC’s risk‑selection models are being applied more broadly.

It also notes that with thresholds frozen and not adjusted for rising property prices and inflation, the number of estates liable for IHT is expected to increase. Impending changes for farmers and business owners—including restrictions to Business Relief and Agricultural Property Relief, and the inclusion of pensions within the scope of IHT from April 2027—will further expand the number of affected estates.

Nikita Cooper concludes: “We are likely to see much greater emphasis on compliance as the number of estates eligible for inheritance tax and the amount collected rises sharply in the coming years. The current paper‑based filing system is already buckling under the strain and HMRC will need to get much better at sifting out inaccurate returns from those who are doing the right thing.”

Number of IHT returns amended by compliance following risk assessment