New analysis from Fidelity International highlights the long-term “opportunity cost” of holding Premium Bonds, with savers potentially missing out on significant growth compared to investing in the stock market.

Premium Bonds remain one of the UK’s most popular savings products, held by around a third of the population. Data obtained by Fidelity from NS&I shows that savers typically hold them for around 10 years, with 850,000 under-16s also owning bonds, often gifted by family members.1

While cash-like assets such as Premium Bonds play an important role in providing financial security and stability, Fidelity’s analysis shows that holding them over long periods can come at a cost.

Holding Premium Bonds too long could cost savers thousands

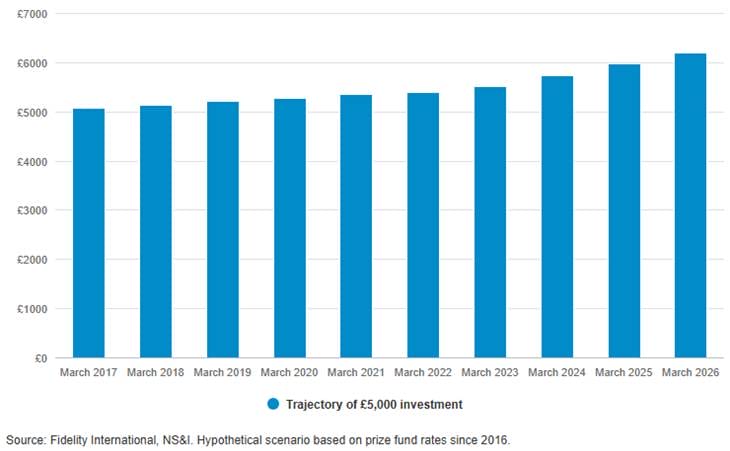

A saver who invested £5,000 in Premium Bonds in 2016 would have seen their holding grow to roughly £6,190 by 2026, based on historic prize fund rates and assuming winnings were reinvested. However, inflation means that £5,000 in 2016 would be worth £6,992 today – leaving the saver worse off in real terms.

This is not an exact science as NS&I’s prize fund rate is not a guaranteed rate of return. Depending on their luck, a saver could have won significantly more – or significantly less.

Premium bonds: return from £5,000 invested in early 2016

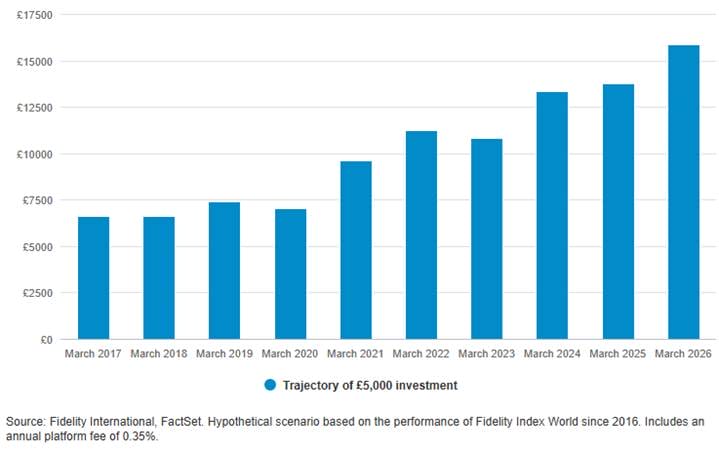

By comparison, investing the same amount in the stock market would have delivered significantly stronger returns. A £5,000 investment in a global tracker fund, such as Fidelity Index World, in March 2016, with dividends reinvested, would have grown to approximately £15,900 over the same period.

World tracker fund: total returns from £5,000 invested in March 2016

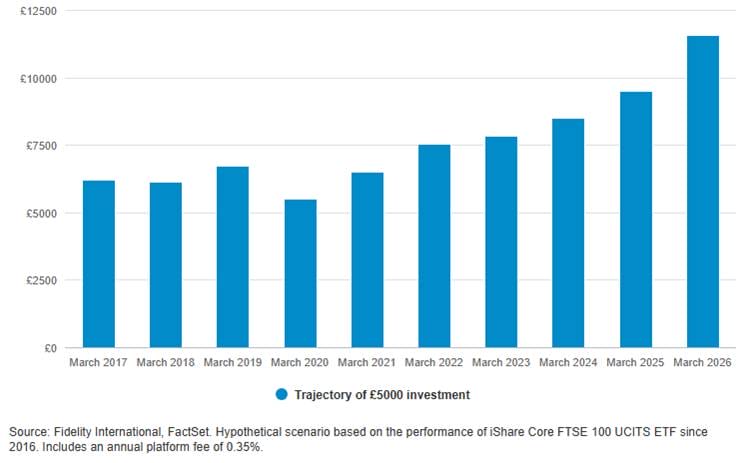

Another option would have been to invest the £5,000 closer to home. A fund that tracks the FTSE 100 – an index of the UK’s 100 biggest listed companies – would have grown your wealth to about £11,600 over the past 10 years.

UK tracker fund: total return from £5,000 invested in March 2016

Jemma Slingo, Pensions and Investment Specialist, Fidelity International, comments: “Premium Bonds can play a useful role in a balanced financial plan. They offer capital security and tax-free prizes, making them a good option for short-term savings or an emergency fund.

“Where savers need to be careful is over longer time horizons. While your money is safe in cash terms, inflation can steadily erode its real value, and returns from Premium Bonds are uncertain as they depend on prize draws. Over time, that can add up to a significant opportunity cost compared to investing.

“This is especially important for children. Premium Bonds are a popular gift, but with such long time horizons, even small amounts invested in the stock market have much greater potential to grow.

“The key is matching your money to your goals. Cash has its place for short-term needs, but for long-term investing, putting money to work in the market gives it a much better chance of keeping ahead of inflation and delivering meaningful growth.”

1Source: The data was obtained from NS&I by FOI request and shows the mean holding period for Premium Bonds purchased on or after 1 January 2005. NS&I does not hold the purchase dates for all Premium Bonds bought prior to 2005 due to a change in banking system.

![[uns] business, handshake, appointment](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/803862-featured-300x200.webp)