As a result of the introduction of Pension Freedoms in 2015, pension savers no longer have to convert their pension pot at retirement to an annuity – an income for life. Since these changes were implemented, annuity sales have slumped and the majority of new retirees either cash out their pension pot in full or move it into a drawdown account to support them through retirement. However, groundbreaking new research from consultants LCP has found that many pensioners should be revisiting that decision later in retirement and could get better outcomes by switching some or all of their savings into an annuity.

The new paper: “Is there a right time to buy annuity” is based on a sophisticated model which compares the happiness a retiree would get at each point in retirement from staying in drawdown compared with switching to an annuity. The model looks at potential outcomes over a range of more than 2,000 different scenarios for future investment performance and life expectancy.

The model takes account of factors such as attitude to risk (allowing for the fact that people generally have ‘loss aversion’ and feel much more dissatisfaction from losing money than they get satisfaction from gaining an equivalent amount) and any desire to have funds at the end to pass on to heirs.

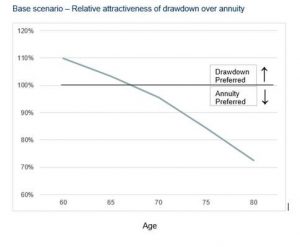

The chart below shows the central result of the paper:

According to the model, someone aged 60 who chooses drawdown is likely to be 10% happier overall than someone who immediately uses all of their pension pot to buy an annuity (see notes to editors for more details about the assumptions made). But as the person gets older, the attractiveness of an annuity increases. At around age 67, the model predicts that the retiree would be happier overall with an annuity, and this effect gets stronger the older they get.

The paper tests the robustness of this finding by varying the assumptions made about the preferences of the individual. A key result is that in all the models tested there is still a ‘crossover’ point where annuities become more attractive, though the age at which this crossover occurs can vary. In particular:

- If an individual is willing to take higher investment risk in their drawdown portfolio, the age at which an annuity becomes more attractive rises; for a 75% equity portfolio, switching to an annuity makes sense at age 70 (compared with age 67 for a 55% equity portfolio;

- If an individual is strongly risk-averse they should move out of drawdown sooner – at age 64 in the version of the model which gives a bigger negative weighting to downside risk, compared with age 67 in the baseline;

- A ‘hybrid’ approach where the individual uses part of their pot to annuitise at 60 and then annuitises the balance later in retirement can generate the best outcomes at all ages. In this case the ‘crossover’ point where the balance of the pot is annuitised would be around age 71.

As the paper explains, one reason why annuities become steadily more attractive is that the uncertainty of life expectancy grows as people get older. In simple terms, it becomes steadily harder to manage the balance of your pension pot in later life in order to make sure you don’t run out of money prematurely or live more frugally than is necessary.

These results raise questions about how the large number of people who have gone into drawdown under pension freedoms might be prompted to reconsider this decision in later retirement. Potential ideas include:

- A mid-retirement ‘MOT’, similar to the mid-life MOT currently being piloted; this would allow individuals to review whether the choices they made at retirement were still appropriate years later;

- Drawdown products which ‘default’ individuals into an annuity at a later age, though with the option to change that decision if circumstances change; this would avoid the need for older retirees to make active choices and should steer most to better outcomes than staying in drawdown;

Commenting on the paper, co-author Steve Webb, partner at LCP said:

“Whilst forcing people into annuities in their late fifties and sixties was not the right approach, it would be wrong to write-off annuities altogether. This powerful research shows that for a wide range of people there could come a point during retirement when a switch to an annuity gives them better outcomes overall. Policy makers need to think how best to nudge people to review their finances not just at retirement but during retirement”.

Phil Boyle, co-author, and partner at LCP said:

“The exact point at which an annuity becomes more attractive depends very much on the individual. Our model suggests that for a wide range of people there is an age beyond which staying in drawdown may not generate the best results. As people get older, their life expectancy becomes more uncertain, and this creates a real headache for manging your pension pot. An annuity takes that uncertainty away”.