The UK General Election on the 4 July is fast approaching and polling strongly suggests that the Labour party is expected to win a significant majority. Although political events rarely alter the course of the global economy and markets, would a Labour government provide investors with enough perception of “change” to encourage them to give unloved UK equities another look? We look at market reaction to previous UK elections and the outlook for key sectors if stability is delivered by a new government.

How much volatility can we really expect?

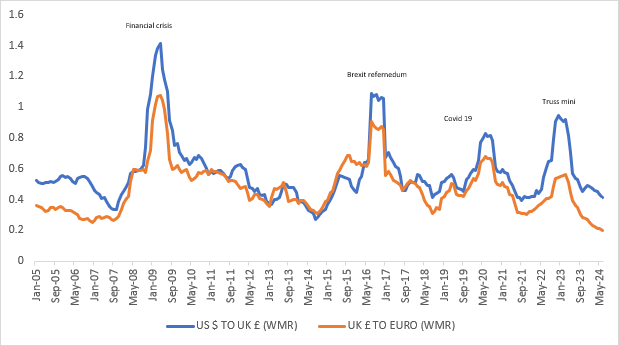

History shows us that elections and referenda can be market moving events in the short term. During the Brexit referendum GBP volatility soared to levels not experienced since the financial crisis of ’08 however, in our experience, short term volatility tends to normalise over the medium to long term. The “noise” around a vote is often an opportunity to take advantage of short term price dislocations, providing an attractive entry point for long-term investors.

GBP 6m rolling volatility – daily returns.

In a year where more people globally will vote than in any year in history, political uncertainty is likely to dominate market headlines and unnerve investors. However political events rarely alter the course of the global economy and/or markets.

Political events and market reactions:

| S&P 500 | Nikkei | MSCI World x USA | DXY Dollar Index | ||||||||||

| Date | Initial reaction | 30 days | 90 days | Initial reaction | 30 days | 90 days | Initial reaction | 30 days | 90 days | Initial reaction | 30 days | 90 days | |

| Nixon/Watergate | 15/03/1974 | -1.7 | -7.3 | -8 | -1.8 | 1.1 | 4.4 | 0 | -2.6 | -6.1 | -1 | -1.6 | -2 |

| Clinton intern scandal | 20/08/1998 | -12.3 | -6.2 | 5.6 | -8.3 | -11.7 | -6.7 | -12.7 | -12.7 | -6.4 | -1.8 | -5.2 | -6.6 |

| Brexit | 23/06/2016 | -2.3 | 4.3 | 3.7 | -6.8 | 3.5 | 4.6 | -5.3 | -0.4 | 1.7 | 1.9 | 4 | 2.5 |

Economic variables such as interest rates, employment figures and GDP tend to be more discernible factors in driving the market. Over time, politics has the ability to shape a country’s political and cultural direction, which can feed through to the economy and business and therefore impact markets. For this UK election the more fiscally conservative nature of the Labour government under Keir Starmer and the desire of the Labour party to demonstrate stability means that it is unlikely that this election result will fundamentally alter the direction of the UK equity market. But there is a chance that the perception of “change” could encourage investors who have maybe taken a break from the UK market to revisit it – particularly given the valuations available relative to the rest of the world.

What will a Labour government mean for the economy?

Shadow Chancellor Rachel Reeves has proposed little change to current economic policy and both parties have recognised the need for economic growth after a long period of stagnation. Labour’s points of differentiation centre around VAT on private school tuition and changing tax rates for ‘carried interest’ to fall under the higher bracket of income rather than capital gains tax. While hedge funds and private equity firms may be displeased, these policies are unlikely to have a significant immediate impact on the economy.

Though Labour’s policies under former leader Jeremy Corbyn were characterised as ‘anti business’, looking back through time, we see little distinction between the effects of a Conservative or Labour led government on the listed market. The incoming government is likely to be constrained by the wider economic environment, poor growth and the need to raise revenue, which will drive tight fiscal policy. On top of this Rachel Reeves and Keir Starmer have, during the campaign so far, put themselves into a tighter spot by ruling out potential tax rises.

After a period of extended volatility, investors will be looking for a government that can deliver stability and recognise the benefits that private capital can bring to the investment needed in the country – as long as that capital can earn a reasonable return. Stability – if delivered – could bring benefits to the UK listed market, and this will particularly be the case if there is upheaval, turmoil or simply uncertainty in Europe and the US.

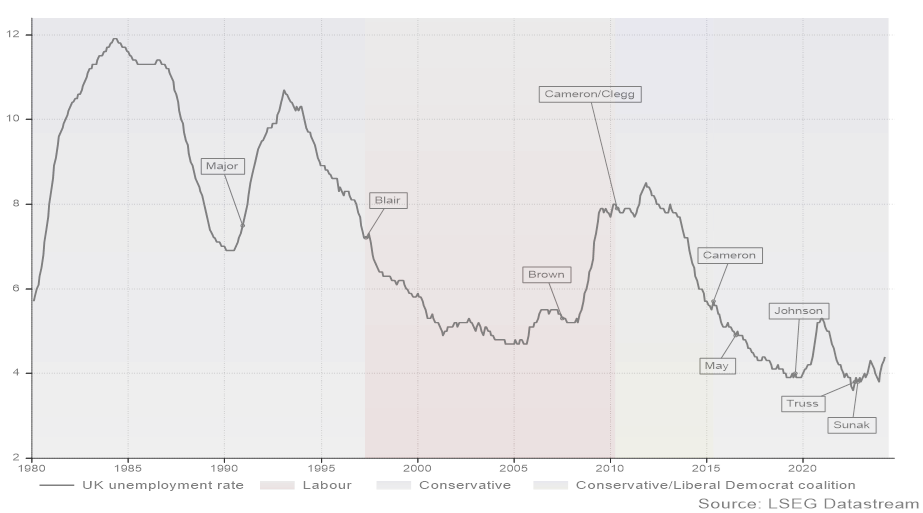

UK unemployment rate through different political parties:

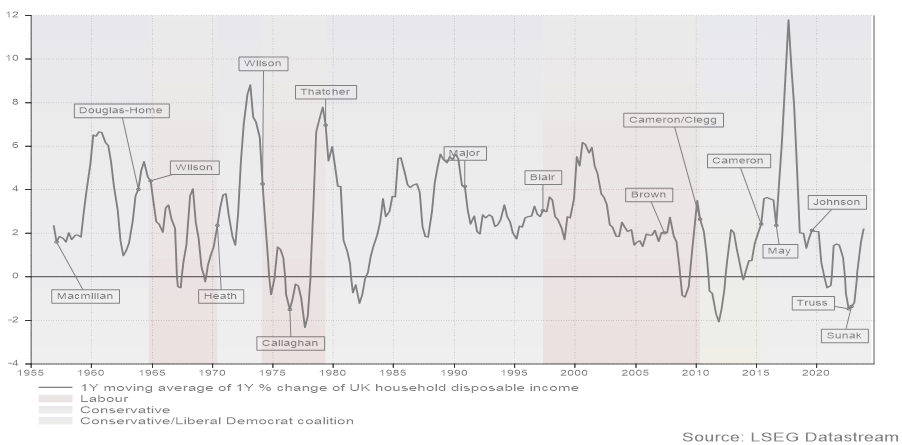

Strength of the UK personal balance sheet:

The current fiscal outlook is unlikely to change substantially whether the Conservatives or Labour party are in power. However, we see a Labour victory as bringing some positives for the UK market. Labour has expressed its intention to drive deeper relations with the EU, providing a boost to both GDP and supply. The prospect of closer ties could help to unwind some of the Brexit discount and could be of particular interest to global investors.

What can we expect with a Labour government?

Though UK equities may be treading water into the election day, we reiterate the potential of a more stable government for UK plc. Since 2016 there have been 13 housing ministers, nine education secretaries and eight home secretaries6. However, where do we see market opportunities with a Labour government majority?

Housebuilders

The Labour party has consistently committed to reforming the current planning system, a headwind that has heavily constrained long-term volume delivery and growth for UK housebuilding. Had the UK had kept pace with the rest of Europe since the 1950s, it would have an additional 4.3 million homes today. Introducing a more standardised approach to infrastructure build and use of ‘grey belt’ land could provide significant upside for housebuilders in the medium term. As an offset it is always possible that an incoming government seeks to offset some of the positive impact through an additional charge or tax on the sector – but the positive benefits for the corporates involved could well outweigh this.

Energy

Labour is likely to continue to be pro-renewable energy, and has proposed a clean energy system by 2030 and an increase in taxation of North Sea oil and gas profits. A windfall tax on oil and gas is unlikely to impact the sector heavily since the burden falls specifically on North Sea production (a tiny proportion of most listed players’ business) and the prospect of accelerated decarbonisation offers ample opportunity through required growth in networks and renewable power.

Pensions

Pension fund investment in UK equities has been in decline for some time, as they took part in a structural de-risking away from UK equities. The current government introduced the Mansion House reforms to address this, and Labour has proposed a near identical proposal. The current proposals are likely to be around introducing disclosure requirements around investment in UK equities rather than mandatory allocation to UK assets. While these reforms are unlikely to be immediately significant, at the margin we feel this is a positive for the UK equity market.

Auto-enrolment

The incoming government is likely to carefully consider whether the UK population is saving enough for retirement (spoiler: we are not) and may well look at increasing auto-enrolment contributions as a proportion of salary. This could be a positive for participants in the financial sector.

Tax

Labour’s current tax pledges could come under pressure over time, dependent on economic growth. Ambitious goals to be the fastest growing country in the G7 will need spending support from government and the private sector. A potential roll back on tax pledges in key areas such as capital gains may be a real possibility. It is also possible that the Treasury under Rachel Reeves leadership seeks to raise taxes in areas hitherto undisclosed and undiscussed. We should not rule out the potential for more targeted corporate taxes and there remains the possibility that areas of the market like the banking sector which are already subject to specific taxes see these increased. Finally, the personal balance sheets of consumers are in reasonable shape currently but the potential for higher interest payments on mortgages and the potential for higher personal taxation means consumer spend is likely to remain somewhat constrained, albeit perhaps not as constrained as some of the more bearish commentators might suggest.