As stagflationary pressures reshape the investment landscape in 2026, traditional portfolio diversification assumptions are being tested to their limits. In this environment, Dan Kemp, Founder, Portfolio Thinking, explains how and why fixed income is no longer a simple hedge but a critical source of portfolio resilience, providing the structural “ballast” needed to stabilise outcomes through volatility, even when bonds and equities fall in tandem.

The financial landscape of 2026 is providing a formidable stress test for independent financial advisers and their clients. Geopolitical turmoil, sluggish economic growth, fractured supply chains, and stubbornly sticky inflation have resurrected the spectre of stagflation. In turbulent market conditions, the natural human reflex is to seek immediate shelter, demanding swift portfolio adjustments to shield capital from unpleasant headlines.

However, successful stewardship requires a more nuanced understanding of how portfolios actually behave under extreme stress. When inflation expectations become unanchored and growth stalls, bonds and equities can fall simultaneously. This recent phenomenon traumatised many investors, negating the traditional benefits of holding fixed income as an automatic counterweight to equity exposure.

To navigate the current environment successfully, we must discard outdated mental models. Rather than regarding equities and bonds as two ends of a simple seesaw, consider bonds as akin to the ballast in a ship.

When a vessel encounters a severe storm, no amount of structural engineering can prevent it from pitching violently or dropping into the trough of a massive wave. The role of the ballast in these situations is not to keep the ship perfectly still, but to provide the critical weight and low centre of gravity required to right the ship after a severe roll. Without sufficient ballast, the ship is unstable and risks capsizing.

Within a multi-asset portfolio, fixed income serves the same purpose. It does not guarantee a smooth ride, but it provides the fundamental righting lever that prevents a temporary decline from becoming a permanent loss of capital.

The mathematics of the ballast: the pull to par

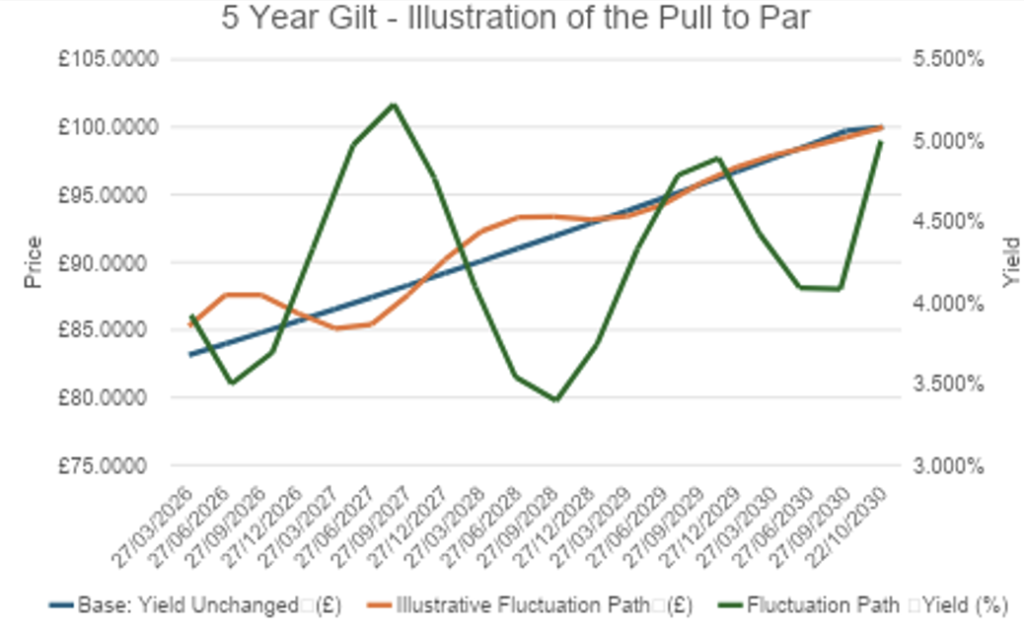

To truly understand why high-quality government bonds serve this function so effectively, we must unpack the unique mathematics of the asset class. The defining characteristic of a sovereign bond is the certainty of its return structure.

When you purchase a high-quality government bond and hold it to maturity, the return of your principal is guaranteed (barring an extreme, tail-risk default scenario). However, this guarantee does not mean the price remains constant along the journey.

In the midst of a stagflationary storm, the market price of that bond will inevitably fluctuate, sometimes falling significantly as inflation fears dominate the narrative. But unlike an equity, a bond possesses a gravitational “pull to par” – as shown in Fig 1. Any temporary decline in price is compensated for by an increase in future yield. The total nominal returns are contractually fixed; they do not evaporate simply because the market is panicking. The volatility represents a change in the timing of your returns, not a permanent destruction of your capital.

Source Portfolio Thinking

Naturally, the real purchasing power of these returns is eroded by actual inflation, but crucially, it is not destroyed by the mere fear of inflation that drives daily price changes.

However, bond mathematics is not a panacea. If purchased at unattractive yields, the guaranteed nature of bonds simply locks in low returns. This is precisely why a valuation-driven approach is just as vital for fixed income as it is for equities. Today, with government bond yields sitting closer to the top of their historical range, the mathematics of bond investing are far more forgiving than they were half a decade ago. Furthermore, for UK investors holding gilts directly, structural tax advantages can enhance net returns.

Knowing what you own: sovereign versus corporate debt

However, to build a robust proposition, we must be exceptionally clear about what type of ballast we are loading. Treating all fixed income as a homogenous block is a dangerous oversimplification.

While high-quality government debt remains the purest form of portfolio stability, corporate credit plays a profoundly different role. Currently, credit spreads, the additional yield investors demand for accepting the risk of default, remain unusually compressed in many areas of the market, seemingly ignoring the potential consequences of a stagflationary environment.

Historically, tight spreads offer an inadequate margin of safety when the broader economic environment deteriorates. Consequently, lending to corporations at current valuations requires an optimistic view of the economy’s path forward. Reaching for a fractionally higher yield by taking on uncompensated credit risk creates the illusion of value but structurally compromises the vessel right when the storm hits.

The imperative for active navigation

Most investors do not hold bonds directly but access these markets through funds. This raises the perennial debate of active versus passive implementation. In equity markets, this debate often centres on the efficient processing of information. In fixed income, the underlying architecture demands a different perspective.

To return to our maritime analogy, relying on a purely passive bond index in a stagflationary environment is akin to locking the ship’s rudder and sailing blindly into the storm, simply because that is the route the heaviest ships are taking. By design, market-cap-weighted bond indices allocate the greatest amount of capital to the entities that have issued the most debt. While this approach offers broad exposure and low costs, automatically lending more money to the most heavily indebted borrowers in a world of rising costs and geopolitical fracturing requires careful scrutiny.

In contrast, an active manager acts as the vessel’s navigator. They possess the flexibility to adjust the ballast and alter course as the weather changes, stepping away from vulnerable corporate issuers and identifying mispriced opportunities across the sovereign yield curve. Naturally, this requires considerable skill to overcome the higher fee drag of active management. However, in an environment fraught with macroeconomic uncertainty, the ability to actively sidestep uncompensated risk is not a luxury; it is a vital component of capital preservation.

Client behaviour: the real challenge of 2026

For the independent financial adviser, the defining challenge of 2026 will not be predicting the precise trajectory of inflation, guessing central bank policy, or timing the resolution of global conflicts. The greatest challenge will be managing client behaviour through the noise.

When the news cycle is dominated by pessimistic narratives, clients will inevitably feel an overwhelming urge to alter their portfolios. Our role is to remind them that volatility is simply the psychological tax we pay for long-term compounding. By anchoring our fixed income allocations in deep valuation and the mathematical certainty of the asset class, we provide the heavy ballast our clients need to navigate the trough and remain securely on the path to their ultimate destination.

This feature was part of our 2026 Fixed Income Insights. For deeper analysis on bond markets and rates strategy for advisers, explore IFA Magazine’s latest Fixed Income Insights publication.

About Dan Kemp

Dan is an investment leader with over twenty-five years of experience. As the Chief Research & Investment Officer at Morningstar, he has overseen approximately $350 billion in assets, leading global teams across Equity Research, Manager Research, Portfolio Management and Behavioural Science.

A theologian by training and an investor by trade, Dan combines analytical rigour with a deep understanding of human nature. Throughout his career, from advising individuals on their savings and trustees on aligning strategy with values to managing complex retirement solutions, his mission has remained consistent: to help investors reach their goals through transparency, stewardship, and evidence-based decision making.