The average closed easy access account rate has been lower than the live equivalent over the past two years. Moneyfactscompare.co.uk analysis reveals how savers are being short-changed as Consumer Duty rules on closed products and services come into play this month.

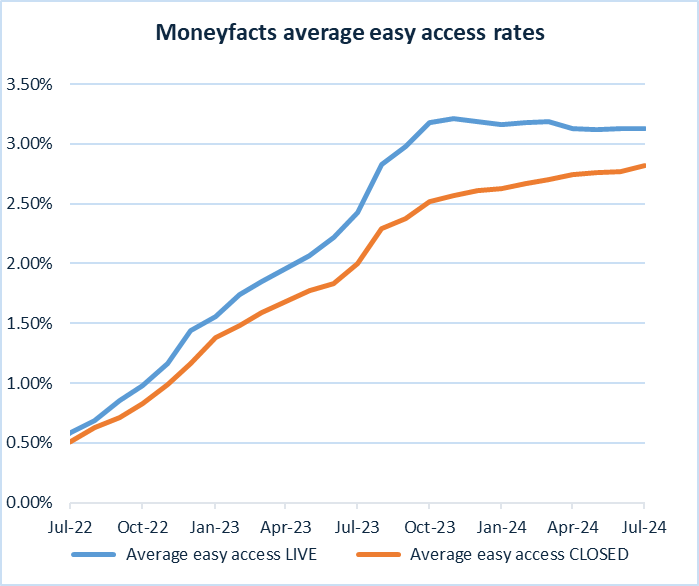

- Over the past two years, the incentive to switch from a closed savings account to a live deal has grown substantially. The difference between the average closed rate and live rate on easy access accounts has widened from 0.08% in July 2022 to 0.31% in July 2024.

- The biggest rate margin between the average easy access closed rate and live rate, where the latter is higher, was in October 2023 at 0.66% (2.52% versus 3.18%). In July 2023, the margin was 0.43%, which is a difference of 0.12% compared to July 2024 (0.31%).

- The biggest banks are paying less than 2% on their most flexible live savings accounts, which is lower than both the average overall live and closed easy access account rates of 3.13% and 2.82% respectively. Out of the biggest brands: Barclays Bank (1.65%), HSBC (1.98%), Lloyds Bank (1.40%), NatWest (1.74%) and Santander (1.70%).

- The Financial Conduct Authority (FCA) Consumer Duty rules for open products and services came into effect in July 2023, the duty for closed products and services comes into effect on 31 July 2024. This includes easy access savings accounts which are no longer on sale to new customers.

| Savings market analysis – easy access accounts | |||||

| Jul-22 | Jan-23 | Jul-23 | Jan-24 | Jul-24 | |

| Average easy access – Live | 0.59% | 1.56% | 2.43% | 3.16% | 3.13% |

| Average easy access – Closed | 0.51% | 1.38% | 2.00% | 2.63% | 2.82% |

| % Difference | -0.08% | -0.18% | -0.43% | -0.53% | -0.31% |

| Interest loss on £10,000 after 12 months | £8 | £18 | £43 | £53 | £31 |

| Average AER based on a £10,000 deposit as at the start of the month. Source: Moneyfactscompare.co.uk. | |||||

| Big bank easy access selection* | ||

| Provider | Account | Gross rate at £10k |

| Barclays Bank | Everyday Saver | 1.65% |

| HSBC | Flexible Saver | 1.98% |

| Lloyds Bank | Easy Saver | 1.40%** |

| NatWest | Flexible Saver | 1.74% |

| Santander | Easy Access Saver | 1.70%*** |

| *Deals available to new customers and includes accounts that allow multiple withdrawals without penalty. **Reverts into Standard Saver after 12 months, which currently pays 1.40%. ***Reverts into Everyday Saver after 12 months, which currently pays 1.20%. Based on a £10,000 deposit, gross rates. Data correct as of 10.7.24. Source: Moneyfactscompare.co.uk | ||

Rachel Springall, Finance Expert at Moneyfactscompare.co.uk, said:

“Savers are being short-changed if they don’t proactively review and switch from their closed easy access accounts. Over the past two years, the average rate on a live easy access account has surpassed the average closed rate, despite base rate rises from the Bank of England and numerous calls for the biggest banks to improve savings rates for existing customers. Savers must shake any apathy they have to move their pots, otherwise they will be left disappointed when their loyalty is not rewarded.

“As some of the biggest high street banks pay less than 2% on their most flexible live easy access accounts, some of the top rates on the market overall pay around 5%. Despite using a trusted brand, the convenience of leaving cash in an easy access account can mean missing out on higher interest rates elsewhere, so it is imperative savers ditch and switch to a better return. Building societies and challenger banks continue to work hard to entice new deposits and reward loyal customers so they are worth comparing against the more familiar high street brands

“In the months ahead, it will be interesting to see if any savings providers pull closed savings accounts or move customers onto different products as Consumer Duty rules on closed products come into force. According to the Financial Conduct Authority (FCA), firms’ closed products and services “will need to be compliant with its expectations under the Consumer Duty price and value outcome” from 31 July 2024. This includes “an easy access savings account which is no longer on sale to new customers”. As it stands, consumers may well have mixed thoughts on how this will impact them, but a recent survey conducted by Moneyhub revealed 36% of respondents felt Consumer Duty “will drive banks to become more customer-centric institutions”.

“As the FCA’s Consumer Duty deadline for closed products nears, it is worth noting that not every institution has a closed savings account, but if they do, customers need to see if they are getting a raw deal. The average rate for an easy access account that is closed to new business is 2.82%, compared to the live easy access rate which is 3.13%, so those with a balance of £10,000 could earn an additional £31 in interest over 12 months simply by switching, based on average rates, but they could be earning £500 a year if they have an account that pays 5%.”