With so many converging themes due to affect financial services in 2024 and Christmas and the end of 2023 approaching fast, it felt apt to give a list of our predictions for 2024. Why not, everyone is doing it!

As we say farewell to 2023 and welcome in 2024 it’s natural to reflect on what has been and muse over what may be coming down the road. Here are our best guesses for the year ahead.

1. The UK Economy

Laith Khalaf, head of investment analysis at AJ Bell shared: “Economic growth is forecast to be thin on the ground going forward, with growth of just 0.7% next year, rising to 1.4% the year after. The budget watchdog is actually pretty upbeat compared to the Bank of England, which sees growth coming in at 0.1% next year and 0.2% the year after. It remains to be seen which set of predictions prove to be correct, if either.”

Economies in the West did better than expected in 2023, but even if we manage to avoid a recession here in the UK, times are likely to remain tough for many consumers and businesses throughout 2024.

Avoiding a recession is going to be a tough ask but not impossible. Usually when an economic cycle starts with high inflation, the likelihood of a ‘soft landing’ diminishes, but stranger things have happened.

But according to data from FT, UK voters out there already think we are in a recession!

Roger Martin-Fagg, a behavioural economist thinks that “the UK faces five unique circumstances, Brexit, five prime ministers in seven years, a permanent shortage of labour, chronic underinvestment and a diminished brand value.”

Based on this it looks like the UK is going to be kept fairly busy throughout 2024.

2. Interest rates will reduce, but also maybe won’t.

After fourteen consecutive rises, the UK Bank rate in September, set by the Monetary Policy Committee, was unchanged from the previous review at 5.25%. The Bank rate is currently still at its highest level for fifteen years and the pause was the result of five votes against four within the committee, so a close call.

Andrew Bailey, Governor of the Bank of England, said at the time: “I can tell you that we have not had any discussion… about reducing rates because that would be very, very premature. Our job is to get inflation down.”

So, what does that mean for 2024?

Well firstly, interest rates are not high, they are about average if you’re looking over the past fifty years. They just feel high because we have only experienced very low rates over the past ten years, as the global economy struggled to recover from the GFC of 2008.

Interest rates are set at the level they are to reduce inflation towards the Bank of England’s target of 2%. The idea is that if interest rates are high, mortgage and borrowing rates will increase and people will spend less, thus there is less demand and inflation falls. It also affects the relative value of sterling on currency markets and thereby the value of imports v exports and global currency flows.

However, there is a slight issue with that logic. A larger proportion of consumers don’t have mortgages than do have them. We have an ageing population, and when people retire, they have usually managed to pay off their mortgage. So more than half of the population isn’t hugely affected directly by interest rate rises.

This means retirees need to make sure they’re shopping around for their deposit accounts to get the best rate, especially amid recent accusations that banks have not been fully passing on the higher interest rates to their savers.

In short, interest rates are unlikely to be hiked again in 2024 and more likely to reduce, albeit slowly.

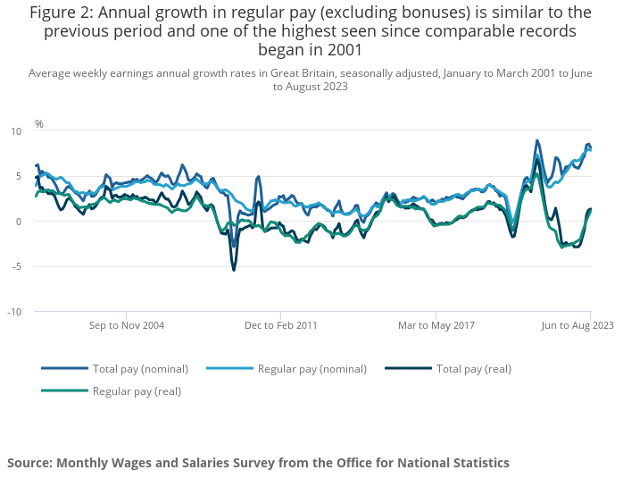

3. Inflation. It’s not personal.

Inflation has remained stubbornly high in 2023 and that can be attributed largely to supply restrictions which came about because of Covid and Brexit and the soaring cost of energy. This is the reason our inflation remains higher than many of our European neighbours. At the time of writing, UK inflation stands at 4.6% year on year to October 2023.

In times of high inflation, it’s good to remember that the public rate of inflation is not an individual’s rate of inflation. The published inflation rate is based on the CPIH basket and within the basket is a collection of goods thought to be relevant to the world we live in. But the items in the basket, totalling around 743, will never match your personal consumer habits. For example, in 2023 unless you bought an e-bike, a security camera and a soundbar your rate will be different to that in the news.

Also, whilst it may feel like finances are getting a bit of a squeeze, disposable income has actually increased, with pensioners potentially ending up being the best off after the significant state pension increases of 10.1% in 2023 and 8.5% in 2024.

Inflation is expected to reduce further, but it will be slow, and we are likely to be above the Bank of England’s target base rate for a few years yet. While the inflation rate may be falling, prices are still rising of course, impacting the real value of money and clients’ assets.

4. Politics Trump it all

It feels like déjà vu, but sadly it’s not. Donald Trump apparently has a considerable chance of regaining the US Presidency in 2024. Having been underestimated in his bid to be re-elected, it appears he’s managed to somehow sneak back into favour in the US, despite being involved in four ongoing criminal trials for 91 felonies. If this were to happen, the consequences would be global, affecting everything from climate policy to military support for Ukraine.

Regarding the upcoming UK election, it’s probably too early to tell what the race will bring or make any predictions. Bloomberg announced in September that: “A Labour-led government after the next UK election would be the best result for stocks and the pound according to a new Bloomberg survey that shows the ruling Conservatives have failed to win back the faith of global investors.”

I am sure 2024 will be saturated with election speculation from the UK and across the pond, so that’s enough on this matter… just for the time being.

5. Markets. Don’t give up on the UK.

As we go to print, the FTSE 100 index stands at under 7500. It is at almost exactly the same level as of January 2018. This means that there has been no capital growth in the index for over 5 years! So, what’s going on? And more importantly, when will it change?

Hindsight is easy, and we know that the pandemic, uncertain political leadership, slow growth, abnormally high inflation and Brexit are the main causes of the FTSE’s poor relative results.

So when will it change?

It really depends on a few factors – including economic growth, inflation and politics.

When inflation is high, companies have higher costs and cannot always pass that on to customers, so margins are squeezed, and the share price goes down. When you have political uncertainty, investment in the UK falls because people fear what will happen. As they pull money out of the UK markets or no new investments get put into the UK, the reduced demand and increased supply drive down the stock market.

James Sullivan, Chief Investment Officer at Trust DFM states: “There remain, as always, a host of concerns for markets to navigate in 2024, including the lagged effect of significant interest rate increases still to work through the system, generally weak economic activity levels, heightened geopolitical tensions in multiple regions and a less than stellar start to the corporate earnings season.”

Despite these challenges, people should be wary about being tempted to move into cash during periods of high inflation and disappointing market performance, despite fixed interest still being very appealing.

With nominal interest rates high and the markets remaining volatile, it may be tempting to keep more money on deposit rather than invest it. However, long term, cash is not always king. In fact, it rarely is, as even though interest rates are high, inflation is nearly always higher!

To demonstrate this, here is a chart that shows the results of moving into cash at the time of certain market events between 1992 and 2022.

And that’s a wrap.

Whilst we can all guess or predict, nobody actually knows what is going to happen in 2024. But it can be interesting to take educated guesses and see if they come to fruition. Like we always say in the world of finance, past performance is never a guide to the future. Yes, that’s true of course, but it can sometimes give you a pretty good idea. Time to put the crystal ball away for now and enjoy a well-deserved break so we are fighting fit to begin the New Year in robust form.