Once the preserve of large institutions, investments in early-stage unlisted businesses are now becoming an important part of some client portfolios. The growing interest reflects a broader change in sentiment towards democratising access to private markets, making them more accessible and inclusive to a wider range of investors.

Investors are hungry for higher returns, greater diversification beyond portfolios weighted toward listed equity and bonds, and opportunities to back exciting companies with significant growth potential. You only need to look at the growth in crowdfunding platforms to see evidence of this.

At the same time, pension funds are under increasing pressure to direct more capital towards private markets and the UK economy – as set out in the Mansion House Accord from May 2025.

Why early-stage businesses can outperform incumbents

While investors in early-stage businesses face greater risk due to higher failure rates compared to more mature businesses, they also benefit from substantial upside potential. By investing in venture capital, clients gain exposure to these businesses which, given their stage in the growth cycle, have the potential to generate outsized returns relative to more traditional asset classes.

Macroeconomic factors, can be a significant driver of growth and success for early-stage companies. Surprisingly, even uncertain economic environments can create opportunities for early-stage companies. Their agility allows them to pivot quickly, responding to changing market demands, and capitalise on gaps left by bigger and slower competitors. This flexibility can be a key advantage in volatile environments.

Most recently, inflation and tighter capital markets have pushed many tech firms to cut costs and prioritise profitability.

What to expect from an early-stage portfolio

Investors looking to access venture capital often buy shares directly in early-stage companies. With this approach, returns are typically only realised when these companies are either sold to another company or list on a stock exchange. Naturally this takes time, and investors are usually unable to access their investment prior to realisation. Investors must therefore generally commit to a five to ten-year investment horizon and be comfortable with having limited or no access to their funds during that period.

By their nature, early-stage companies also have a high rate of failure so it is important that investors are appropriately diversified in their exposure to companies and that they understand how their investment values may fluctuate.

Allocation based on risk appetite

Clients with the appropriate objectives and risk profile may be comfortable taking on more risk with a portion of their assets. Adding investments in early-stage businesses to an existing portfolio allows a client to target higher returns, but also adds risk to the portfolio.

However, those that are new to venture capital often think investing in early-stage companies only means taking big risks. This view overlooks how venture capital can help diversify within a balanced portfolio. When considering a client’s exposure to early-stage businesses, it’s important to take a holistic view of a client’s portfolio. We need to recognise that a portfolio can be made up of assets that have different risk profiles and different degrees of correlation, while the overall level of risk in the portfolio is at an appropriate level for the client.

Adding venture capital to a portfolio without increasing overall risk

Dr Moretta, Head of Tax Enhanced Services at Hardman & Co, researched the effect of adding venture capital to client portfolios. Using market data and established research for venture capital, he applied Modern Portfolio Theory to determine optimal asset allocations. Modern Portfolio Theory looks at risk through the lens of variance (the volatility of returns for each asset class) and uses this to establish the optimum allocation, producing the potential best return for a given level of risk across a portfolio.

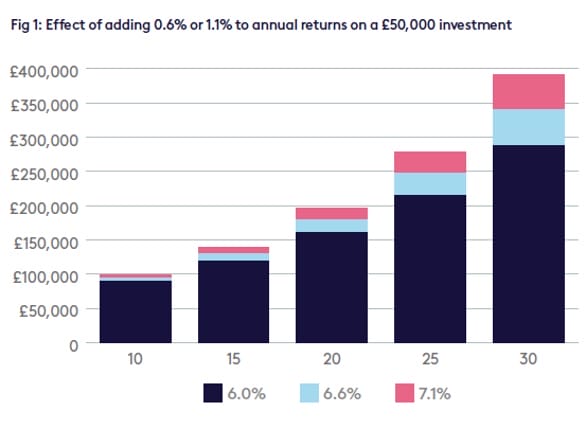

Effect of adding 0.6% or 1.1% to annual returns on a £50,000 investment

Dr Moretta’s research found that by adding relatively small exposures to venture capital, investors can improve potential annual returns by 0.6% to 1.1%** without changing overall portfolio risk. While this might not sound like much, the impact of compound returns is significant. The chart in Fig 1, taken from the research shows the effect of adding 0.6% to 1.1% to a £50,000 investment returning 6% annually over 30 years.

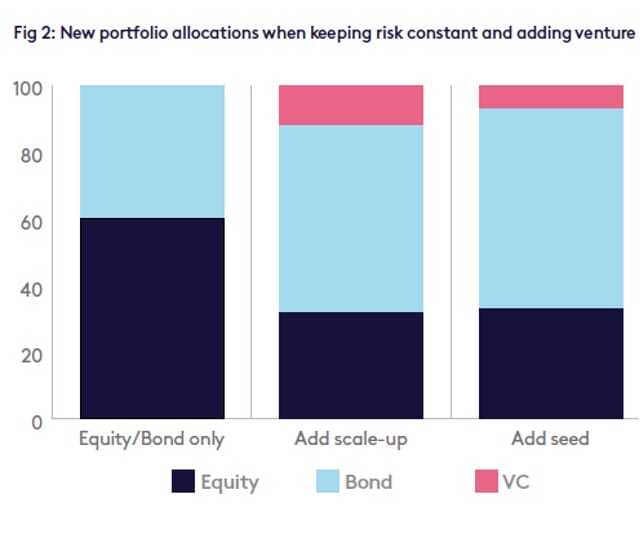

Rebalancing a 60:40 portfolio when adding venture capital

When a portfolio’s asset allocation changes the overall exposure to risk will often change too, however, careful rebalancing means that this can be avoided. The chart in Fig 2 taken from Hardman & Co’s latest research shows how asset allocation might change from a 60:40 equity and bond portfolio when venture capital is introduced, where a client wishes to keep the same level of overall portfolio risk.

Allocations are shown for the addition of seed capital (where companies are in product development and finding their first customers) and scale-up capital (investing in slightly later stage companies with an established product and market).

Dr Moretta explains: “We are adding a riskier asset to the portfolio. It’s not simply a matter of leaving the rest of the portfolio unadjusted or even selling down equities to invest in venture capital. We have to reduce equities by even more and increase the bond proportion to keep the same overall risk.”

Applying this in practice

While the theory behind portfolio rebalancing makes sense, it’s not typically well understood in practice. This creates an opportunity for advisers to add real value by helping clients manage asset allocation more effectively.

Since Dr. Moretta’s research was first published in 2021, interest rates and bond yields have risen significantly. Encouragingly, the recommended allocations remain very similar, showing that the model is robust. The upside for investors is that the rebalancing now feels more attractive – earning 4%-5% on bonds is far more appealing than the 2% yields available previously. As a result, expected overall returns have improved.

This analysis doesn’t account for tax reliefs, which can further enhance returns. Conversely, venture capital funds typically have higher fees than traditional equity or bond funds. However, with long enough holding periods, the tax benefits can outweigh the higher costs – making this a more attractive option for suitable investors.

It’s worth noting that short-term volatility often appears lower than for quoted equities. Venture capital assets may not react to external market shocks in the same way as quoted equities. For instance, during the early months of the COVID-19 pandemic, when listed markets saw sharp swings, unquoted valuations stayed relatively stable. While this can help with short-term portfolio stability, it may cause an imbalance after sharp market movements and investors can end up overexposed to private assets without an easy way to rebalance, due to their illiquid nature.

How clients can access venture capital

With the inclusion of venture capital in a diversified portfolio, you can potentially raise expected returns while being mindful of an investor’s overall risk appetite.

Direct access to early-stage companies for clients outside of family office levels of wealth can be difficult. However, the Enterprise Investment Scheme (EIS) and Venture Capital Trusts (VCTs) are an attractive and accessible route to diversifying client portfolios with investments in smaller companies. These investment structures make it possible for clients to invest in private companies and claim tax reliefs to compensate for some of the risk they take.

It’s worth reiterating that the potential impact of tax reliefs is excluded from the analysis in this article, making these types of investments even more compelling within a long-term investment portfolio.

Written by Toyin Oyeneyin, Tax Product Specialist at Octopus Investments.