This is the 2nd part of the detailed analysis from Defaqto which was featured in our Multi-Asset Fund Insights publication, sponsored by Schroders and produced in partnership with Defaqto. In their analysis, Defaqto’s Fraser Donaldson, Investment Consultant and Mike Turner, Investment Development Consultant, explore how multi-asset investing has evolved and where it’s heading next. In part one, which we published earlier this month, Fraser and Mike looked at the rise of multi-asset and the diversification benefits it brings. Here, in part two, they look at different types of multi-asset solutions, the evolution of the multi-asset market and what the future may hold for this important investment approach.

Advisers can download IFA Magazine’s full Multi-Asset Fund Insights publication for deeper analysis and exclusive insights from leading fund managers on navigating today’s multi-asset fund landscape.

Why multi-asset vehicles?

Multi-asset investment vehicles not only help to achieve diversification, but they also make rebalancing easy, as the manager can rebalance the portfolio back to its strategic longer term asset allocation either on a set frequency or as and when necessary. While the asset manager is essentially doing what an adviser would be doing for advisory clients, undertaking this in a multi-asset vehicle has a number of advantages.

Whether through a fund or managed portfolio, the asset manager is making each trade on behalf of a large number of underlying investors. The buying power of the manager is infinitely greater than an individual investor, allowing economies of scale to be achieved which should reduce the overall costs of the investment portfolio. Furthermore, asset managers have access to resources, data flows and expertise that the average DIY investor or adviser dealing with individual clients on an advisory basis does not have.

The different types of multi-asset solutions

Multi-asset solutions come in several structures, each offering different ways to access diversification. One common approach is direct holding multi-asset funds, where the fund manager invests directly into securities, covering a range of assets. Traditionally there’s a lower total cost associated compared to some of the other types of multi-asset solutions, as there are no underlying fund layers.

Another approach is the Fund of Funds (FoF) structure, where the portfolio invests in a selection of other funds rather than directly in securities, therefore diversifying manager risk. Within this category, there are two key types: fettered and unfettered funds. A fettered fund of funds traditionally invests only in funds managed by the same asset manager, which can offer greater control and some cost benefits, but may limit choice and sometimes diversification. However, over the last decade we have seen many fettered FoFs allocating a minority of the portfolio to external funds or even direct securities where internal options are limited, with the goal of offering better outcomes for the end investor.

An unfettered fund of funds selects funds from across the whole market, allowing access to best-in-class funds regardless of provider, but potentially adding additional layers of cost. In recent year, managers have been reducing the additional cost through investing in underlying passive investments such as trackers and ETFs.

Manager of Managers (MoM) portfolios, which utilise a segregated mandate approach, have a central manager which appoints specialist managers to run different parts of the portfolio according to their defined mandates. This allows for highly tailored investment strategies, tight risk controls, and access to specialist expertise. Typically, there are few of these in the market compared to the fund of fund market as the manager of manager has to have the buying power to secure the services of top managers.

Lastly, Model Portfolio Services (MPS) have grown in popularity, particularly in the advised market. MPS solutions offer clients access to risk-rated, professionally managed portfolios without the need for a fund wrapper. Instead, the portfolio is built from underlying funds and in a minority of cases direct investments. The portfolios sit on a platform under the client’s name or in a direct custodian account with the DFM. MPS solutions appear as a portfolio of individual lines of investment to advisers and their clients, which has some appeal.

The evolution of the multi-asset market

The evolution of the UK’s multi-asset (MA) landscape has been striking over the past few decades. Initially dominated by multi-asset funds such as unit trusts and OEICs, the market has expanded dramatically with the advent of Model Portfolio Services (MPS).

As shown in Chart 1, MA fund solutions in the 1990s were relatively limited, growing modestly into the 2000s. However, the true inflection point came in the 2010s, where platform-distributed MPS solutions began to overtake MA funds in terms of choice, driven by Retail Distribution Review (RDR) of 2012 and evolving adviser needs. By the 2020s, MPS offerings represent a substantial share of the total MA solutions market.

As well as breadth of choice, there is also depth, with significant numbers of different styles available (ESG, Passive, Active, Income oriented etc).

This regulatory environment proved fertile ground for the rapid adoption of risk-rated MA funds and later the widespread take-up of platform-based MPS solutions.

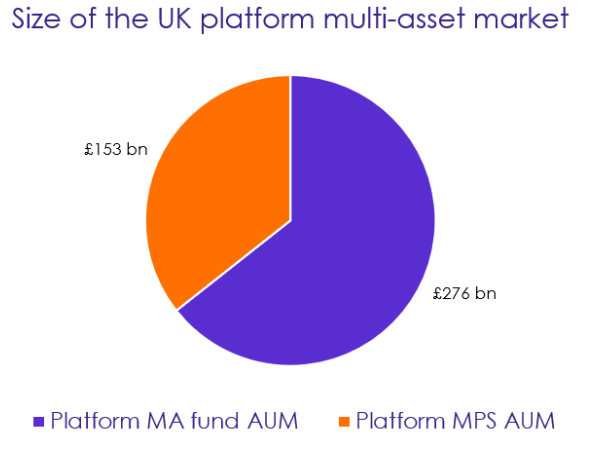

The size of the UK platform retail multi-asset funds and DFM MPS market combined was estimated at circa £400bn at the end of 2024. Chart 2 illustrates that platform MA funds account for 65% of the UK platform multi-asset market with £276 billion AUM, compared to £153 billion AUM for platform MPS portfolios. Quite a surge in MPS investing given they started from almost nothing 15 years ago.

Chart 2 shows size of the UK platform multi-asset market compared to MPS

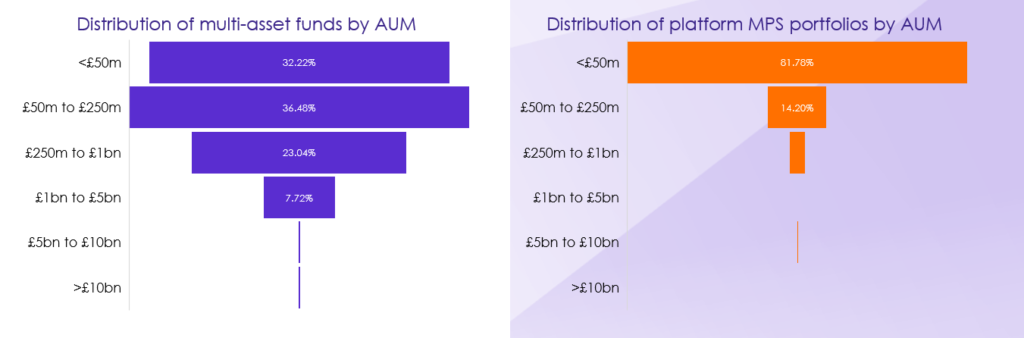

When we focus in further to how the multi-asset market is segmented (see chart 3) we can see the MA fund market is fairly even indicating a mature and established market where over time asset management firms have successfully scaled their strategies with 30% of the MA fund market operating with AUMs of over £250m.

This is maybe unsurprising as many advisers and clients trust the structure, regulation, and oversight associated with OEIC and unit trust vehicles. For many, MPS investing is a relatively new concept introduced to the market through the outsourcing theme introduced by the RDR.

In stark contrast the MPS market is heavily skewed towards small scale solutions with 82% of the market operating with portfolio AUMs of less than £50m. This does mean that advisers have to consider if some DFMs will have longevity.

Chart 3 How is the market segmented?

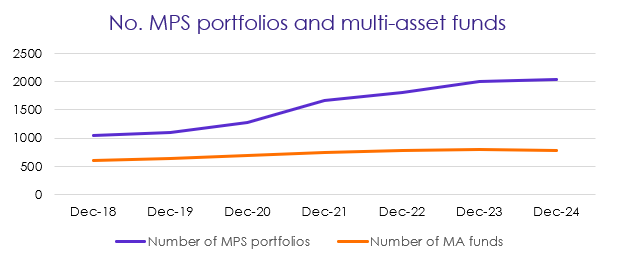

However, the skew towards smaller solutions in the MPS space when compared to the MA fund space is indicative of a less mature market that’s seen recent rapid growth in comparison to the MA fund market. While MA funds currently control the larger share of AUM, the gap is closing. In the last 6 years Defaqto have witnessed an 100% increase in the number of MPS solutions coming to market, with a relative plateauing in the number of new MA fund solutions launching in the UK market over the same timeframe ending with a slight decline in 2024, as demonstrated in Chart 4.

Chart 4 shows number of solutions being launched

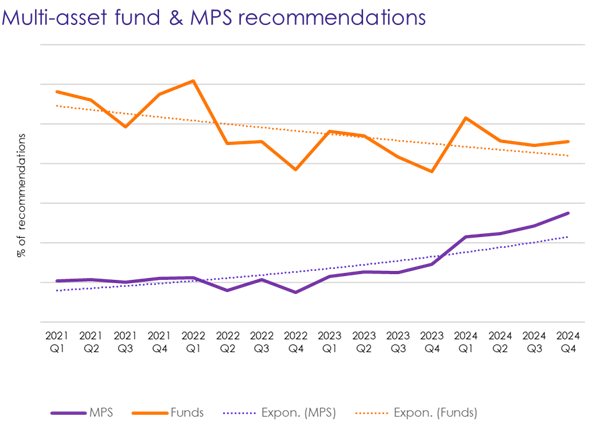

But has the rapid growth in the MPS market that we’ve experienced in recent years been as a result of demand or has it been DFMs predicting future uptake of MPS portfolios?

The Chart 5 shows that since Q1 2021 there has been a rapid growth in adviser recommendations also, in line with the increasing supply of MPS portfolios in the market. Based on new business adviser recommendations, we can see that coinciding with the Consumer Duty, the growth in adviser recommendations has been increasing for MPS but declining for MA funds as more advisers look to use MPS solutions as part of a CIP.

Chart 5 shows multi-asset fund & MPS recommendations

There is an argument that these lines have already crossed in that the above graph shows recommendations, whereas we know there is a lot of generic research for CIP inclusion.

Costs are falling

Part of the growth in the MPS market can also be attributable to the reduction in cost. This is in part due to newer DFM propositions deliberately setting up to be more competitive, but also as a result of the knock-on effects of funds experiencing a fall in charges, meaning underlying investments in MPS portfolios are consequently cheaper.

There does also seem to be increasing use of passive instruments within portfolios, a cheaper option than active funds, and there is also no doubt that regulation has made costs much more transparent, in particular MIFID II in 2018 and also the cumulative effects of Fair Value assessments and The Consumer Duty.

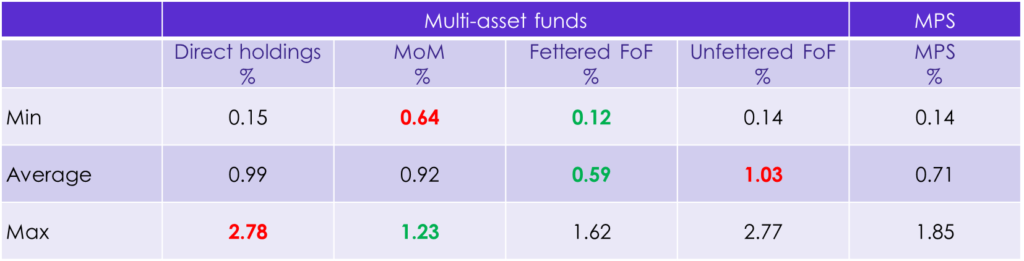

Table 1 illustrates the total ex-ante MiFID II costs and charges for each segment of the multi-asset market. MPS was once considered to have a higher average cost when compared with MA funds but are now on an even playing field when it comes to total cost of ownership.

Table 1 shows the total ex-ante MiFID II costs and charges for each segment of the multi-asset market

This is good news for clients as long as these falls are not lost elsewhere in the distribution chain. While there may be mitigating circumstances for higher costs, perhaps they are temporary until economies of scale kick in for example, advisers should be questioning some of these significantly higher numbers. In other words, they should be thinking ‘value for money’ as well as absolute cost.

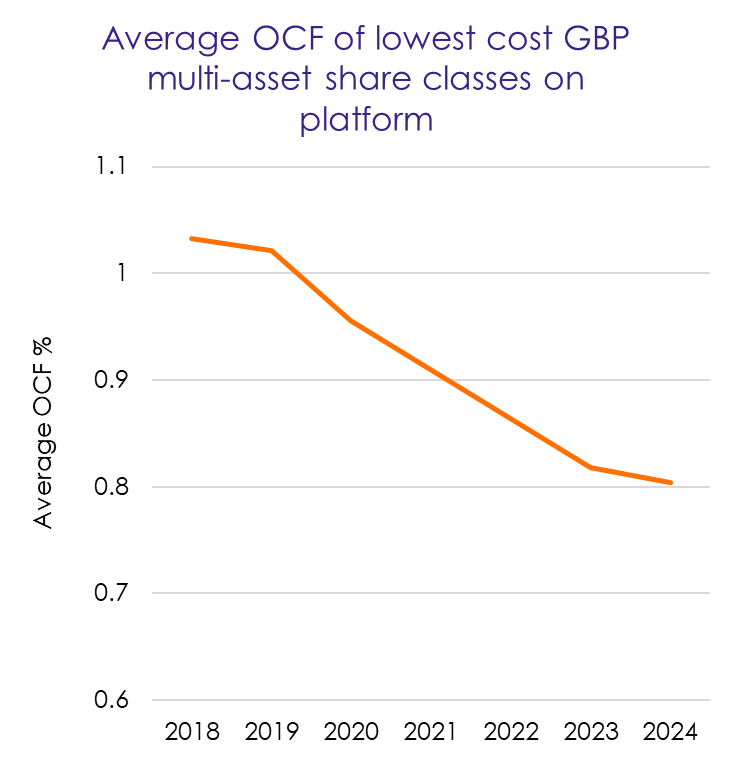

As mentioned, we have also experienced significant decreases in the OCFs of MA funds since the inception of MiFID II – as shown in Chart 6 – in which it became a regulatory requirement for authorised fund managers and DFMs to increase the transparency of their cost and charges.

Chart 6 shows OCFs of multi-asset funds

What does the future hold?

We expect to see the market for DFM MPS plateau in terms of new solutions coming to market, However, maturing over the next five years in terms of AUM as advisers continue to utilise risk rated MPS solutions to match to their client’s risk profiles and utilise MPS solutions for their client’s decumulation needs. Multi-asset funds are already a more mature market and we would expect to see steady growth in AUM continue.

With literally thousands of options to choose from, and some with worryingly low AUMs it is always tempting to predict consolidation in the market. However, experience tells us this doesn’t happen beyond the occasional bouts of M&A activity. We would not expect the breadth of choice to change much from this point.

With one exception. A significant proportion of the rapid growth in MPS solutions has been sustainable and ESG solutions. When the regulator determines the SDR requirements for DFM MPS providers, we may see name changes, mergers and closures of portfolios.

Now that DFMs are required to produce Fair Value Assessments, The Consumer Duty is more embedded in the industry and transparency, particularly around cost, is increasing, not to mention the increasing competition in the market, we would expect to see costs continue to fall.

We may see the regulator carrying out similar reviews as to those carried out following the requirement for authorised fund managers to publish Assessment of Value (AoV) reports back in 2019. This will force DFMs to be more explicit and transparent with their fair value assessments. In which DFMs may need additional external data sources to help aid them with meeting the demands of the regulator.

We haven’t mentioned performance. MA funds are classified under the relevant IA sectors, generally the mixed asset sectors. This has given the funds an advantage in the past as it meant they can be compared against sector averages. Until very recently, the same like for like comparisons could not be done for MPS portfolios as there were no peer group averages in the market. This is changing and will add to the robustness of adviser due diligence. Last year Defaqto launched a series of 5 risk based MPS portfolio peer group averages created from real life portfolios across the whole of the market. Under Consumer Duty, we expect the use of these ‘Comparator’ averages to quickly gain traction.

But what about the MA funds market. Under the new SDR regulation, we may start to see some of the smaller funds close as the additional operational overheads force the hands of the managers, with some consolidation in the form of fund mergers as a result of SDR. However, for those funds that adopt a label approach their clients will receive enhanced reporting and unparalleled transparency when it comes to sustainability disclosures.

What have we learnt?

Multi-asset investing is here to stay and is a sensible approach to managing a client’s portfolio. It means outsourcing to experts, generally benefiting from economies of scale and achieving suitable portfolio diversification.

Both the funds and MPS markets are mature in terms of choice, but advisers need to be mindful of the likely level of support for very small funds and portfolios and judge whether they have longevity.

Frustrating and sometimes costly as it can be, both in terms of fees and time resource, regulation is there to protect the client. We have seen costs come down and looking at the bigger picture, it is much more likely that client outcomes will be met if investing is outsourced to third party expert asset managers.

About Fraser Donaldson

Fraser is an Investment Consultant at Defaqto. He has more than 40 years of experience working in the investment industry and more than 30 years at Defaqto. In that time, he has focused exclusively on investments, in particular collective investments and discretionary management and their distribution through tax wrappers and adviser platforms. For the last 15 years his focus has been on discretionary management, ensuring Defaqto maintains its position as the industry’s pre-eminent source of comprehensive discretionary management information and analysis.

About Mike Turner

Mike is Investment Development Consultant at Defaqto. He has over 20 years’ worth of industry experience covering funds, DFM, products and platforms. Mike is positioned within the Defaqto Investment Insight team where he’s responsible for risk rating MA solutions, conducting Fund/MPS reviews, ESG reviews and shaping Defaqto’s data proposition to ensure that advisers have access to new and relevant data, to help them fulfil client suitability in an ever-evolving regulatory landscape.