“Elevated valuations and concentration are driving investor caution” and “pushing allocators to reassess the role of alternative strategies” – “particularly those that are less dependent on market direction”, explains Paul Lacroix, Head of Products at Ossiam in his latest analysis.

“Macro-driven outcomes have become structurally harder to forecast. Inflation dynamics, policy responses, and growth trajectories are more uncertain and less synchronized than in previous cycles. As a result, market returns are increasingly shaped by episodic macro shocks rather than stable, trend-driven regimes…This shift naturally favours equity market neutral strategies, whose return streams are designed to be largely independent of broad economic scenarios.

“By focusing on relative value rather than market direction and by leveraging favorable dispersion, correlation, and funding dynamics, they [equity market neutral strategies] offer a compelling approach to diversification and absolute return generation in an increasingly complex and uncertain investment landscape.”

Key analysis:

- Elevated skew in the options market

- Low implied correlation in the S&P 500

- High cross-sectional dispersion in the S&P 500

- Supportive funding conditions

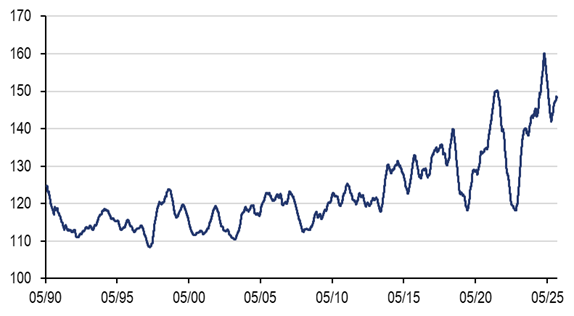

“Concerns are clearly visible in the options market through the level of equity index skew…When skew is high, investors are willing to pay a significant premium for protection against market declines relative to participation in upside moves. In other words, skew captures the market’s assessment of downside tail risk rather than its central volatility outlook. A persistently elevated skew therefore signals that investors are increasingly concerned about the severity of potential drawdowns, even if near-term volatility remains contained.”

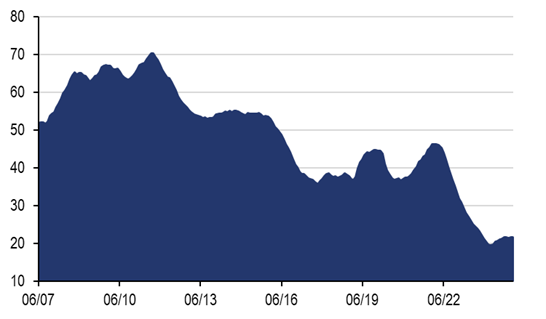

“Implied correlation measures how closely individual stocks are expected to move together, as inferred from option prices on equity indices and their underlying constituents. High implied correlation suggests that macro factors dominate, causing stocks to move in unison. Low implied correlation, by contrast, indicates that company-specific factors such as fundamentals, earnings, and positioning play a larger role. Low implied correlation is particularly favourable for market neutral strategies, as it enhances the ability to distinguish relative winners from losers.”

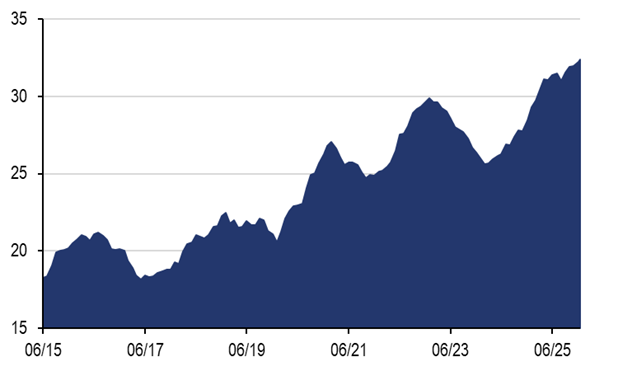

“Elevated dispersion implies that even when index-level returns are muted, individual stocks can experience very different outcomes. From an active perspective, high dispersion expands the opportunity set for relative value strategies, as the performance gap between outperformers and underperformers widens. Taken together, low implied correlation and high dispersion point to a market environment rich in idiosyncratic opportunities, precisely the conditions under which equity market neutral strategies tend to perform best.”

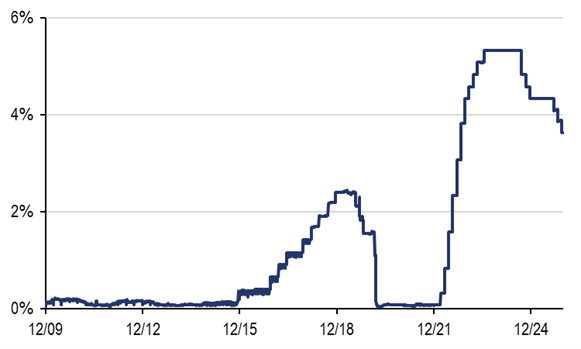

“Short-term interest rates remain elevated compared to the latest decade, as reflected in money market benchmarks such as SOFR. For market neutral strategies that efficiently manage leverage and maintain positive cash balances, higher funding rates translate into a meaningful carry component. This carry provides a structural contribution to returns and can enhance the resilience of performance across market regimes.”

![[UNS] celebrate](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/801986-featured-300x200.webp)