Gold’s multi‑year rally has been underpinned by an unusual convergence of central bank buying, heightened geopolitical risk, and renewed concerns around currency debasement. However, while these forces have supported a powerful rise in prices, they also introduce fragility should any of these drivers fade.

Recent market moves underscore the potential for volatility should sentiment shift. On the final trading day of January, markets reacted sharply to the surprise nomination of Kevin Warsh as the next Federal Reserve Chair. Viewed as a more orthodox and less politically influenced policymaker, Warsh’s nomination challenged the prevailing debasement narrative.

Gold prices fell by 9.5% in a single session, with further weakness in the following days. The sell‑off spread quickly across precious metals, with silver declining nearly 30% in one day, highlighting the sensitivity of these markets to shifts in expectations.

In contrast, Aberdeen Investments believes copper and copper miners could present a more durable and compelling investment case, supported by clearer long‑term demand growth, tightening supply, and superior equity leverage to the underlying commodity.

Ben Shrewsbury, Investment Manager – Global Emerging Market Equities, at Aberdeen Investments and co-manager of the Aberdeen Future Minerals Fund, says:

“Gold’s rally has been impressive. However, it is increasingly dependent on factors that may prove transient, supported by an unusual mix of central bank buying, geopolitical risk premia, and renewed concerns around currency debasement.

“While these factors qualitatively justify the price strength, they also introduce fragility should any of them unwind. We also remain cautious on gold miners given their structurally weaker capital allocation and margin erosion over time.

“By contrast, we find greater conviction in copper and copper miners, where both demand and supply dynamics point to an enduring structural deficit, and where mining equities have historically offered cleaner leverage to the underlying commodity.”

Aberdeen Investments believes copper’s fundamentals are anchored in durable structural trends rather than the volatile geopolitical or financial flows seen in gold.

Demand is accelerating as global electrification gathers pace, driven by renewable energy, grid expansion, electric vehicles, data centres and digital infrastructure. At the same time, supply is tightening as existing mines mature, copper reserves decline and years of underinvestment limit the pipeline of new projects.

With the development timeline for new copper supply often stretching close to a decade, higher prices are unlikely to deliver a rapid supply response. This points to a structural deficit and a prolonged period of market tightness – a long‑cycle environment in which it would appear copper miners are well positioned to deliver attractive returns.

Gold’s break with history

Gold has been in a sustained upcycle since 2022, rising from around $1,800 per ounce at the start of 2022 to a peak of over $5,200 per ounce in January 2026. The early phase of this rally was particularly notable for breaking with gold’s long‑established relationship with interest rates.

Historically, rising yields have reduced the appeal of non‑yielding assets such as gold. However, gold prices have continued to climb even as rates have increased, signalling a shift in the underlying drivers of demand. This decoupling reflects a broader reassessment of gold’s role within portfolios, driven less by traditional monetary dynamics and more by geopolitical considerations.

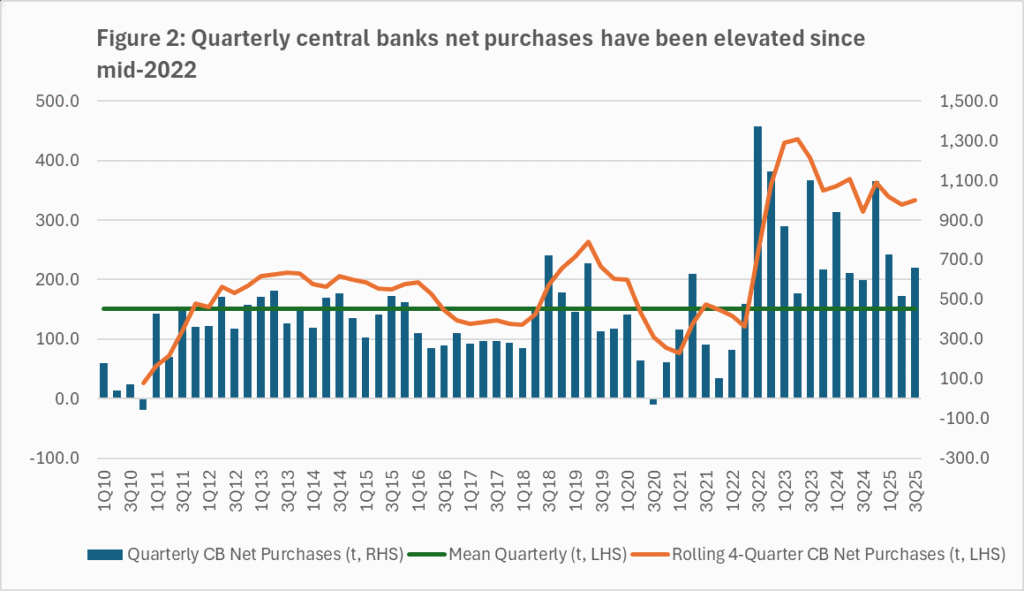

A key catalyst for this change emerged in 2022 following Russia’s full-scale invasion of Ukraine and the subsequent escalation of financial sanctions. These events prompted renewed scrutiny of reliance on the US‑centric financial system and the security of dollar‑denominated reserves. In response, central banks across a wide range of countries – including Poland, Turkey, India, and the Czech Republic – significantly increased gold purchases.

Source: World Gold Council, Bernstein Estimates

Although the pace of central bank buying has moderated slightly, demand remains elevated, providing a pillar of support for gold prices.

Safe havens and the debasement trade

The second leg of gold’s rally began in 2024 and accelerated through 2025, driven largely by investment flows rather than official sector demand. Escalating tensions in the Middle East, increased friction between major global powers and renewed trade disruptions all contributed to a rising geopolitical risk premium, reinforcing gold’s appeal as a “safe‑haven” asset.

At the same time, concerns around monetary policy and fiscal sustainability intensified. Political pressure on the US Federal Reserve to cut rates despite inflation remaining above target, combined with historically high sovereign debt levels, renewed concerns around currency debasement. These dynamics spurred strong ETF inflows into gold, alongside rising physical bar and coin demand.

A reminder of gold’s fragility

While these factors have aligned to support gold, recent market moves underscore the potential for volatility should sentiment shift. On the final trading day of January, markets reacted sharply to the surprise nomination of Kevin Warsh as the next Federal Reserve Chair. Viewed as a more orthodox and less politically influenced policymaker, Warsh’s nomination challenged the prevailing debasement narrative.

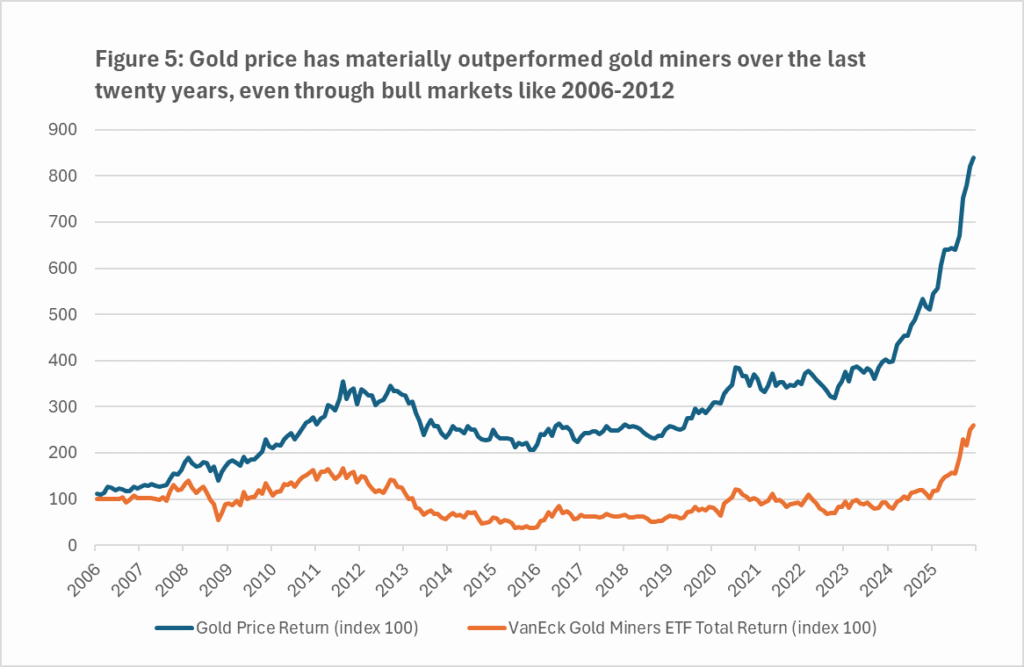

In addition, despite continued support for physical gold, Aberdeen notes that caution remains warranted toward gold mining equities, and believes that over the long-term, investors have generally been better served by owning physical gold rather than miners. Rising commodity prices tend to be accompanied by rising input costs, eroding margins and diluting operational leverage.

Source: FactSet

Moreover, the gold mining sector has a poor track record of capital allocation, Aberdeen says, often characterised by mergers and acquisitions which add little value and poorly timed growth investments. Over the past two decades, physical gold has outperformed gold mining equities, even after accounting for dividends.

![[UNS] celebrate](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/801986-featured-300x200.webp)