Understanding a client’s attitude to risk has long been a cornerstone of financial planning, but when it comes to retirement, advisers must look beyond risk tolerance alone. In this article, Louis Williams, Head of Psychology and Behavioural Insights at Dynamic Planner, explores why capturing clients’ retirement income preferences is becoming increasingly important.

For over 20 years Dynamic Planner has used psychometric questionnaires to assess attitudes to risk, with the latest edition being developed in conjunction with Henley Business School in 2018, adding the ability to extract financial personality insights from responses in 2025. Built using academic research, psychometric testing principles, statistical analysis and data modelling, Dynamic Planner’s Attitude to Risk Questionnaire (ATRQ) is a robust measure with questions that are tested for reliability and validity each year. It is a measure that is suitable regardless of a client’s life phase, so there is no need for an accumulation and decumulation alternative.

A client’s attitude to risk may change during different stages of their life, but this will be captured in a well-designed questionnaire. Dynamic Planner’s psychometric ATRQ is agnostic. In fact, willingness to take risk naturally tends to decline as clients get older and therefore it’s important that one measure is continuously used over the lifetime which does not change simply because a client has transitioned into another life phase. One measure, like Dynamic Planner’s, can be used as it considers attitudes more broadly to understand changes and to avoid miscalculating a client’s willingness to take risk. In any science, changing the test while also changing the conditions results in unreliable data – was it the client’s attitude that changed, or the tool measuring their attitude?

It goes without saying that it is crucial to capture changing conditions and circumstances to offer meaningful advice. Attitude to risk is but one element for consideration, there is a wider picture, including the client’s capacity for loss, their goals, knowledge, experience and vulnerability. However, it also becomes important to capture a client’s income preferences when considering their retirement plans. This is not an issue solely about risk tolerance, but income factors and priorities of a client as they transition into retirement.

Dynamic Planner’s Retirement Income Questionnaire (RIQ) was launched in 2025 and is positioned between client profiling and solution selection to encourage clients to consider their high-level retirement income preferences in a way that is long standing and not solution specific. The output is a summary that enables the adviser to match available solutions and tailor the advice and recommendations to the clients’ preferences and expectations.

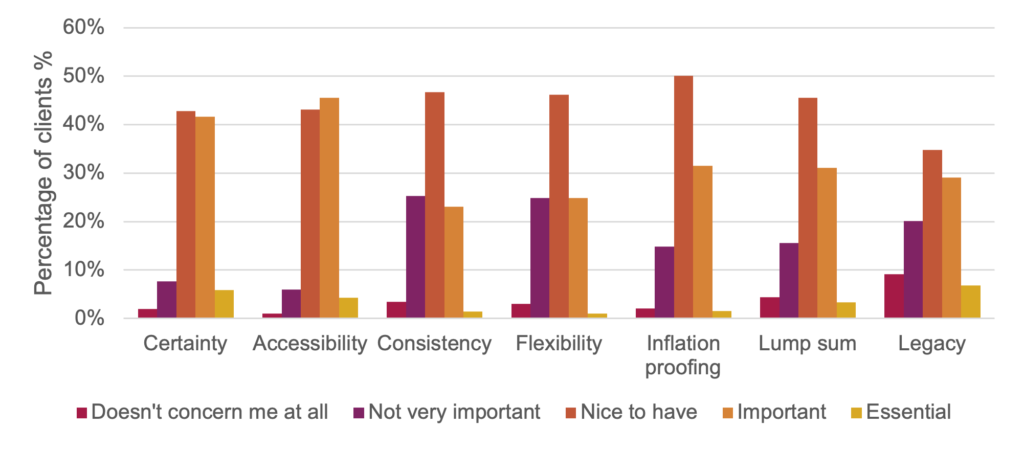

The questionnaire takes into consideration a client’s desire for:

- Certainty – Having necessary expenditure covered for life

- Accessibility – Taking income as and when they want to

- Consistency – Having a fixed income

- Flexibility – Having the ability to vary income

- Inflation proofing – Protecting against future inflation

- Lump sum – Having the ability to take lump sums

- Legacy – Being able to leave something behind

Furthermore, it helps ascertain if clients are willing to make any lifestyle changes during retirement to increase their income and assesses their desire to make a permanent decision at the time in which they complete the questionnaire. This question set is differently to industry-standard tools for assessing risk tolerance, but it compliments Dynamic Planner’s existing client profiling process to gives advisers greater insight into their client’s retirement preferences and requirements.

Some of our early findings from circa 5,000 advised clients completing the RIQ questionnaire in 2025 shows that there is a stronger preference for certainty and accessibility with consistency and flexibility being of less importance for clients.

Access to demographic variables such as age, gender, and marital status provides additional context for interpreting our dataset. For example:

- Females have a greater need for certainty and consistency, and would like to protect their income against inflation, whilst males care more about leaving something behind after they’re gone.

- Males are also more willing to make changes during their retirement to increase their income and are more likely to be ready to make a lasting decision about their retirement plan.

- Younger clients care less about certainty and consistency, and those between 46 and 75 would like flexibility and the ability to take lump sums.

- A trend regarding leaving a legacy, shows that younger adults (26-45) and older adults (over 75) view this to be important, potentially due to having younger family members to care for.

- Those between 46-55 are more willing to return to work, if necessary, but older clients are both less willing to cut back on expenditure and return to work. As expected, they are more ready to make lasting decisions regarding their retirement plans.

- Married individuals are more likely to want to leave something behind after they’re gone and less willing to return to work during retirement.

Assessing attitude to risk is important, and Dynamic Planner includes a robust measure within its suite of profiling questionnaires, however a decumulation specific attitude to risk questionnaire is not necessary when a client enters retirement. In fact, a change in measure can cause more issues for both client and adviser. An attitude to risk measure should be suitable regardless of the life stage of a client and it should assess relevant dimensions of risk tolerance, such as a client’s emotions and their abilities to tolerate uncertainty. Multiple measures can lead to a miscalculation of risk that the client is willing to take, but one reliable measure allows us to analyse changes in risk tolerance over time. Therefore, Dynamic Planner provides its RIQ to be used alongside it’s universal ATRQ to enable meaningful and consistent conversations to be held between advisers and their clients as they enter retirement.

Dr Louis Williams, Head of Psychology and Behavioural Insights:

Dr Louis Williams is Head of Psychology and Behavioural Insights at Dynamic Planner, and a Visiting Fellow at the University of Reading. He specialises in behavioural science, applied psychology, eye movement behaviour and aesthetics. Louis holds a PhD in psychology and has worked with Dynamic Planner since September 2019, when the business embarked on its government-sponsored behavioural science and investment project with Henley Business School. Louis is an experimental psychologist and has worked with universities across the globe on multidisciplinary research projects. He is keen to use experimental methods and apply findings to help financial planning clients make better decisions. He is an experienced teaching fellow and has attained fellowship of the higher education academy.

![[UNS] celebrate](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/801986-featured-300x200.webp)