Following speculation* over the weekend that the Chancellor, Kwasi Kwarteng, is reviewing pension tax allowances, Aegon has set out why increasing frozen limits at a time of rampant inflation is important to the future of the pensions system and the retirement livelihoods of hundreds of thousands of individuals.

Steven Cameron, Pensions Director at Aegon said:

“The pensions system has many limits on how much an individual can have in their pension without suffering tax penalties, as well as numerous rules around the maximum which can be paid in each year. Many of these have been fixed in money terms for many years, and others were frozen by Rishi Sunak back in 2020. These need an urgent overhaul, particularly at a time of rampant inflation.”

Pensions Lifetime allowance

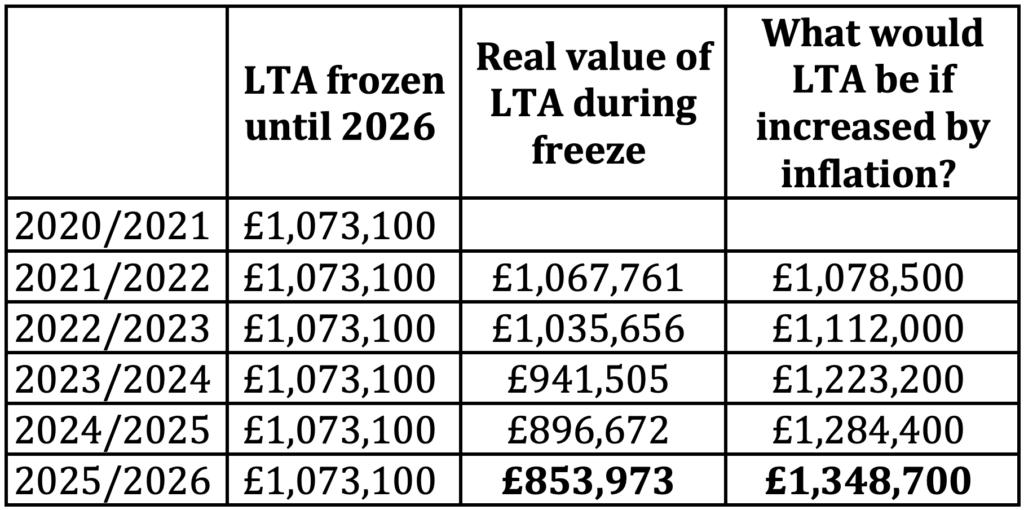

“The pensions lifetime allowance has been frozen at its 2020/21 level of £1,073,100 until 2026, rather than increase annually in line with inflation. While we didn’t expect any changes in last week’s mini-Budget, we very much hope this is now moving up the Chancellor’s in-tray. If left unchanged, it could cause real and long-term damage to the UK pension system and the retirement livelihoods of thousands.

“The freeze, coupled with spiralling inflation, means in purchasing power terms the maximum you can have in a pension without suffering tax penalties is plummeting. If inflation averages 10% next year and falls back to 5% for the following 2 years, Aegon analysis shows that freezing the pensions lifetime allowance means its value will have fallen by over 20% in real terms by 2025/26. On these assumptions, had it increased in line with inflation, it would have reached £1,348,700 by 2025/26.

“Looking at it another way, someone who starts taking an income in 2025/26 with a fund of £1,348,700 wouldn’t have been above the lifetime allowance if there had been no freeze. But under the freeze, they could have to pay 55%** tax on the difference of £275,600. This means they could face a huge tax penalty of £151,580 just when they need their full pension more than ever to fund a comfortable retirement and cover potential future social care costs.”

**There is currently a 55% tax charge on pension funds taken as a lump sum above the lifetime allowance

Table: Impact of soaring inflation on the Pensions Lifetime Allowance

Aegon Analysis: Figures use actual inflation to 2022/23 and assume an average inflation rate of 10% for 2023/24 and 5% for 2024/25 onwards. LTA increase rounded up to the next £100.

Aegon Analysis: Figures use actual inflation to 2022/23 and assume an average inflation rate of 10% for 2023/24 and 5% for 2024/25 onwards. LTA increase rounded up to the next £100.

Annual Allowances

“As well as the pensions lifetime allowance, there is also a limit on how much an individual and their employer can contribute to a pension each year. Including the Government tax relief top-up, this is £40,000 a year and has been since 2014 meaning it is now far less generous after allowing for the effects of inflation. There are complex lower limits for high earners under a ‘tapered annual allowance’. As well as being long overdue for an increase, there’s a real question over why there needs to be both a lifetime limit and an annual limit.”

Money Purchase Annual Allowance

“Another little-known limit which needs to be increased is the ‘Money Purchase Annual Allowance’ (MPAA). This allowance reduces how much can be paid into a pension each year from the £40,000 ‘Annual Allowance’ to just £4,000 per year once an individual has accessed their pension flexibly, an option availability to those aged 55 and over.

“The MPAA isn’t increased in line with inflation, but the pandemic and cost-of-living crisis has highlighted the unsuitability of the £4,000 limit for the current world of work and economic situation. Over 55s may have dipped into their pension for financial support during the pandemic and cost-of-living crisis without knowing this comes with a sting in the tail if they then want to rebuild their pension by making future pensions contributions.

“We’d urge the government to increase the MPAA to ensure people who have been adversely affected by the pandemic and cost of living crisis are not left disadvantaged in their ability to rebuild their pension savings. Increasing the MPAA limit to at least £10,000 would go some way to help those individuals whose retirement plans have been thrown into disarray since the beginning of the pandemic. Bringing it fully into line with the Annual Allowance would also be a welcome simplification.”

*Report in the Sunday Telegraph

Find out more about Aegon

Also, be sure to read our mini-budget update right here on IFA Magazine.