Pension withdrawals have spiked as the cost-of-living crisis forces savers to raid retirement pots. AJ Bell’s head of recruitment policy, Tom Selby, has weighed in on this matter.

- Pension withdrawals surged at the start of 2022 as the cost-of-living crisis forced savers to dip into their retirement pots, new HMRC data shows (Private pension statistics commentary: September 2022 – GOV.UK (www.gov.uk))

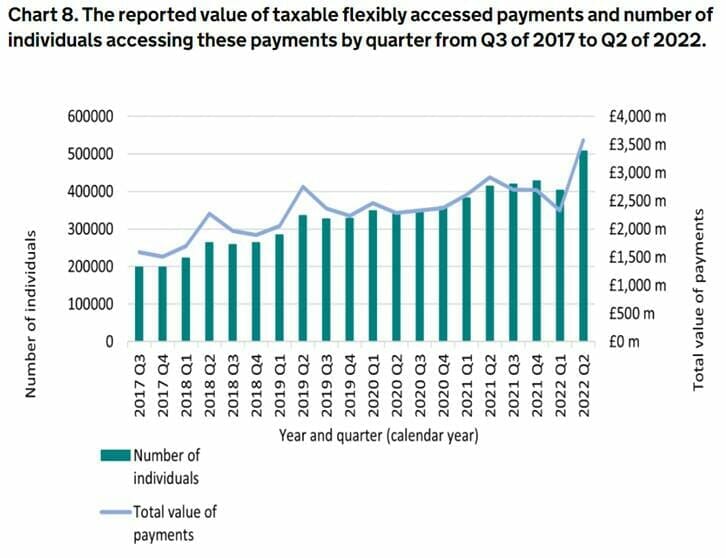

- A staggering £3.6 billion of flexible pension withdrawals were made between 1 April and 30 June 2022 – a 23% increase compared to the same period in 2021

- Over 500,000 people accessed their pension in the second quarter of 2022, with the average withdrawal over the period standing at £7,000

- Across the 2021/22 tax year, £10.6 billion of flexible withdrawals were made by savers, up from £9.6 billion in 2019/20

- Treasury urged to consider increasing the money purchase annual allowance (MPAA) so people can rebuild their retirement pots once the current crisis eases

Tom Selby, head of retirement policy at AJ Bell, comments:

“Today’s numbers provide clear evidence that squeezed savers are being forced to turn to their pension pots to make ends meet during the cost-of-living crisis.

“In the first three months of the 2022/23 tax year, over half a million people withdrew £3.6 billion from their retirement pots, a 23% increase versus the same period in 2021/22.

“While we don’t know exactly what has driven this behaviour, the most likely culprit is spiralling inflation. With millions of families struggling to pay the bills at the moment, for many turning to their hard-earned pensions will feel like the only option. There will also inevitably be lots of parents or grandparents who are taking some income from their pensions to help younger generations get by.

“Anyone accessing their pension or increasing withdrawals as a result of inflation needs to consider the long-term impact of this decision. Accessing your pension early, or upping your withdrawals, will put the sustainability of your retirement plan under strain.

“This may be a secondary consideration for people truly struggling as bills rise, but it’s crucial not to stick your head in the sand or make big decisions like this blindly.”

Source: HMRC

Ability to rebuild your pension restricted

“Anyone taking taxable income from their pension for the first time will also have their ability to rebuild their retirement pot severely restricted. Taking even £1 of taxable income flexibly from your pension will trigger the money purchase annual allowance (MPAA), permanently reducing your annual allowance from £40,000 to just £4,000. You will also lose the ability to carry forward up to three years of unused allowances in the current tax year.

“Given the severity of the current crisis and the impact it is having on behaviour, there is a strong case for increasing the MPAA back to £10,000 at the very least. Over the longer term, the Government should consider scrapping the MPAA altogether as part of a much-needed simplification of pension tax rules.”

How can people access their pensions without triggering the MPAA?

- Just take your tax-free cash. While accessing taxable income flexibly from your pension will trigger the MPAA, withdrawing your tax-free cash won’t. It is possible to ‘partially crystallise’ your fund so you just take out the tax-free cash you need, with the rest left in your fund and able to grow tax-efficiently.

- Take a small pot withdrawal. If your fund is worth £10,000 or less you can withdraw both the tax-free and taxable element flexibly without triggering the MPAA. You must extinguish the entire fund in order not to trigger the MPAA. You can take up to three small pot withdrawals worth £10,000 or less in your lifetime.

- Capped drawdown. Capped drawdown is no longer available, but some savers who were in capped drawdown before April 2015 have remained in it. Provided any withdrawals taken via capped drawdown do not exceed the maximum income limit (150% of the GAD annuity rate), the MPAA will not be triggered.

Find out more about AJ Bell.