By Geraldine Sundstrom, Asset Allocation Portfolio Manager, and Tania Bachmann, Equity Research Analyst at PIMCO

Whenever motorists pump gas these days, they get a painful reminder of Russia’s role in global oil markets. What’s been less appreciated is the range of raw and semi-finished products that Russia and Ukraine export. From palladium to wheat, disruptions are already putting upward pressure on prices across a range of everyday products, heightening macroeconomic and market risks over the coming quarters.

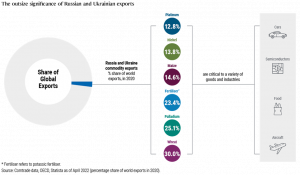

At first glance, Russia and Ukraine shouldn’t matter that much to global economic activity. Ukraine’s share of global exports is just 0.3%, while Russia’s is 1.9%. In contrast, China and the U.S. each make up roughly 10% of global trade.

Yet it’s a dramatically different story when it comes to key industrial inputs. As the graph shows, Ukraine and Russia are major exporters of palladium, nickel, grains, and other resources that are critical to a variety of goods and industries – from cars to semiconductors to groceries.

Palladium

Consider palladium, a chemical element and rare precious metal with a silver-white appearance. Russia produces more than a third of the world’s palladium, much of it for export. In addition to jewelry and dentistry, palladium is used to make catalytic converters that reduce pollution in exhaust from internal combustion engines. They’re mandatory in many countries. So automobile production – already slowed by pandemic- and supply-chain-related shortages of semiconductors – faces further disruption.

Palladium is just one example. Other key manufacturing inputs include fertilizer for agriculture, neon gas for semiconductors, nickel for steel, and ammonia for plastics.

Market impacts

Commodity markets have been quick to price in the supply/demand imbalances, but we believe economists and equity investors are behind the curve in assessing the impacts on growth and corporate earnings.

Shortages of primary inputs will be felt on both the demand and supply side of the equation. This runs the risk of snowballing and nonlinear negative impacts on broader economic growth while pushing inflation higher.

Second-order effects are already sprouting as higher input costs push prices higher, in some cases leading to demand destruction. In recent weeks, Europe has been hit by reduced or suspended production in select steel, fertilizer, and paper manufacturing facilities. The auto sector, already reeling from the semiconductor shortages of the past 18 months, has slowed production, leading industry experts to predict more delays and disruptions in coming months.

While interlinkages and pass-through effects are complex and hard to quantify, higher prices and demand destruction will slow growth and put upward pressure on prices – giving central banks an incentive to tighten policy faster than would otherwise have been the case.

Naturally, Europe will likely be hit hardest due to its proximity and economic ties to the combatants. Nonetheless, the interconnectedness of the global economy means that ripples will spread, from food prices in Egypt to prices of children’s toys in the U.S.

Importantly, as outlined in our Cyclical Outlook, “Anti-Goldilocks,” the disruptions come amid elevated economic uncertainty with high inflation, slowing growth, and tightening financial conditions, leading to a fragile and precarious market environment over the coming quarters.

Investment implications

For multi-asset portfolios, we believe this necessitates a more defensive stance and a focus on quality and liquidity, as the risk of recession rises over the cyclical horizon. Investors may want to avoid more cyclical sectors within equities, especially in Europe where the economic cycle looks most vulnerable in the near term, in our view.

Instead, we favor high-quality securities with pricing power and durable earnings growth, in areas such as semiconductor manufacturing and healthcare. We also like companies that can deliver sustainable upside potential in a slower-growth world, in areas such as renewable energy and automation.

At the asset allocation level, our strategy has been to broaden potential return drivers into interest rate and currency markets where we see better value, such as emerging market foreign exchange. We aim to keep overall directionality low while being dynamic in our risk management.

As always, volatility presents both risk and opportunity.