In truth no one enjoys thinking about death or dying and least of all their own funeral. However, without any plans in place, your clients’ loved ones will be left with the responsibility of making arrangements, which can add financial and emotional pressure at an already difficult time.

By making preparations now, your clients can put all their arrangements in place, as well as making their wishes known, which will simplify things when the time comes. It’s wise not to put off the inevitable, encourage your clients to take the time now to consider their funeral and what the costs are likely to be.

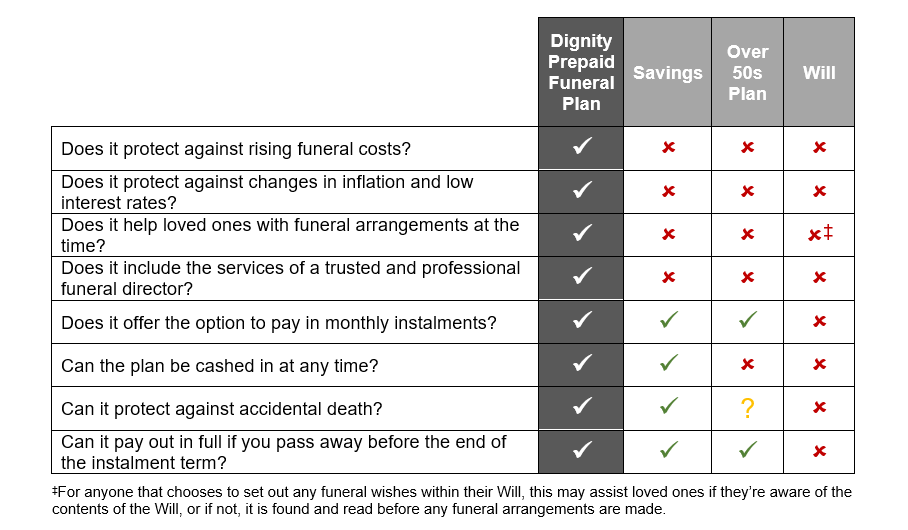

One of the first, and most important, things for them to consider is how they’re going to make provision for their funeral. There are many options open to them, some of which are outlined below.

Savings

Your clients could look to use their savings to settle their funeral costs. However, with interest rates currently so low, savings are struggling to keep up with inflation.

Funeral costs have risen much faster than inflation. Between 2011 and 2019, average funeral costs increased from £2,971 to £4,202*. That’s a 41% rise. It’s a trend that’s been going on for a while and if this continues, by 2028**, we project the average UK funeral could have risen to £6,206.

In addition, if your clients rely on their loved ones paying for their funeral from their savings, the accounts may be frozen upon death and, in some instances, the cash only released to the Will beneficiaries once the cost of winding up the estate has been met.

A Will

Using their estate to settle their funeral costs might be a possibility. However, this could lead to problems for the loved ones they leave behind.

Locating the Will can sometimes be difficult for the family after the person has passed away. And making sure there’s time for it to be read before the funeral may not always be possible.

Many families also have to go through probate, which might result in a possible delay in releasing funds to pay for funeral director’s services and third party expenses, which often have to be paid for up front, or very soon after the funeral.

Over 50s life insurance

Another option is to take out a life insurance plan – usually known as an ‘Over 50s Whole of Life Insurance Plan’. Such plans guarantee to pay a fixed cash amount towards your clients’ funeral costs, however, they also need to be aware that the cash sum may not cover the whole cost of their funeral.

Premiums and cover remain fixed while the plan is running, but because the cash amount is fixed, inflation will reduce the value of the payout over time.

The cash amount is payable upon their death or when they reach 90 (whichever comes first), as long as they have paid the premiums for a specified minimum period. However, if they fail to keep up the premiums, cover will stop, and they may lose any cash-in value. In addition, depending on how long they live, they could end up paying a lot more in premiums than the plan will pay out.

Funeral Plans

With some 165,000 funeral plans sold† in 2019, this is an increasingly popular choice for many people. A funeral plan allows your clients to arrange and prepay for their funeral in advance, which means costs for services in the plan are fixed at today’s prices. Funeral plans also help to protect loved ones from the stress of arranging and finding the money to pay for the funeral when the time comes.

Before your client takes out a funeral plan, it’s essential to check with the funeral plan provider which costs are covered by the plan. This means they can further protect their loved ones from having to meet any additional or unexpected costs in the future.

Most funeral plans will guarantee to cover the funeral director’s costs and other third party fees such as the crematorium and Minister or Officiant’s fees. However, some plans only provide a contribution towards those costs. It’s advisable to look for the plans that guarantee these costs will be covered, for greater peace of mind.

Your client’s family will usually be assigned a local funeral director who will assist when the time comes. Some larger plan providers operate a free telephone bereavement advice and counselling service should the family need one.

Important factors to consider when choosing a product to cover funeral costs

Dignity introduced the UK’s first funeral plan in 1985. Since then, they have helped nearly one million people^ plan for their funeral in advance.

Peace of mind

If your clients choose to pay for their funeral plan over more than 12 months, and pass away before they’ve finished paying for it, Dignity will cover their outstanding balance.

Dignity won’t ask their loved ones to pay a penny more than they’ve already paid for all the services included in their plan.

That’s the Dignity promiseⱡ.

A trusted partnership

Dignity prides itself on being there to help people at one of the most difficult times of their lives. It does this with compassion, openness, care and respect. But perhaps most importantly, the service provided comes highly recommended by the families that Dignity serves – in fact, 98%^ said that they would recommend Dignity to friends and relatives.

As standard within its partnership model, Dignity combines a high quality proposition with competitively price funeral plans and the highest standards of customer service.

With a dedicated relationship manager, having expertise in the financial services and funeral markets, you’re fully supported from the start. Dignity also provides free training in all locations, either remotely or face to face.

If you’re interested in joining Dignity’s partner network, get in touch. Simply click here and one of Dignity’s Relationship Managers will contact you.

*2011 – 2019 Matter Communications independent research

**2019 – 2028: Forecast based on average annual compounded growth rate of 4.43% each year between 2011 and 2019

^Dignity plc Annual Report and Accounts 2019

†Funeral Planning Authority, https://funeralplanningauthority.co.uk/about-us/statistics/

ⱡPlease see the Instalment Payments section of the Funeral Plan Terms and Conditions for further details

Click here for more information about Dignity.

IFA Magazine is for professional advisers only. For full terms and conditions click here