Written by L&G’s Vanessa Sallows, Claims & Governance Director, Group Protection – Retail

Is the group Critical Illness Cover (CIC) market growth being impeded by lack of intermediary knowledge of the ins and outs of the product? And although sales of individual CIC last year took a significant leap, is there room for improvement here too? If so, on either count, it’s our role as an insurer to help equip intermediaries.

Alan Lakey, Director – CIExpert, who we spoke to for the purposes of this article, comments: “CIC is quite complex. And group CIC is quite different to individual plans. Most advisers don’t work in the group market and lack the knowledge of the sometimes subtle differences.”

So, to help with this, we’ve pulled together simple comparison tables to highlight the similarities and differences across individual and group markets. But first a brief overview of the current state of each market.

Group CIC market size

The group CIC market showed marginal growth last year, according to Swiss Re GroupWatch 2025.

The number of people insured increased by 4% to 839,872 in 2024, in comparison to 807,319 in 2023. And the bulk of those insured (567,990) sits with Flexible / Voluntary arrangements, as opposed to Employer-Paid (271,882).

Intermediary respondents to Swiss Re GroupWatch state they are cautious about the prospects for growth. The reason they give is the potential impact of the cost of living and other pressures for employees. Of course, group CIC is also subject to P11D – in other words, it’s taxable as a benefit in kind – and this might reasonably have an impact too.

In contrast though, Alan says there is “substantial potential” for the group CIC market “especially in the SME field, where many companies do not offer these benefits,” he says. “Many advisers fail to discuss these matters with company owners, maybe through a lack of knowledge and, therefore, confidence”.

Individual CIC market size

Meanwhile, sales of standalone CIC increased by 22%, from 109,959 in 2023 to 134,439 in 2024, according to Swiss Re Term & Health Watch 2025. The report says this steep increase in standalone sales indicates that CIC sales are slowly becoming less tied to mortgages as the main distribution channel.

So, if that is indeed the case, what is driving this growth?

Alan comments: “A prime reason is the use of menu plans where advisers may use standalone CIC and standalone Life to better protect a client. Also, those consumers who purchase online or direct from an insurer will likely purchase a standalone plan, without actually realising that an accelerated plan is available.”

Accelerated CIC is an option in some Life policies that allows for an early payment of the death benefit – in full usually, or sometimes a portion – if the policyholder is diagnosed with a covered critical illness. It should be noted that some policies may state that a severity level must be reached.

On a final note, the total number of new CI policies, attached to Whole Life cover and standalone combined, increased by 2.5% to 545,251 last year. And total new Term Assurance with CIC sales stood at 1,421,512, down 0.8% from 1,433,089 in 2023.

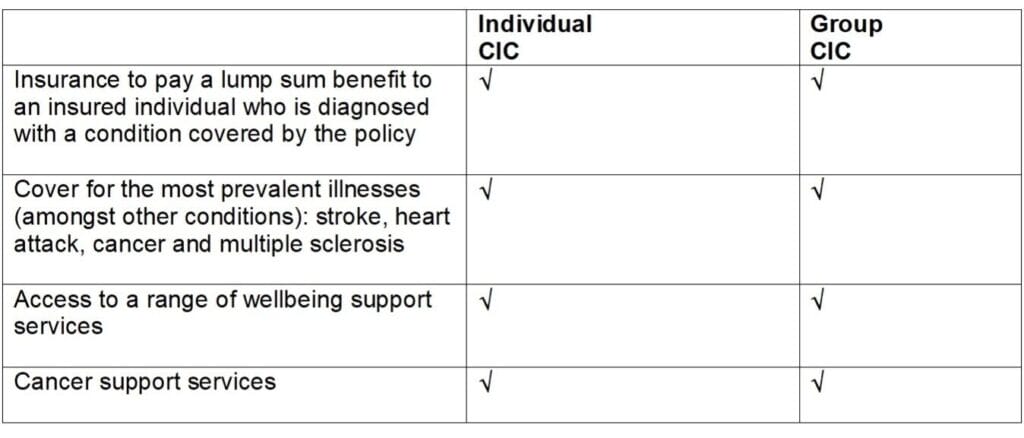

Similarities between individual & group CIC: A brief summary

Differences between individual & group CIC: A brief summary

| Individual CIC | Group CIC | |

| Immediate customer | Individual (self-employed, employee, contractor, gig worker). | Employing organisation of various minimum sizes, depending on provider. |

| Who can policy cover? | Individuals. Some providers will also automatically include the children of insured individuals, others will cover children for an extra charge. | Employees and equity partners – and their children – are automatically covered. And for an increased premium, the spouse or registered civil partner of insured employees may be covered. |

| Buying motivation | Traditionally sold in line with a significant life event (buying a house, having a family etc) to provide a financial safety net. However, the rise of menu plans seems to be changing this, as outlined earlier. | To help employers with recruitment and retention, CIC can be included as part of a comprehensive benefits package, or available under a flexible / voluntary arrangement. |

| Underwriting | Medical underwriting is required upfront as part of the purchasing process. This takes pre-existing conditions into account when making the decision. | Most employees are not subject to medical underwriting up to a free cover limit or ‘free limit’. If a scheme member needs a higher level of cover, additional medical information may be required. Employees are underwritten at point of claim. |

| Pre-existing condition exclusions | Not applicable. The application is underwritten at outset so all conditions are covered. | Pre-existing condition exclusions apply. Claims won’t be paid for any condition the insured person had at, or before, the start of their cover. |

| Related conditions | Not applicable. The application is underwritten at outset so all conditions are covered. | Within two years after new cover starts, if an employee has an insured condition that is related to a condition they had at the time (or before) the start of cover, they won’t be able to claim for it. But if they remain free of that condition and any associated, cover for that condition will start after two years. |

| Number of conditions covered | Typically, at least 30 core conditions. And, for an increased premium, the option to take additional cover for more conditions. | Typically, around 15 core conditions. And, for an increased premium, the option to take additional cover for more conditions. |

| Additional payments | All individual policies include additional payments (partials) for conditions such as lower grade cancers. | Not applicable |

| Changes to the policy | There is no renewal for individual CIC – it is a long-term product. Changes can usually be made during the policy term, but the type of changes and their availability depend on the insurer and the terms of the policy. | Changes can be made at renewal and at ‘lifestyle events’ including marriage, divorce and birth of a child. |

| Is the payout taxable? | No, if the individual is paying the premiums themselves out of already taxed income, any payouts are not taxed. | Yes, if the employer is whole or part paying the premiums, any payout will probably be subject to tax (but only on the portion the employer pays, where the cost of the policy is split). The benefit is also subject to P11D as a benefit in kind. |