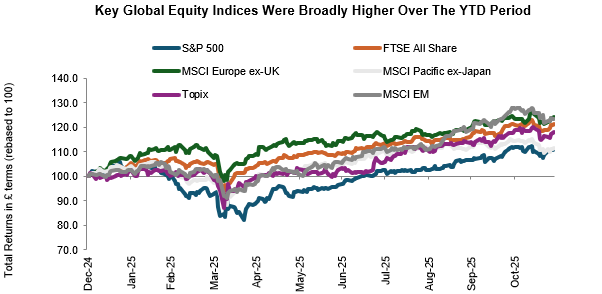

UK equity markets have staged a meaningful resurgence and are on course for their best calendar year since 2013, comfortably outpacing the US and other developed market peers year-to-date. While the market’s optimism and rise in valuations should warrant caution, according to Alex Wright, portfolio manager of the Fidelity Special Situations Fund and Fidelity Special Values PLC, meaningful discounts down the market spectrum lead to exciting opportunities.

Source: LSEG Datastream, 30 November 2025

Commenting on the year ahead, Wright said: “The UK enters the year from a position of strength. The market continues to trade at a meaningful discount to other major regions – both on outright price to earnings multiples and after adjusting for structural sector differences, such as the heavy weighting of technology in US indices. While bullish sentiment has driven valuations to more demanding levels across many global markets, the UK still offers many pockets of value, particularly further down the market cap spectrum. Our strategies maintain a structural bias towards these smaller and mid-sized businesses, as these businesses are typically less well known to investors and often receive limited and artificial coverage by the sell side.

“Domestically exposed areas have been weighed down by economic and political uncertainty. Interestingly, buying the UK market does not necessarily mean buying the UK economy. More than three-quarters of revenues generated by UK-listed companies come from overseas, providing investors with access to globally diversified earnings streams at valuations that remain attractive relative to international peers. The remaining quarter of the market, which is more domestically focused, has generally been held back, yet it offers selective opportunities where valuations more than discount a subdued backdrop. These unloved areas present compelling investment prospects and would benefit from a more stable environment in 2026 – though conditions do not need to improve materially for valuations to begin to recover.

Wright then turns to discuss his portfolio positioning for the year ahead: “We search for ideas across sectors and the market cap spectrum, focusing on unloved companies with the potential for positive change. We have been finding value further down the market cap spectrum as large-cap companies are trading close to their long-term averages, with the FTSE 100 on 14.2x forward price to earnings. Whereas mid-cap and small-cap companies remain materially undervalued, trading at 11.4x and 10.8x forward earnings respectively.

Diversifying financials

“While our investment process is driven by bottom-up stock selection, we categorise the market into super sectors to articulate positioning changes. Financials remain the largest absolute sector weight in the portfolio, but this exposure is highly diversified across a variety of sub-sectors, geographies and business models. Our weighting has moderated slightly due to increased takeover activity and profit taking within our insurance holdings. We continue to hold meaningful exposure across the banking sector, including emerging-market-focused Standard Chartered, domestic lenders Lloyds and NatWest, Irish banks AIB and Permanent TSB, as well other smaller banking positions.

Domestic-businesses spark interest

“We have actively recycled capital from defensive areas that have performed well such as tobacco and defence companies, and leaning into unloved, domestically focused businesses, with attractive turnaround stories. Particularly in consumer-related areas such as housing, furnishings, and home improvement, where volumes are depressed versus pre-Covid levels. UK household balance sheets are healthy, and savings rates elevated. With inflation easing and interest rates likely to follow, improving confidence could support consumption. These collection of businesses combine attractive stock-specific opportunities with depressed industry volumes, offering multiple catalysts to support a turnaround. While we are marginally leaning into domestically cyclical areas, we continue to strike the right balance with defensive earnings streams, notably in utilities, support services and non-life insurance.

Resources underweight position narrows

“Within resources, our underweight position has narrowed as we have identified selective opportunities. While our oil exposure has fallen over the past twelve months, our exposure to mining has increased. We remain underweight large-cap miners, reflecting our cautious view on iron ore, but hold a position in Glencore, supported by its attractive commodity mix and our constructive outlook on copper.

“Our analyst estimates point to an improving earnings backdrop for the UK market in 2026, with an even stronger outlook for our strategies. We remain confident in our holdings and in the UK market’s capacity to deliver attractive long-term returns.