“No investor, no politician and no central banker knows what is coming next, and whether inflation, stagflation or deflation will result from the combination of the interest rate rises, Quantitative Tightening, pay increases, record debts and the cost-of-living crisis,” says AJ Bell investment director Russ Mould.

“Going ‘all in’ on one scenario is probably not going to be good idea and portfolio construction will need to address a range of outcomes, as frankly anything is possible (especially given the likelihood of ongoing central bank and Government action). But carefully following five major investment themes may help investors sense which way the wind is blowing so they can try to obtain the best possible risk-adjusted returns for their portfolios, especially once they take the all-important issue of valuation into account.”

- The yield curve

“Central banks and policymakers are trying to manage inflation on one hand but do so without tipping heavily indebted economies into recession on the other (all while keeping an eye on their currencies and financial market stability for good measure). Given that central banks made a mess of it with their call that inflation would be ‘transitory,’ it would be logical to apply a large dollop of salt to their claim that they can engineer a ‘soft landing’ as they rein in inflation. American economist Rudi Dornbusch was never confident in their ability to use the blunt instrument to fine-tune economies, given his assertion, ‘None of the post-war (US economics) expansions ever died of old age. They were all murdered by the Federal Reserve.’

“Economists and investors will all be looking to macroeconomic data such as inflation, unemployment, job vacancies, wage growth and GDP to judge whether central bankers are getting the balance right or not, but they are all backward-looking – and markets are forward-looking.

“It may therefore be worth keeping an eye on the yield curve, on both sides of the Atlantic, using the relationship between two- and ten-year bonds as a benchmark.

“Usually, ten-year Government bonds will yield more than two-year paper simply because more can go wrong in the additional eight-year period. Investors will demand a higher yield as compensation for the added risk.

“But at the moment, two-year Treasuries in the US and two-year gilts in the UK are yielding less than their ten-year equivalents. This may be to due markets pricing in interest rate cuts in response to a slowdown or recession and can be a strong signal that a recession is coming. Note also how headline stock indices have historically tended to top out when the yield curve is at its most inverted and that was because the recession (as predicted by the yield curve) kicked in and took corporate earnings down with it.”

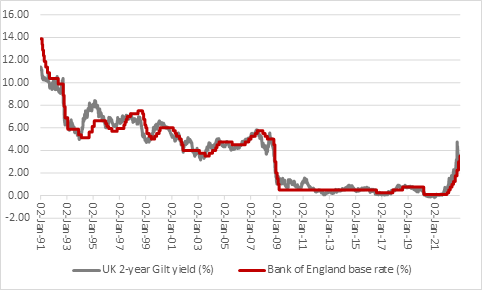

- Two-year Government bonds

“Equity investors can take another lead from the bond market by also following the yield on two-year US Government Treasuries or UK two-year Government gilts. This is because history suggests the two-year yield will lead monetary policy, as set by central banks, by some six months.

“History is no guarantee for the future – if it were, librarians would be the best and richest investors, as Warren Buffett tartly put it – but if this relationship holds firm, then the bond market could give a valuable steer as to whether rates are staying higher for longer or moving lower much quicker than expected.”

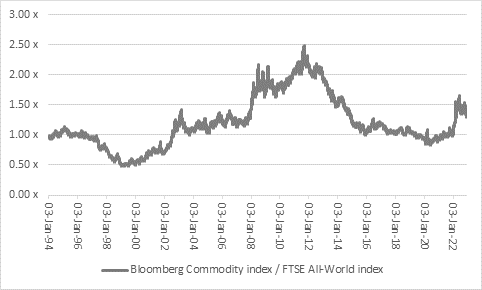

- Commodity prices (relative to share prices)

“The Bloomberg Commodity index, which follows the spot price of 23 different products ranging from oil to gold, wheat to cotton and hogs to cattle, is up around 10% in 2022, so it is doing better than every major stock market and beating the bond market hands down.

“But the index is still down by a fifth from its high, as the Turkey-brokered deal gets grain flowing out of Ukraine, oil prices sag as Europe mops up supplies of liquified natural gas (LNG) and fears grow that a recession will hit demand for many raw materials next year.

“If central banks succeed in reining in inflation, reasserting control and taking the world back to the low-growth, low-inflation, low-interest ‘Goldilocks’ environment that prevailed throughout the 2010s, then commodity prices could again stumble. They may also do so if we do indeed get a deep recession.

“But if inflation (or maybe stagflation) take hold, ‘real’ assets could come to the fore for three reasons: they could be stores of value; central banks cut rates or even start new QE programmes, even if such money printing would only reaffirm that they cannot print oil or gold; and investment in new resources finds is dwindling thanks to pressure from politicians, investors and the public alike amid environmental concerns.

“Commodities outperformed in 2021 and 2022 but by nothing like to the degree that ‘real’ assets beat ‘paper’ ones during 2001-02, so if this trend does get traction then there could be a long way to go yet.”

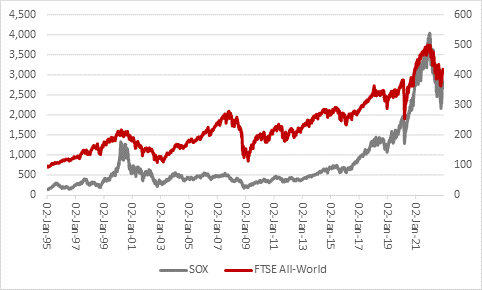

- Semiconductor stocks

“Silicon chips are a good guide to global economic health owing to their ubiquity – they are everywhere, from smart phones to laptops, car to industrial robots and servers to smart meters and global sales are expected to top $600 billion in 2023, to set a second consecutive all-time high.

“In addition, silicon chip stocks can be a good guide to investors’ risk appetite and global equity markets, at least judging by the past two to three decades. History is by no means guaranteed to repeat itself, but the 30-stock Philadelphia Semiconductor Index, or SOX, topped out six to nine months before the S&P 500 and FTSE All-World did in 2000 and 2007, to herald two thumping bear markets, and then bottomed out before those headline indices did in 2002 and 2009, to signal the start of a new bull market.

“The SOX is down by a third from its December 2021 all-time peak and profit warnings had started to pile up from its constituents, not least because inventories had begun to pile up, as end markets softened just as producers ramped up output in response to the shortages suffered in 2020 and 2021.

“Micron will report quarterly numbers in December and then it will be all eyes on Analog Devices, NVIDIA, Broadcom and also Taiwan’s TSMC, the world biggest semiconductor foundry (or third-party, outsourced producer) in January, as their results may set the tone for 2023. Good news would be reduced inventories, forecasts for normal, seasonal sales patterns in the early stages of 2023. Bad news would be a further bulge in unsold stockpiles, lowered revenue and margin guidance, and cuts to capital investment budgets.”

- Transport stocks

“Focusing on planes, trucks, trains and ships is nothing new when it comes to assessing the economy and the financial markets, but as a strategy it stands the test of time and could again therefore prove its worth in 2023 as central bankers, economists and investors try to assess whether inflation, stagflation or deflation would prevail (not least as all three will require different policy responses and asset allocation strategies).

“Robert Rhea’s Dow Theory argues that where the Transports go, the Industrials will surely follow. This is because in a strong economy, goods will need to be shipped and inventories and shelves replenished as product is sold to willing customers. The opposite holds in a weak economy as inventories pile up, new orders are postponed or cancelled and trains, trucks and ships sit idle.

“It can be argued this is less relevant to modern Western economies, which rely much more heavily on services than manufacturing, and intangible assets rather than plant and equipment, but services industries involved consumption too, and everything from food to clothes must still be transported somehow.

“Moreover, Rhea’s theory stood the test of time in 2022. The Dow Jones Transport index peaked in November 2021 and the Dow Jones Industrials did so in January 2022, although the Transports moved up from their autumn low just a week before the Industrials started their end-of-year rally. Whether the rolling stock continues to roll in could be a key consideration in 2023 and beyond.”