Written by Tom Selby, head of retirement policy at AJ Bell

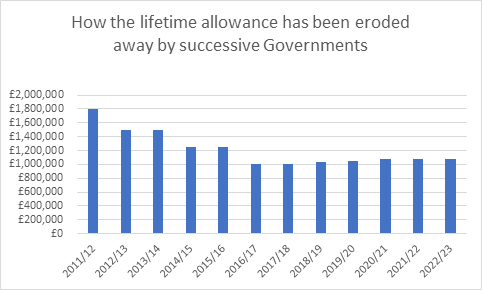

The lifetime allowance has been the subject of repeated attacks by successive Governments since hitting the high watermark of £1.8 million more than a decade ago.

The level was steadily eroded away from that point until 2017/18, when at £1 million a Consumer Prices Index (CPI) inflation link was introduced. That only lasted until 2020/21, however, after which Rishi Sunak – then the Chancellor of the Exchequer – froze the lifetime allowance at the slightly awkward figure of £1,073,100.

While the CPI link had been expected to return after 2025/26, it has been suggested the current Chancellor, Jeremy Hunt, is considering freezing the lifetime allowance for a further two years in next week’s Autumn Statement.

The impact a seven-year lifetime allowance freeze could have on retirement savings incentives is huge, with the lifetime allowance set to be almost £260,000 lower by 2027/28 than it would otherwise have been. This in turn would massively reduce the maximum tax-free cash someone can generate, to the tune of nearly £65,000.” (See table below for details)

Cap on retirement aspiration

Although a lifetime allowance of just over £1 million might sound like a huge amount of money, it puts a relatively low cap on people’s retirement aspirations.

Consider a healthy 65-year-old with a £1,073,100 pension pot – exactly the level of the lifetime allowance today – who takes their 25% tax-free cash (£268,275) and uses the remaining 75% (£804,825) to deliver a retirement income.

That could generate an inflation-protected drawdown income of around £35,000 a year for 30 years* in retirement – a very decent standard of living but hardly a king’s ransom. What’s more, by freezing the lifetime allowance, the amount £35,000 a year can buy someone will be eaten away by inflation.

The lifetime allowance also creates strange incentives. For example, it punishes people who enjoy strong investment performance – effectively acting as a disincentive for individuals to invest in the real economy, including the UK.

In addition, the lifetime allowance has horrific complexity for savers to navigate and firms to communicate – complexity which inevitably puts people off saving for retirement.

As such, it is in desperate need of reform – and ideally should be abolished altogether for defined contribution savers.

How freezing the lifetime allowance until 2027/28 could hit pension savers

| Year | Inflation rate | Lifetime allowance (if inflation uprating had been applied) | Actual lifetime allowance | Difference |

| 2021/22 | 0.50% | £1,078,500 | £1,073,100 | £5,400 |

| 2022/23 | 3.10% | £1,111,900 | £1,073,100 | £38,800 |

| 2023/24 | 10.10% | £1,224,200 | £1,073,100 | £151,100 |

| 2024/25 | 5.20% | £1,287,900 | £1,073,100 | £214,800 |

| 2025/26 | 1.40% | £1,305,900 | £1,073,100 | £232,800 |

| 2026/27 | 0% | £1,305,900 | £1,073,100 | £232,800 |

| 2027/28 | 2% | £1,332,000 | £1,073,100 | £258,900 |

Assumptions: inflation rate for previous September applied in each tax year and rounded to the nearest £100, for years 2024/25, 2025/26 and 2026/27 the Bank of England’s latest projections for Q4 in the previous year is used, for the increase applied in 2027/28 the Bank of England inflation target of 2% is used

Source: HMRC

*Assumptions: £35,000 starting income rises by 2% each year, investment returns = 4% per annum after charges, fund runs out after approximately 30 years