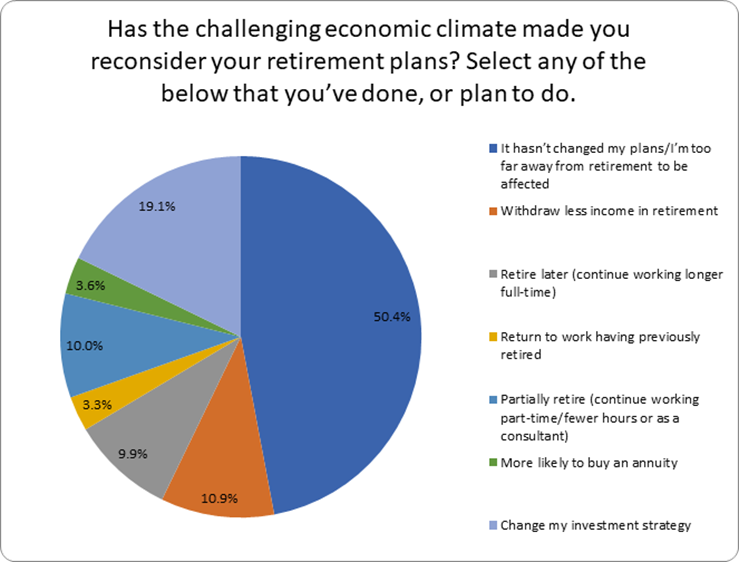

- Half of retirement investors have rethought their retirement plans or strategy in response to the challenging economic climate, AJ Bell customer research shows

- Almost 1-in-5 (19.1%) have switched investment strategy during this period of economic and market turbulence, while over 1-in-10 (10.9%) say they will draw less income in retirement

- For some, the cost-of-living crisis is forcing them to rethink plans to stop working:

- 1-in-10 (10%) say they will now work part-time in retirement

- Approaching 1-in-10 (9.9%) say they will now retire later than planned

- A smaller proportion (3.3%) say they will return to work having previously retired

- Despite rates improving significantly over the past year, just 3.6% say this has spurred them to buy an annuity in retirement

Tom Selby, head of retirement policy at AJ Bell, comments:

“In light of the severity of the cost-of-living crisis and the turbulence we have seen in both markets and the economy, millions of people are being forced to rethink their retirement plans. The approaches people are taking will vary depending on their personal circumstances, including how old they are and whether they are saving for retirement or drawing an income.

“Almost a fifth (19.1%) of retirement investors say they have switched their investment strategy in response to economic uncertainty. It is important anyone considering doing this has a firm focus on their long-term retirement goals, rather than attempting to time markets, taking risks they aren’t comfortable with or panicking because their portfolio has taken a short-term hit.

“For anyone investing over a time horizon spanning decades, the current bout of inflation, while painful, shouldn’t necessarily force a change in approach. Indeed, the danger in shifting your investments based on relatively short-term factors is you drift away from your long-term strategy and end up paying unnecessary trading costs to boot.

“The fact half of people are not changing their retirement plans at all should not be viewed as concerning as, in many cases, doing nothing will be the best approach. However, it is also important not to stick your head in the sand and keep an eye on your retirement pot, particularly if you are in the early years of taking an income through drawdown.”

Source: AJ Bell customer survey 2022.

Scaling back retirement plans

“For those who have already retired or are approaching retirement, economic turbulence is already forcing many to reconsider how and when they stop working.

“Some 10% say they will now work part-time in retirement to enjoy the lifestyle they want, while roughly the same proportion (9.9%) say they will now retire later than planned.

“A smaller number (3.3%) plan to return to work having previously retired, something the government is keen to encourage to fill vacancies in the labour market, while 1-in-10 say they will draw less income in retirement.

“All of these approaches should help ensure withdrawal plans are more likely to be sustainable over the long-term. While for some these decisions will be painful – particularly when it comes to pushing back retirement and working for longer – it is encouraging so many people are being clear-eyed in their approach to generating an income in their later years.

“Interestingly, a relatively small proportion (3.6%) say they now plan to buy an annuity, despite a substantial improvement in rates over the last year. The rise in annuity rates means in many cases, a combination of annuity and drawdown will likely provide the right solution in retirement.”

Sustainability is the key

“The longer the cost-of-living crisis drags on, the more the issue of sustainability will be driven up the agenda as people are forced to turn to their retirement pots to maintain their standard of living.

“For those who have stopped working, that might mean increasing withdrawals in line with inflation. Given inflation is currently running at double digits, this creates a real risk to the sustainability of withdrawals, particularly where large withdrawals are coupled with falling markets.

“Among those aged 55 or over who are still working, we will inevitably see more people turning to their retirement pot earlier than planned, either to cover their own increased living costs or help a loved one facing financial difficulty.

“The most recent data from HMRC suggests this was already happening in 2022, with a staggering £3.6 billion of flexible pension withdrawals made between 1 April and 30 June 2022 – a 23% increase compared to the same period in 2021.”

For many, 2023 will be when the financial pain strikes

“But for many people – and particularly those with mortgages – it will be 2023 when rising costs really start to bite. For those accessing their pension earlier than planned as a result, this could have consequences for their longer-term retirement plans in two ways.

“First, and most obvious, they will deplete their pension pot and so have less to turn into a retirement income when they do exit the workforce.

“Second, if they access taxable income flexibly from their pension pot, their ability to rebuild their fund will be constrained by the money purchase annual allowance (MPAA), which reduces the annual allowance from £40,000 to £4,000 and removes the ability to carry forward any unused allowance from the previous three tax years.

“One way to avoid triggering the MPAA is to just take your tax-free cash, but some will need more than their tax-free cash while others will be unaware that taking taxable income will reduce their available annual allowance.

“Given the immediate financial challenges facing millions of people, the government should review the level of the MPAA as a matter of urgency.”