By Chris Iggo, Chief Investment Officer, Core Investments, AXA Investments Managers

Key points

- Peak interest rates support fixed income

- Capital gains hard to come by

- Bonds provide improved income returns

- Equities at risk from recession

- Earnings forecasts are likely to be cut further

- Some scope for sector rotation

- Much will depend on energy prices

Contrasting returns

There were few places to hide in 2022. Inflation, monetary policy tightening and geopolitical risks marked a stark contrast to the drivers of returns in 2020 and 2021; the backdrop ultimately forced a revaluation of fixed income and equity assets. From low to high inflation, and from low to high interest rates, returns suffered as markets adjusted to the new paradigm.

However, as 2022 came to a close, markets found a more stable footing. Fourth quarter (Q4) returns were significantly better than what had gone before, even if the outlook was clouded – as it still is. Inflation is high and is only just showing signs of moderating. Central banks are not likely to stop raising rates until well into the new year. More importantly, we expect recession on both sides of the Atlantic.

The modest recovery in asset prices towards the end of 2022 should not, in our view, be seen as a step towards revisiting the valuation peaks of recent years. Equity price-earnings ratios are likely to remain below their highs and bond yields are not going back to close to zero. The kind of capital returns that investors enjoyed in the quantitative easing era are unlikely to be repeated any time soon. The current environment requires more thoughtful investment strategies than just chasing earnings growth and higher yield, irrespective of valuations or credit risk.

The inflation advantage

In a recession, cash flow from corporate assets to investors becomes challenged. Earnings growth slows as costs rise and revenues come under pressure. In credit markets, scarcer cash flows mean understanding how borrowers manage their debt liabilities is key. It seems in the early part of 2023, with macroeconomic uncertainty still running relatively high, investors are likely to retain a level of defensiveness. Volatility and ongoing periods of losses should not be ruled out.

Improved trade-off

Fixed income investors, however, stand to benefit most from the peak in inflation and policy rates. For bond markets, the trade-off between return and risk has improved. Yields are higher – compared to the situation in recent years – and this provides more ‘carry’ for bond holders and better income opportunities for new fixed income investments. At the same time, with higher yields, fixed income has the potential to play a more significant role in multi-asset portfolios. In 2022, very unusually, both bond and equity returns were very negative. Thankfully, central banks don’t raise rates by 300-500 basis points every year. As such, we don’t expect a repeat in 2023. If equities struggle with the growth environment, bonds can provide a hedge and an alternative to those investors putting a premium on income.

Supporting duration

Higher rates dominated 2022 and their impact on valuations has been clear. When and if growth slows, central banks will stop raising rates, as long as inflation is easing back. This is already priced in to yield curves with markets anticipating peak rates in the US in Q2 and in the Eurozone in Q3. For now, it is an environment that supports exposure to the shorter maturity part of bond markets. Such strategies currently provide the highest yields seen for years. Extending duration along the curve also locks in better yield and provides optionality to recognise capital gains once markets start to anticipate central banks easing. Our base case is that this is unlikely until late 2023 or 2024, but markets tend to look forward to these events.

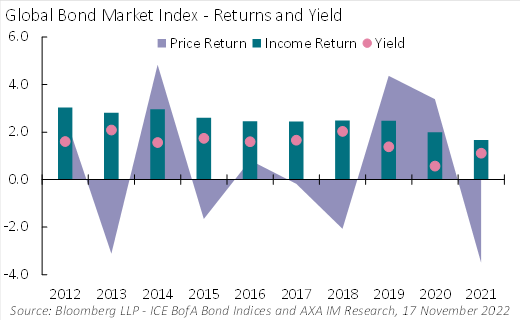

Income vs. total returns

The new regime for fixed income markets and related strategies is a more balanced one. In recent years, returns were dominated by capital gains as central banks pushed down yields. Income should now be a more significant contributor to total returns (Exhibit 1). This has portfolio construction implications with bonds now more suited to income-focused strategies as well as allowing institutional investors more flexibility in meeting liabilities without taking unnecessary credit or liquidity risks to achieve yield targets.

This focus on income, with more modest capital gain potential, supports corporate bond markets. However, borrowers will be challenged and this could impact on the level of credit spreads. Rates have done a lot of the work in pushing up corporate borrowing costs. Spreads have also widened but remain below the highs seen in previous periods of stress. This means that for similar credit ratings, today’s yields are significantly higher than in recent years. This provides attractive return potential as corporates have generally managed balance sheets well, terming out debt, containing leverage levels and ensuring healthy interest coverage. Over the medium term, today’s spreads will allow investors to benefit from capital gains when corporate fundamentals do improve.

Exhibit 1: Income to dominate bond returns

High time for high yield?

Core credit investment strategies can achieve higher yields with less credit risk. Subsequently investors need not chase returns in more economically-sensitive sectors when more defensive credit sectors offer attractive yields. However, we also see a role for high yield credit. Yields have been at levels in 2022 that historically have been associated with subsequent positive returns. High yield markets are of better credit quality in general than in the past and have seen similar improvements in credit metrics as the investment grade market. Of course, defaults will rise a little but we have little concern about a large wave of refinancing-related defaults. Given the close relationship between the excess returns of high yield bonds (relative to government bonds) and equity returns, we see high yield as a relatively lower risk option on an eventual recovery in equity returns.

Chasing income

Higher yields can be achieved with less duration and credit risk than in recent years. That is useful in this kind of economic environment. A significant improvement in risk-adjusted performance for more challenged parts of the fixed income market, like emerging market debt, may have to wait until the overall outlook and risk sentiment is significantly improved. An end to the Ukraine war and a recovery in the Chinese property market would be welcome developments for emerging market debt.

The Q4 equity market rally was chiefly driven by expectations of peak inflation and rates but it needs to be judged against a deteriorating earnings outlook and in an environment where interest rates are going to be higher than they have been for years. These will remain headwinds for stocks for some time. Even after the significant de-rating already seen, stock markets are still vulnerable to the expected earnings recession.

A balanced outlook

There is the potential for some sector and style rotation going forward. Energy stocks have outperformed on the back of high oil and gas prices. Historically, however, energy sector earnings are more cyclical and with lower long-term growth potential than the more dynamic new economy sectors which have been most impacted by the market de-rating.

The long-term outlook for traditional energy companies is challenged by the momentum of the energy transition. Sure, prices may remain high but this is not guaranteed if growth undercuts energy demand or if there are new developments on the supply side (an end to the war in Ukraine; a return of Iran to global oil markets). At the same time, a new corporate investment cycle will eventually benefit technology and automation while government policies are more focused on energy efficiency and healthcare.

It is not unheard of to have consecutive years of negative equity returns. However, I believe the outlook is more balanced; earnings are under pressure but valuations more attractive. Outside of the US, markets have seen significant declines in price-earnings multiples. European markets, for example, would be well placed to rally should there be positive developments in Ukraine. Asia will benefit from a post-‘Zero-COVID’ recovery in China. Long term, however, the US valuation premium is not likely to be challenged given the dominance of US technology, a greater level of energy security and more positive demographics. In the near term though, some highly-priced parts of the US market remain vulnerable.

Global tightening forced a revaluation across asset classes. Cash flow expectations have been challenged and investors should be less confident about capital growth strategies as we enter 2023. Bond returns should improve relative to volatility and parts of the equity market are becoming cheap. As 2023 unfolds, there should be more clarity on the macro outlook. This should support positive, albeit prudent, portfolio return expectations.

To consult the full Outlook 2023 report, please click here.