Naomi Fink, chief global strategist at Amova Asset Management, assesses Japan’s weaker-than-expected fourth-quarter GDP growth of 0.1% as masking firmer inflation dynamics, with a 3.4% rise in the GDP deflator highlighting price pressures, while wages, the yen and the fiscal-monetary policy mix remain central to the outlook.

On the surface, Q4 2025 GDP provided broad disappointments, expanding only 0.1% q/q in real terms, and 0.6% in nominal terms (vs 1% expected). Capex also crept higher by 0.2% versus 0.6% expected, which was a disappointment though not a reversal of the expansionary backdrop, driven by corporate pricing power and reflationary wage-price dynamics. Inventories reduced by more than expected (-0.2%), providing a small incremental drag, and net exports also delivered a small negative surprise (0% q/q). A great focal point however was the GDP deflator, which was up 3.4% y/y vs 3.2% expected, underscoring the contribution of inflation rather than stagnant demand to the gap between nominal and real growth.

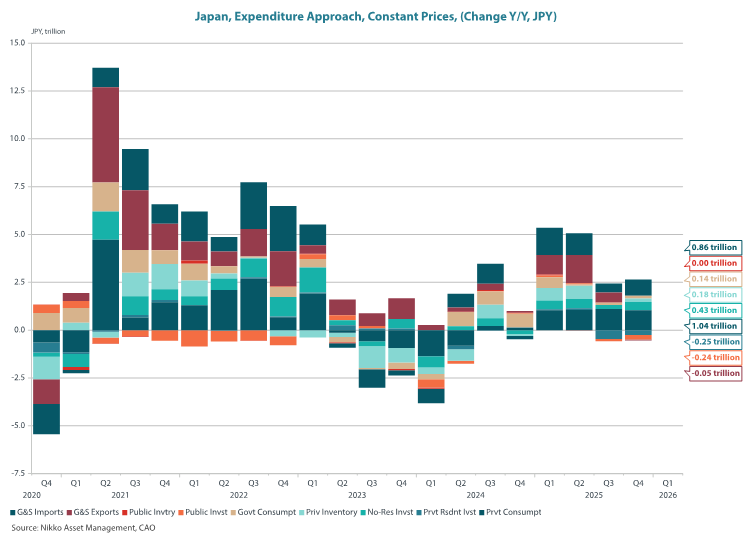

Some of the q/q estimates owed to a revision in Q3 data, and by seasonally adjusted standard, quarterly data in 2025 showed greater swings than usual. It is therefore useful to look at both full-year data as well as y/y data, to smooth out the technical fluctuations.

From a full-year perspective, Japan has delivered resilience in a year of significant uncertainty; it’s full-year 2025 real GDP growth estimates are well above potential, at 1.1% (BOJ estimates potential to be near 0.4%), with private demand recovering to expand 1.6% over the year, following negative readings in both 2024 and 2023. A big part of this was domestic consumption and private non-residential investment, all growing well above 1% over the full year. The problem remains that even these healthy above-potential results pale in comparison to nominal growth of over 4% y/y in the above-mentioned sub-components, underscoring that despite the household’s potential to engage in greater consumption, much of this potential is being eaten up by price rises. Meanwhile, a weak yen is weighing on terms of trade, which reduces Japan’s real purchasing power. Despite ongoing growth in the volume and value of exports over the full year (+0.6% y/y in real terms, +0.7% in nominal terms), the rising value of imports has constrained Japan’s global purchasing power. We may also see many of these dynamics play out in y/y data (see below chart, which shows y/y real GDP growth in JPY terms).

What matters going forward? Wages, inflation, the yen

First and foremost, the Bank of Japan has highlighted why we should pay greater attention to wage-price dynamics as a forward-looking indicator of Japan’s reflationary potential. Firstly, for households, real balances matter and for households, this means whether wages are growing more quickly than the prices of goods and services in their consumption basket. There are also second-order effects of wage-price dynamics on production capacity – it is possible that many quarters of labor supply shortages (which, in the Bank of Japan’s terms, are now “chronic”) have weighed upon Japan’s capacity to effectively utilize its physical capital before it is fully depreciated. If indeed a driving factor of Japan’s utilization of physical capital, increasing human capital would be paramount to maintaining the momentum of Japan’s reflationary dynamics. Announcements surrounding the “shunto” spring wage round and also the continued investment of firms into labor-saving dynamics should be closely watched going forward, as well as factors of labor supply growth in Japan, such as immigration.

The Fiscal-Monetary policy mix: Complementary is optimal

Whether inflation is demand-pull (wage-driven) or cost-push (influenced by price rises, foreign exchange and terms of trade) remains a complex question, and it is not as simple as contrasting household real vs. nominal consumption to resolve this question. The firm GDP deflator clearly shows that prices are driving a wedge between the volume and value of consumption. The weak yen is a contributing factor to the terms of trade drag. Insofar as interest rates in Japan remain far below those of its developed economy counterparts despite experiencing similar rates of inflation, the relatively cheaper yen has facilitated the financing of risk investments across the globe (as may be seen in MOF portfolio flow data). These flows may have contributed to the yen’s chronic weakness, which all else equal may increase pressure on the Bank of Japan to prioritize normalization of interest rates in the interest of calming imported inflation.

Meanwhile, although expectations for significant fiscal stimulus have accompanied PM Takaichi’s special election victory, the more meaningful contribution of this increase in political support may be the ability to stand back and allow the independent Bank of Japan to fight inflation while itself making greater commitments to long-term fiscal sustainability, which the government can now afford to do.