George Lagarias, chief economist at Mazars, comments on inflation, demand and supply chain.

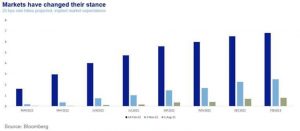

“Last week saw the US registering the highest headline inflation number in over 40 years, 7.5%. Equity and bond markets roiled, with the US 10-year Treasury yield rising above 2% and the S&P 500 shedding nearly 2% for the week. Currently, markets are pricing in nearly more than six rate hikes by the end of the year instead of less than two, three months ago. To be sure, the Fed’s communications have been much more reserved, with even the most hawkish officials expecting four to five hikes during the year.

“Is the market overreacting, or is the Fed so far behind the curve? The truth is, no one knows at this point. No one is an expert on inflation, and certainly not the kind of inflation we are currently experiencing.

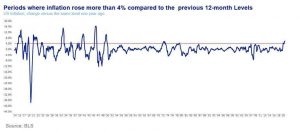

“For a generation that has only experienced the benefits of globalisation, inflation is a riddle, wrapped in a mystery, inside an enigma. Twenty-two years of falling prices, twelve of which saw muted consumer demand and preference for saving overspending had ostensibly consigned inflation to history.

“In fact, “history” is the operative word. The swift rise in inflation we are seeing today can only be found near, or around very significant historical events. For inflation to rise over 4% in a single year and stay high for more than 3-4 consecutive months, one would have to travel back fifty years to 1973.

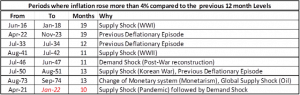

“The great Milton Friedman, the first major economist of the Monetary Era suggested that “inflation always and everywhere is a monetary phenomenon”. This would imply that interest rates would be the most appropriate tool to fight it. However, and with respect to the Nobel Laureate, this aphorism, which seems to be anchored in many investors’ and central banker’s thinking, is probably wrong.

“If we take US numbers, the first major inflation surge of the century came in 1916. This was the year when America got involved in the First World War. Supply shocks from a devastated European continent drove inflation higher. The next episode took place in 1922. After another collapse in supply, Europe was in disarray, and it followed a massive deflationary episode. Similarly, inflation in 1933-34 came after a significant deflationary episode, following the Great Depression. Inflation in 1941-1942 was again about the US entering a World War, and in 1946 it was about consumer and industrial demand after the European reconstruction was underway. In 1950, the Korean war and a prior deflationary episode drove an inflation surge. In 1973, the Yom Kippur war, coupled with a change in the global economic system from the Gold Standard to Monetarism, fuelled another inflationary episode. Independent central banks and the fall of the Iron Curtain as well as a new status quo in the Middle East, brought nearly unprecedented peace, the “Pax Americana”. With it, a modicum of macroeconomic stability.

![[UNS] celebrate](https://ifamagazine.com/wp-content/uploads/2024/11/jason-leung-Xaanw0s0pMk-unsplash.webp)