- A proposed overhaul of projections rules used to show investors what income their pension pot might deliver when they retire risk undermining Pensions Dashboards reforms

- Under plans outlined by the Financial Reporting Council (FRC), the projected growth of someone’s pension (or pensions) would be based on the volatility of their investments (see end of press release for details of the proposals)

- The plans, designed to support the rollout of Pensions Dashboards, will at best be of no benefit to savers and at worst could leave people bewildered when they engage with Dashboards

- Projections need to be as simple as possible for consumers to understand

- Deadline for responses to the FRC consultation paper is today

Tom Selby (pictured), head of retirement policy at AJ Bell, comments:

“Pensions Dashboards have the potential to fundamentally improve the UK’s retirement landscape, helping connect savers with lost pots and, over time, better engage with their financial future.

“However, the project risks getting unnecessarily tied up in knots over plans to reform growth projections which few people pay attention to and, invariably, will end up being wrong.

“The thinking behind the FRC’s plans to base projections on the volatility of someone’s underlying investments is to build consistency into the system.

“In striving for this aim, they risk delivering an unwanted hat-trick of bringing in changes that will be of zero benefit to savers, layer complexity into an already complex system and become a costly nightmare to administer.”

Perverse outcomes

“The plans also risk creating perverse outcomes. For example, someone with their entire portfolio invested in one highly concentrated, high-risk (and therefore volatile) fund would likely be projected a higher return than someone with a well-balanced, diversified portfolio.

“This feels like an odd message to be pushing to savers, many of whom presumably will be engaging with their pensions for the first time.

“What’s more, the FRC’s approach, if adopted, will mean savers viewing two different pensions via Dashboards could potentially see two different growth rates. This will inevitably create confusion, particularly among those who are relatively new to saving and investing.”

If in doubt, keep it simple

“The FRC needs to go back to the drawing board and devise a simpler solution. For example, a single growth rate could be adopted, with clear signposting that this is for guidance only and lower-risk investments might have lower expected returns.

“We also need consistency between FCA point-of-sale disclosures and Statutory Money Purchase illustrations (SMPIs) – something that is lacking at the moment.

“For example, FCA rules require 2% inflation to be factored into point-of-sale disclosures, while for SMPIs the figure is 2.5%. This is patently non-sensical and needs to be addressed as part of a review of disclosure rules.

“There is no reason why the two sets of disclosure requirements should be different. This might not have been a major problem in a world where most people don’t engage with these statements, but if Dashboards are to be a gamechanger, policymakers need to make sure what they see is consistent.”

Background – what are the FRC proposing and why are they doing it?

The projections issue first surfaced when the Government made clear it wanted Pensions Dashboards not just to display the values of people’s pensions, but to project that pot to their retirement date and convert it into an ‘Estimated Retirement Income’ (ERI). These figures are available from Statutory Money Purchase Illustrations (SMPIs).

The Occupational and Personal Pension Schemes (Disclosure of Information) Regulations 2013 govern SMPIs, with guidance on how to produce them provided on a statutory basis by the Financial Reporting Council (FRC).

Under current rules providers have flexibility to set their own SMPI growth rate – it just needs to be “justifiable” and take account of charges and inflation at 2.5%. This has the advantage of being relatively simple but also means different providers will produce different SMPI growth rates.

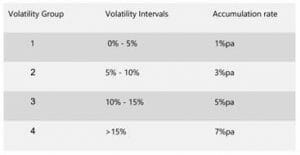

Because of concerns the lack of consistency of this approach risks undermining trust in Dashboards, the FRC now wants to mandate growth rates used by providers, using volatility to determine the rate.

The proposed rates are set out below, with investments placed in a volatility group based on their volatility of monthly returns over a 5-year period.

![[UNS] celebrate](https://ifamagazine.com/wp-content/uploads/2024/11/jason-leung-Xaanw0s0pMk-unsplash.webp)