By Erik Esselink and James Matthews, Invesco European Equities Fund Managers.

We see three main reasons why the outlook for European smaller companies is favourable versus other regions. Firstly, we think growth rates in Europe will be strong for a few years to come. Secondly, we think valuations are reasonable and, lastly, Europe has a number of big themes that will attract investment flows. We have seen a remarkable first half of the year in European small caps in which they have generated higher returns for our shareholders in six months than we usually see in a full year.

These returns come on top of a strong recovery in markets last year from the March 2020 lows. We tend to refrain from commenting on the overall market and whether our funds will go up or down over the next few months as our goals are to generate long-term capital growth. We do, however, have strong views on the stocks we own and how attractive they are as investments today, where we see value emerging and which parts of small- and mid-cap markets we are getting more cautious on.

1. European growth rates remain strong

In western Europe vaccination rates are high and hospitalisation rates have come down sharply. Furthermore, large portions of the population have tested positive for Covid at some point over the last year, which should lead to smaller and smaller spikes of outbreaks going forward. The European consumer meanwhile is in a very strong position. Low unemployment means spending power is high but, added to that, the saving rate has ballooned over the pandemic as consumers were not spending money on travel and leisure activities.

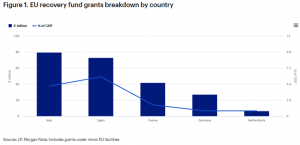

The European stimulus program still has to kick in and should provide a big tail wind, especially for Southern European countries and companies. This stimulus should be seen in the context of a region that, over the last decade, managed to only show marginal GDP growth. This makes the incremental change here very significant in our view.

2. Based on 2023 estimates European small caps look attractively valued

In the early stage of a recovery, the valuation of individual securities is always a tricky concept. As the earnings and revenues of the companies have gotten a beating, it makes little sense to value companies based on current earnings. Our favoured method was to estimate new mid-cycle earnings and value securities based on those numbers.

As the recovery progresses, we enter the growth phase, typically the multiple that the market trades on contracts but the earnings upgrades are offsetting this and driving the market higher.

Obviously, not every stock or sector gets equal earnings upgrades. Cyclical areas of the market tend to get significantly more earnings upgrades than the less economically sensitive sectors.

In this phase, we focus a lot of our analysis on the ‘earnings over-delivery’ that we expect from the companies we invest in. We believe European small caps are attractively valued based on 2023 estimates (mid-cycle) and have focused the portfolios on companies that can over deliver on the current expectation in the market.