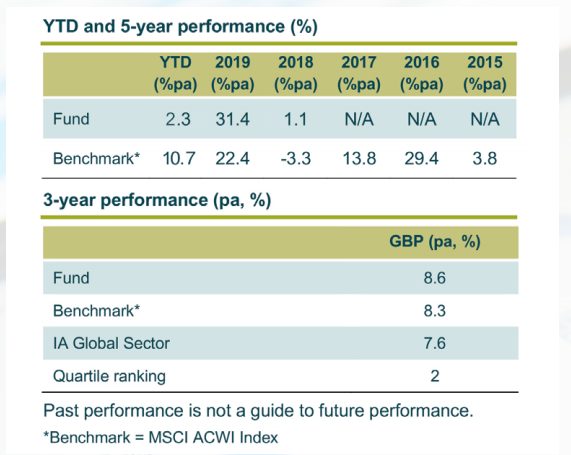

Three-year performance

In the three years since the fund’s launch in October 2017, the M&G Global Listed Infrastructure Fund outperformed the MSCI ACWI Index with an annualised total return of 8.6% (GBP I Acc shares). Each segment of the portfolio – ‘economic’, ‘social’ and ‘evolving’ infrastructure – made a positive contribution to performance.

The fund also delivered on its income objective by increasing the distribution by 6.5% for the financial year ended 31 March 2020 (GBP I Inc shares).

The benchmark is a target which the fund seeks to outperform. The index has been chosen as the fund’s benchmark as it best reflects the scope of the fund’s investment policy. The benchmark is used solely to measure the fund’s performance and does not constrain the fund’s portfolio construction.

The fund is actively managed. The fund manager has complete freedom in choosing which investments to buy, hold and sell in the fund. The fund’s holdings may deviate significantly from the benchmark’s constituents.

Source: Morningstar, Inc., as at 30 November 2020, GBP Class I Acc shares, income reinvested, price-to-price basis. Benchmark returns stated in share class currency.

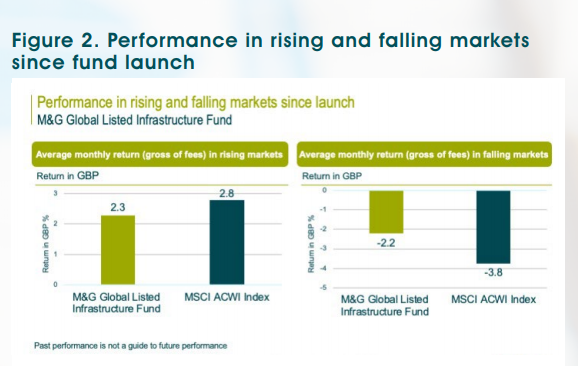

Upside capture, downside protection

The fund experienced a variety of market conditions during its first three years, but the outperformance was driven by a recurring pattern: capturing most of the upside during market rallies and providing downside protection when markets fell (see Figure 2). The upside capture was a direct consequence of the fund’s resolute focus on growth, while the downside protection was a reflection of the defensive qualities of listed infrastructure as an asset class.

The fund delivered a positive return in 2018 when equity markets fell, and outperformed its benchmark, the MSCI.

Source: M&G, Aladdin, 30 September 2020. Investment return (gross of fees) calculated in sterling. Fund was launched on 5 October 2017. Investment returns are shown to eliminate timing issues between the pricing of the fund (product return net of fees), which is calculated at midday in London, and the close-of-trading day pricing of the index. Past performance is not a guide to future performance.

ACWI Index in 2019 as the markets rallied, but has faced more challenging times so far in 2020 against a difficult backdrop for listed infrastructure strategies.

This year’s performance has been influenced by events in March when the weakness in energy infrastructure and transport weighed on returns, and the period from June onwards when ‘new economy’ stocks dominated proceedings and propelled equity markets to all-time highs.

Covid-19

The exogenous event of a global pandemic was an exceptional circumstance which had unique consequences for listed infrastructure. Energy infrastructure came under severe pressure in March as pipeline stocks became embroiled in a broader sector malaise, thwarted by the dual shock of increased supply from Saudi Arabia and lower global demand in the wake of COVID-19. The cashflows generated by energy infrastructure businesses have different characteristics to those of oil & gas producers; they have limited direct exposure to the underlying commodity price, although fundamentals gave way to sentiment in an environment of extreme uncertainty. Transportation infrastructure, in particular airports, was another area under pressure as the world entered lockdown. In contrast to previous recessions when traffic volumes slowed, the enforcement of ‘stay-at-home’ policies saw international travel come to an abrupt halt.

Despite the challenges in the short term, we continue to have a positive view and we believe our long-term perspective has already worked in the fund’s favour. Energy infrastructure and transport, which led the detractors in March, were strong in the rebound in April and May. Our decision to add to selected holdings during the market downturn was swiftly rewarded.

There is scope for further upside, in our view. A phased reopening of economies, or a successful vaccine, for instance, could lead to a significant reassessment of these businesses as investors contemplate a world returning to normal. The fund’s look-through exposure to airports is currently limited to about 5%.

Narrowness of market leadership

In contrast to the one-off nature of the global health crisis, the narrowness of market leadership, which was apparent from June onwards, provided a more familiar headwind for listed infrastructure. The technology-led rally in January 2018 was another example when the reliable growth from listed infrastructure was largely ignored as investors chased the momentum behind ‘new economy’ stocks.

This time round, Apple and Amazon.com stood out as the beneficiaries of the market’s scramble for growth, which gathered pace with little heed for value. These paragons of the modern world are simply not infrastructure businesses and are therefore ineligible for our strategy, although their explosive growth is reflected in our digital infrastructure exposures. Many of the market’s tech leaders are important and growing tenants of our data centre holdings, for example.

We continue to believe that listed infrastructure provides attractive opportunities for long-term growth from a variety of sources, without being hostage to the market’s fickleness and its bouts of excessive euphoria. ‘New economy’ stocks made a hasty retreat from their peaks in September.

Continue reading article…