Portfolio activity

The fund is usually managed as a low turnover, buy-and-hold strategy. There were just five new purchases and six complete sales during the first two years of the fund’s history. One of the sales, John Laing Infrastructure Fund, was driven by a takeover approach. However, the indiscriminate selling in March triggered by the onset of COVID-19 created buying opportunities, in our view, for long-life infrastructure assets which are critical for the smooth functioning of modern society, while delivering reliable revenue and cashflow growth. Valuation is a key consideration in our stock selection process. We were therefore more active than usual during the period of market volatility to take advantage of what we considered attractive entry points.

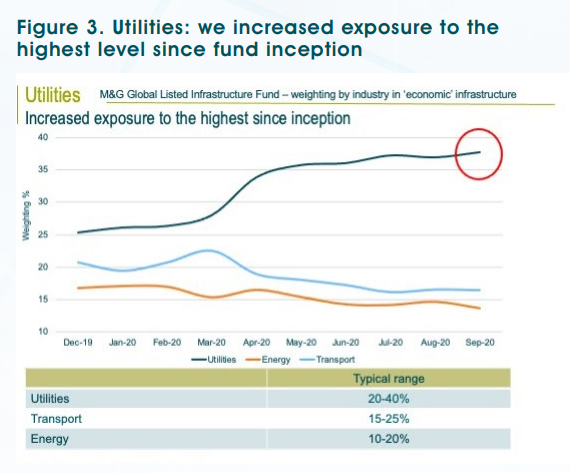

We capitalised on what we considered to be relative value opportunities in utilities, which proved distinctively resilient during the global health crisis. We see the sector acting as a bastion of strength against the backdrop of ongoing economic uncertainty.

We initiated six new positions in utilities since March. We have been tracking these companies for many years, but the valuations were out of reach until the recent market downturn presented the buying opportunity we were waiting for.

The new purchases were selected from around the world, and for us, each one has its own growth story. In the US, NextEra Energy Partners is a pure play on the structural growth in renewable energy, while Sempra Energy and AES Corp provide a different dynamic. Sempra diversifies the exposure we already have to California and Texas by way of our existing holdings in Edison International and Atmos Energy, with the addition of potential growth avenues in the key transition fuel of liquefied natural gas (LNG), as well as emerging markets through its presence in Mexico. AES Corp’s long-term growth is driven by its transition to renewables and battery storage, in addition to its emerging market exposure and the transformation of its asset portfolio by way of an aggressive phase-out of coal.

A2A, the Italian multi-utility, also combines growth in renewables with a rapid decarbonisation programme. ContourGlobal is listed in the UK but has a broad geographic footprint with exposure to growth in emerging markets as well as the trend towards sustainable energy sources. China Gas Holdings is another beneficiary of structural growth as China reduces its reliance on coal and shifts its source of power and heat generation to gas. This critical aspect of the energy transition is a multi-decade trend, in our view. We bought the Hong Kong-listed shares.

Following these transactions, the fund’s utilities weighting rose to the highest since inception at 38% (see Figure 3).

The exposure to energy infrastructure and transport was trimmed back after our holdings recovered strongly in the early stages of the market rebound. The weightings in communications and social infrastructure were also reduced, having performed well across the market’s ups and downs. The fund can be exposed to different currencies. Movements in currency exchange rates may adversely affect the value of your investment.

Investing in emerging markets involves a greater risk of loss due to greater political, tax, economic, foreign exchange, liquidity and regulatory risks, among other factors. There may be difficulties in buying, selling, safekeeping or valuing investments in such countries.

Dividends

COVID-19 and its knock-on effect on the global economy have had a profound effect on corporate cashflows and dividends. We therefore took decisive action and made efforts to strengthen the fund’s income stream, with the new utilities holdings providing the necessary ballast. NextEra Energy Partners and China Gas Holdings have already made their mark with double-digit dividend increases. We view the utilities sector as having the most reliable revenue and cashflow prospects in the current environment.

Despite the need for caution in certain industries, dividends from listed infrastructure companies have been highly resilient. Many of the fund’s holdings have continued to pay and increase their dividends since March as a reflection of their cash-generative qualities and their confidence in long term growth potential. The fund benefited from dividend increases across the spectrum of listed infrastructure as well as a broad range of countries.

In ‘economic’ infrastructure, utilities companies demonstrated the resilient nature of their business models, with our holdings continuing to deliver more impressive dividend growth than the pedestrian progress more commonly associated with the sector. American Water Works raised its dividend by 10%, in line with the last two years. Republic Services, the US leader in recycling and waste management, reported a 5% increase. Energy infrastructure was another source of reliable dividends as our holdings continued to pay dividends at prior levels. Union Pacific, the US railroads company, maintained its dividend in transportation infrastructure.

‘Social’ infrastructure also proved dependable as a source of steady growth. International Public Partnerships (INPP) and HICL Infrastructure announced dividend increases which were broadly in line with inflation, as expected. SDCL Energy Efficiency Trust remains on track to grow the dividend by 10% in the current financial year.

‘Evolving’ infrastructure provided a more exciting source of growth, with American Tower being the standout. The owner and operator of communication towers has raised its dividend every quarter this year with an annualised growth rate of 20%. Industry peer Crown Castle increased its dividend by 11%.

The fund was not immune to dividend cuts, however, particularly in airports where the operating environment has been extremely challenging. Dividends from airport companies are under pressure in the short term, and our pure airport plays, Sydney Airport and Flughafen Zurich, have temporarily suspended their payments. Vinci and Ferrovial also have airports businesses, and Vinci has cut its dividend. It would be reasonable to expect Ferrovial to follow suit.

We continue to have conviction in the long-term prospects of these companies as owners and operators of strategic assets and have no intention of selling out of these holdings on a tactical basis. We have faith in their commitment to reinstate dividends and resume dividend growth at the appropriate time. In these unprecedented times, we remain supportive as long-term shareholders.

While a dividend cut should never be taken lightly, these disappointments were outliers in a 47-stock portfolio. The majority of holdings continued to deliver stable or rising dividends in an extreme environment, as a result of which the fund delivered on its objective of growing the income stream during the first six months of the current financial year ending 31 March 2021. The distribution for the first two fiscal quarters rose 27% compared to last year (GBP I Inc shares) (see Figure 4).

We would be wary of extrapolating this growth rate for the remainder of the year, but we remain confident that the vast majority of our holdings can keep growing their dividends in the core 5-10% range. The fund remains on track to deliver on its objective of providing a rising income stream for the full year.

The fund holds a small number of investments, and therefore a fall in the value of a single investment may have a greater impact than if it held a larger number of investments.

Continue reading article…