ESG integration

The analysis of environmental, social and governance (ESG) issues has been an integral part of the investment process since inception of the fund because there are risks and considerations associated with listed infrastructure that are unique to the asset class. We are investing in companies with physical assets which are by their very nature immovable and have an impact on a variety of stakeholders including employees, customers, shareholders and wider society. Our ESG process is designed to assess the sustainability of assets and thereby ensure that the cashflows generated by the infrastructure businesses in which we are investing are sustainable and have the potential to grow over the long term. We need to make sure that our favoured businesses do not face ‘stranded asset’ risk or lose their social licence to operate.

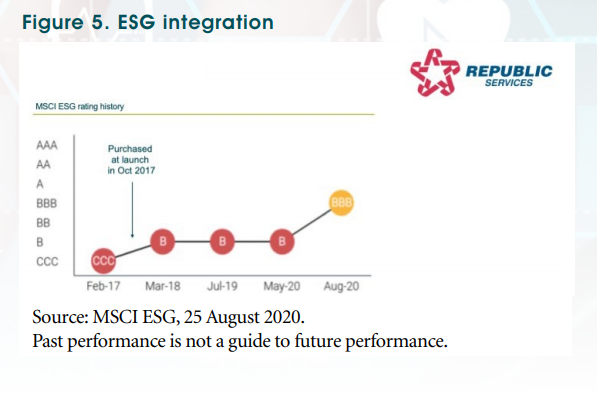

Proprietary research is central to our ESG analysis. We do not subscribe to the blind acceptance of third-party rankings or the mechanical exclusion of poorly rated companies. Take Republic Services, for example. The US leader in recycling and waste management provides essential services for society, but its landfill assets and associated greenhouse gas (GHG) emissions were given what we considered to be simplistic treatment by third-party ESG ratings providers. Prior to the fund’s launch in October 2017, Republic Services was rated CCC by MSCI ESG. For us, the low rating was not a sufficient reason to dismiss the company as a potential investment candidate; it merely prompted us to conduct our own due diligence and engage the company on ESG issues.

Following a series of ESG-focused meetings with the company in conjunction with M&G’s Corporate Finance and Stewardship team, we gained comfort that the company is being managed in a responsible manner: Republic Services has adopted pioneering technologies to reduce by-products and increase the recycling of landfill gas wherever and as much as possible. We invested in the company at the fund’s launch and the investment has made a positive contribution: the dividend has increased every year in the 5-10% range and the share price has climbed 30%. We are pleased that we did not miss out because of a poor third-party ESG rating at the outset.

The company’s progress is also reflected in ESG ratings. MSCI ESG has upgraded Republic Services on two occasions in the past three years in recognition of the significant improvement in its GHG profile (see Figure 5). The company’s ESG journey does not end there. The promising direction of travel is also reflected in the company’s commitment to clearly defined sustainability goals. Having achieved its 2018 targets, Republic Services has embarked on a more ambitious strategy with seven sustainability goals aligned with the United Nations’ Sustainable Development Goals (SDGs), including the aggressive reduction of GHG emissions and a continued increase in recycling. The stock remains a core holding.

Outlook

Governments around the world have announced huge fiscal stimulus packages in response to the global pandemic, including higher spending on infrastructure, which may provide a favourable backdrop. Europe’s recovery plan has been notable, not only for its scale and ambition but also the prominence attached to its green agenda. ‘Next Generation EU’ has a clear policy of promoting renewable energy and clean transport, as well as the renovation and efficiency of buildings and infrastructure to support a more circular economy. Digital infrastructure is another area receiving more investment as Europe strives to improve connectivity in a digital age, with the rapid deployment of 5G networks high on the priority list. Companies exposed to these structural growth trends can prosper to the benefit of their stakeholders, which include employees, customers, shareholders and broader society.

Infrastructure investment has been a key feature of economic stimulus packages in Europe, China and Japan, but the major economy where this has been notably absent is the US – ironically, the country that probably needs it most.

The need to repair, modernise and expand America’s ailing infrastructure is one of the few areas of common ground between the Republicans and Democrats. The fact that Donald Trump was unable to implement a much needed infrastructure plan during his presidency provided much frustration for both sides of the political divide. That said, decisions on infrastructure spending in the US remain in the hands individual states for the most part, although federal initiatives in the form of state subsidies and tax incentives will be widely welcomed. A Biden victory, which looks all but certain at the time of writing, is also expected to add impetus to renewable energy deployments, given his upfront green agenda. His plan ‘to build a modern, sustainable infrastructure and an equitable clean energy future’ comes with two specific targets: net zero carbon emissions by 2050 and $2 trillion investment in infrastructure.

Our long-term approach to listed infrastructure is not reliant on fiscal expansion continuing or government initiatives having an immediate impact on economic growth, but we are also conscious that this type of dynamic can drive strong performance for the asset class.

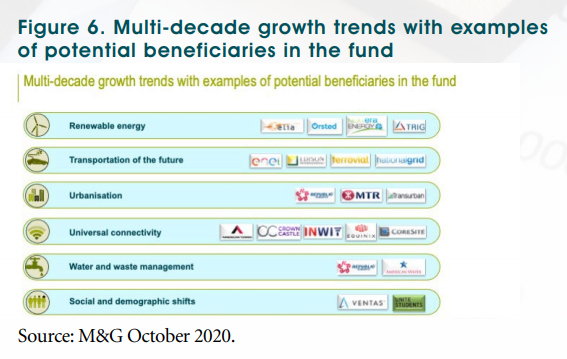

Fiscal stimulus is likely to remain a topical issue until the global economy is on a firmer footing, but it is also important not to lose sight of the fact that listed infrastructure is a beneficiary of powerful trends which we believe are likely to be more enduring. Thematic tailwinds such as renewable energy, clean transportation and digital connectivity are likely to persist for many decades to come, in our view (see Figure 6).

That said, we remain vigilant about the immediate outlook. We are acutely aware that growth is fragile in many parts of the global economy and therefore that dividends will continue to be tested. We cannot dismiss the potential for more dividend retrenchment as the year progresses. With this reality in mind, we believe that the fund is better placed after our efforts to strengthen the income stream with more reliable growth from selected utilities.

We continue to invest with a long-term view and remain confident that the portfolio is in good shape not only to weather the current uncertainty, but to capture attractive growth over the long term. Having passed the three-year milestone, we are even more excited about the next three years. We are optimistic as we have ever been about the long-term growth opportunities in listed infrastructure.

Click here for more information about the M&G Global Listed Infrastructure Fund