“The FTSE 100 is no higher now than it was in spring 2017, when Theresa May was Prime Minister and still trying to make the best of Brexit, but the index has not been the total duffer that many take it to have been, because it ranked third on the global stage in 2022, behind only India and Brazil,” says AJ Bell investment director Russ Mould.

“The FTSE 100 stands barely 5% below its all-time high and it is possible to make the case for the UK’s premier stock market benchmark setting new peaks in 2023, despite the doom and gloom which prevail in the wake of Trussonomics, a sequence of interest rate increases and Russia’s invasion of Ukraine.

“Take those into account and the FTSE 100’s performance looks quite resilient and, if anything, the best argument is favour of investing in UK equities is the air of pessimism which surrounds them.

| Index | Country | Capital return in 2022* |

| S&P BSE 100 | India | 7.0% |

| Bovespa | Brazil | 2.6% |

| FTSE 100 | UK | 0.6% |

| Nikkei 225 | Japan | (3.0%) |

| S&P / TSX | Canada | (5.8%) |

| Dow Jones Industrials | USA | (6.4%) |

| Euronext 100 | EU | (6.6%) |

| CAC-40 | France | (6.9%) |

| DAX | Germany | (9.7%) |

| Shanghai Composite | China | (12.7%) |

| SSMI | Switzerland | (14.1%) |

| Hang Seng | Hong Kong | (16.2%) |

| S&P 500 | USA | (16.3%) |

| FTSE All-World | Global | (17.2%) |

| FTSE 250 | UK | (20.0%) |

| NASDAQ Composite | USA | (28.8%) |

| FTSE AIM All-Share | UK | (31.7%) |

Source: Refinitiv data. *From 31 December 2020 to 12 December 2022, in local currency.

“No-one seems interested in the UK equity market, other than to bash it for failing to attract more new flotations and temporarily losing its status as Europe’s largest arena by market cap to France. Such knocking copy persists, even though analysts think the FTSE 100’s aggregate pre-tax income in 2023 will exceed that of 2017 by 71% and that dividend payments will set a new all-time high and come in 6% above 2017, when the index reached its closing high of 7,877.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts

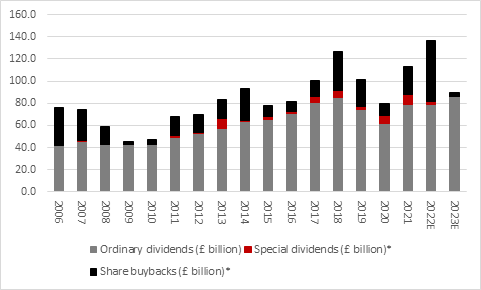

“Corporate confidence also seems high, judging by how the FTSE 100’s members have announced a record £55.2 billion in share buybacks in 2022, to add to £2.8 billion in special dividends already paid and analysts’ forecasts of £79.1 billion in dividend payments. Combined, that lot makes a cash yield on the FTSE 100 of 6.6% for 2022.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts

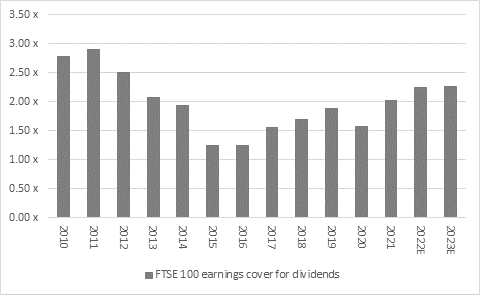

“Even if there is no guarantee of a repeat next year, dividend cover is at its highest point since 2012 and forecasts of a 4.1% dividend yield combined with a forward price/earnings ratio of barely 11 times may catch the eye of value-seekers.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts

“Any trader or investor will tell you that mood follows price and prices are not doing much right now. As a result, UK stocks feel unloved and unloved can mean cheap. And buying cheap is the best possible way of getting good long-term returns. As the old saying goes, ‘you can have good news and cheap stocks, just not both at the same time.’

“All other things being equal, even a 10-12% advance in the FTSE 100 to 8,250 would leave the index on a PE of 12 and a yield of 3.8%, neither of which looks demanding.

“That said, there are more than enough variables to make second-guessing the markets even harder than usual. Geopolitical tensions continue to bubble in Eastern Europe, the Middle East and Asia; inflation is yet to be tamed; central banks are still talking tough on monetary policy; forecasts of a long recession are everywhere; and the UK is still trying to make the most of Brexit and find some degree of political stability after a truly chaotic year.

“Markets continue to put their faith in central banks and their ability to rein in inflation, engineer a soft landing for the global economy and maintain financial market stability. Hopes for a slowdown, pause and then pivot in interest rate policy underpin the rally in stocks and bonds seen since early autumn, but there are inherent dangers in relying on the very same people who promised inflation would be transitory, especially as the cryptocurrency and liability-driven investing blow-ups, as well as bear market in US equities, also question the narrative of central bank omnipotence.

“If central bankers can be potentially wrong on, well, anything, then stock market strategists and asset allocators can be forgiven for hiding behind Lao Tzu’s assertion that: ‘Those who have knowledge don’t predict; those who predict, don’t have knowledge.’

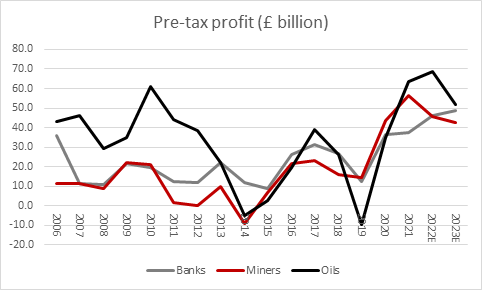

“It is also possible to argue that the UK stock market is cheap because it deserves to be, given the FTSE 100’s heavy weightings toward the unpredictable (oils and miners), the indigestible (banks and insurers) and the beyond-the-pale, at least so far as ESG screens are concerned (tobacco, oils, miners, bookmakers and defence stocks).

“Yet the valuation is tempting and certain sectors – banks, miners, housebuilders – already look to be pricing in a downturn in earnings and a recession, looking at their valuations and analysts’ predictions for the trajectory of their earnings. Yes, aggregate earnings forecasts for earnings and dividends in 2023 could be too high, especially if any recession is a deep one, but the market seems to be ahead of analysts in terms of pricing that in.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts

“A recession may not be the surprise many think it to be, at least from a share price perspective, and if we get an alternative outcome – such as stagflation, inflation and stickier-than-expected interest rates – the UK equity market’s charms may become more apparent. This could indeed be the lesson from 2022 when the FTSE 100 hung in there

“Admittedly, consensus forecast earnings growth of 9% for 2023, alongside 8% dividend growth, may not set everyone’s pulse racing. But there is the potential for upside to those estimates, especially as the slant of earnings towards oils, miners and banks means the FTSE 100 may be one of the indices that is better suited to an inflationary or stagflationary out-turn which could mean interest rates stay a bit higher for a bit longer than expected and that yield curve turn out steeper than expected.

| Percentage by sector for total FTSE 100, 2023E consensus forecasts | ||||

| Pre-tax profit | Dividends | |||

| Oil & Gas | 24% | Financials | 23% | |

| Financials | 23% | Consumer Staples | 18% | |

| Mining | 16% | Mining | 16% | |

| Consumer Staples | 12% | Oil & Gas | 12% | |

| Industrial goods & services | 7% | Health Care | 8% | |

| Health Care | 6% | Industrial goods & services | 8% | |

| Consumer Discretionary | 5% | Consumer Discretionary | 6% | |

| Utilities | 3% | Utilities | 4% | |

| Telecoms | 2% | Telecoms | 4% | |

| Real estate | 1% | Real estate | 1% | |

| Technology | 0% | Technology | 1% |

Source: Marketscreener, consensus analysts’ forecasts

“That would again contrast with markets like the USA, which is packed with tech, social media, internet and biotech stocks that offer the prospect of long-term earnings growth from the starting point of high valuation multiples. The package remains one of jam tomorrow at high prices, a combination which proved ill-suited to 2022’s environment – an environment which investors believe to be the aberration rather than the new normal.

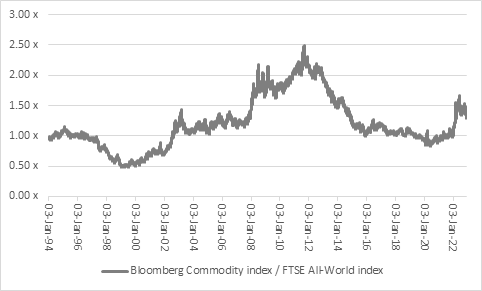

“Equities have rallied of late, and commodities have lagged, owing to the narratives that a recession is coming and that rate cuts will follow as inflation eases. But should inflation – or stagflation – prevail, commodities and ‘real’ assets could yet exert a stronger pull than ‘paper’ ones and although commodities have outperformed for the last two years, their relative strength compared to equities is nowhere near as great as it was during 2008-10 when faith in paper assets and central banks was also at a low ebb.”

Source: Refinitiv data