The impact of the Pension Freedoms

However, since the pension freedoms were introduced in 2015, few people now buy an annuity, choosing instead to draw their pension as cash, or invest it to produce an income. Prior to this liberating legislation, around 90% of retiring pension savers bought an annuity. But data from the FCA shows that in 2020/21, only 10% of retiring investors bought an annuity. So there has been a dramatic shift in the retirement market, which should have prompted a radical rethink in pre-retirement investment strategies. It did, and most providers have updated their pre-retirement de-risking options for new pension plans.

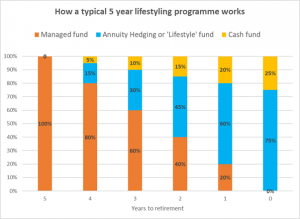

But problematically, pension plans that were set up ten, twenty, maybe even thirty years ago, can’t simply be switched across to a new investment strategy without the pension investor making an active decision to do so. Lifestyling is an automatic process, set in train many years ago, which starts switching pension savers out of a managed fund into an annuity hedging fund in the five to ten years before retirement (see example in the chart below).

We estimate there are around 850,000 pension investors who currently hold one of these lifestyling funds, based on the amount of money held in these funds (£15 billion, source: Morningstar), and the average Defined Contribution pension pot of 55 to 64 year olds (£35,000, source: ONS), and the simplifying assumption that the typical pension saver in one of these funds will have 50% of their pension pot invested. That number doesn’t include people who might have a lifestyling programme sitting patiently in the background, waiting for them to hit 55, or 60 years of age, and then starting to shift them into annuity-hedging funds.

Most of these people will have been automatically invested in a default strategy which includes lifestyling when they signed up to their pension many years ago, so few would have made an active decision to invest in this way. This strategy was most common in insurance company workplace personal pension plans, and individual Stakeholder pension plans (which effectively came with a government stamp of approval). The result is that many of the people invested in these annuity hedging funds probably don’t even know it, and they could be sleepwalking into a bond market sell off.

So why is this an issue now?

This hasn’t caused a big problem in the seven years since the Pension Freedoms were introduced because UK bond yields have fallen over this period, thanks to the Bank of England cutting interest rates in the wake of Brexit and the pandemic. In the five years after the pension freedoms were introduced in April 2015, the benchmark 15 year gilt yield fell from 2% to 0.5%, and as a result, the average lifestyle fund rose by 37% between April 2015 and April 2020 (Sources: Refinitiv and Morningstar). Few people were buying an annuity with their pension in this period, but no-one felt out of pocket because they were still banking a healthy return on their money.

![[uns] office, appointment, staff](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/787084-featured-300x200.webp)

![[UNS] tax](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/787063-featured-300x200.webp)