By Daniel Gerard, Senior Multi – Asset Strategist, State Street Global Markets

Financials preferences changing through earnings season

As we make our way through the second full week of US earnings season, about a third of all the companies that have reported so far have been Financials. We’ve seen a few trends develop over this period when scanning through company reports, and it’s been clear that a lot of the earnings surprise has come from either better expected trading volumes or challenging environments for fee and NII that still persist. We’ve also seen a bit of steepening of the yield curve due mostly to a falling short end with a relatively stable long end versus the prior month. This rate and EPS environment has created a sea of change in institutional investor flow trends as we progressed through the month. The selling of Insurance was short-lived and we’re seeing a strong return to buying, selling of banks has subsided, and buying of Financial Services, dominated by the payments sector, has started to fade, perhaps on worries of consumer spending headwinds.

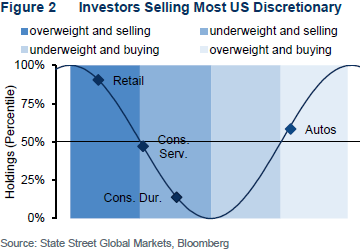

Discretionary groups under pressure

In that same vein, institutional investors have also become much more sour on the industry groups within the Discretionary space. Long-only funds are now net-sellers of nearly every piece of Consumer Discretionary save Autos, and even in the Autos space, flows are fading fast. The largest overweight is in Retail, dominated by one company of course, but the message is that the coincident selling of this part of consumer world alongside the selling of the payment processers tells us a bit more about how institutions expect the first quarter to develop as we wait to see more on rates policy as well as tariff policy out of the new Trump administration.

US inflation flashes a spark in the new year

December inflation trends were dominated by a slowing trend in price growth, something which came through on CPI and emboldened market participants, if only slightly, to become a bit more dovish on potential Fed policy. Yet as we progress through the first few weeks of January, the slowing trend has sharply reversed. Our US PriceStats metrics have noted a steady increase in the daily rolling level of MoM price changes, now approaching 0.3%. A primary driver of this change has come from the Recreation sector; we’re seeing a quick reversal in the trend in prices here, which have now reached over 1% MoM. As much as we saw December’s data ease concerns, the question remains as to whether that will be repeated when official data is released in a few weeks.

![[UNS] celebrate](https://ifamagazine.com/wp-content/uploads/wordpress-popular-posts/801986-featured-300x200.webp)