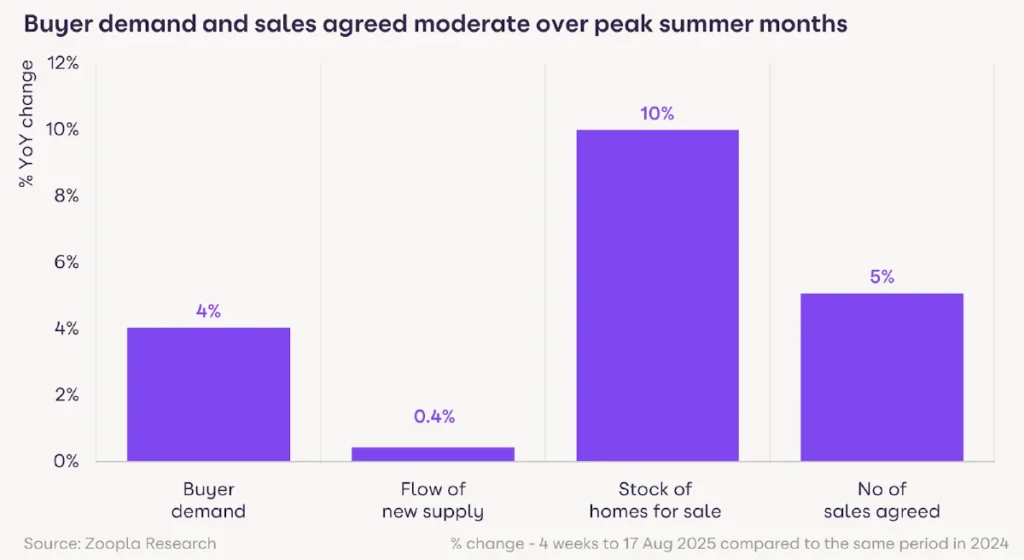

Activity in the housing market has seen continued growth over the last 12 months, according to Zoopla’s latest House Price Index1. More sales are being agreed (five per cent), but buyer demand is higher (four per cent) resulting in it remaining a buyers market, although this varies across the country. Those looking to sell over the upcoming autumn selling season need to price their homes correctly, while recent tax speculation may have a short term impact on homes valued at over £500,000.

The pace of house price growth has slowed over recent months, due to buyers having greater choice of homes for sale (10 per cent more than last year) and affordability being a continued constraint on buying power, especially across Southern England.

However, the slowdown looks to have stabilised, with average house prices 1.3 per cent higher over the last year. This is below the 2.1 per cent price growth recorded at the start of 2025, but higher than 0.6 per cent this time last year. The average UK house price is £270,600, £3,560 more than a year ago2.

Table 1: Buyer demand and sales agree moderate over peak summer months

Property tax speculation creates uncertainty for a third of home buyers

Media speculation over possible tax changes, including the removal of stamp duty and its replacement with an annual property tax for homes over £500,000, and a requirement for sellers of homes over £1.5m to pay capital gains tax, has attracted a lot of interest. The risk is that this creates uncertainty for home buyers in the coming weeks ahead of the Autumn Budget. History shows that tax changes can impact market activity and buyer expectations.

Speculation over the removal of stamp duty replaced by a new annual property tax for homes over £500,000 may make some buyers consider a ‘wait and see’ strategy. This covers those who may possibly save money on purchases under £500,000 and concern those buying over this level as well. A third of homes for sale are over £500,000, with the impact felt more keenly in London and the South East where home values are higher.

Capital gains are not taxed on main residence sales but do apply to second home owners and landlords. Just four per cent of homes for sale are over £1.5m but speculation about possible taxation of capital gains may impact buyer decisions at this end of the market in the short term.

Homes priced too high take twice as long to sell

The time a property stays on the market is a key indicator of housing market health and is directly linked to house price inflation. In northern regions, a combination of fewer homes on the market than a year ago and better affordability is leading to quicker sales times. For example, the average time to sell a home in the North West and North East of England in July was 27 days, 23 per cent faster than the national average of 35 days. This is helping fuel above average house price growth in these areas which is sitting at 2.7 per cent and 2.1 per cent respectively.

Table 2: Time to sell by region across England and Wales

| Area | Time on market to sold subject to contract (days) | Annual price change (%) |

| N West | 27 | 2.7% |

| N East | 27 | 2.1% |

| Yorks’ & H | 32 | 2.0% |

| W Mids | 34 | 1.8% |

| Wales | 34 | 2.1% |

| E Mids | 38 | 1.3% |

| Eastern | 38 | 0.7% |

| S West | 38 | 0.3% |

| London | 39 | 0.5% |

| S East | 40 | 0.3% |

| England & Wales | 35 | 1.3% |

Source: Zoopla Research 2025

In contrast, regions across southern England are experiencing a stronger buyer’s market. The supply of homes for sale is higher than a year ago while higher house prices create affordability problems that have extended the time it takes to agree a sale to an average of 39 days in July. This is 11 per cent longer than the national average. Longer sales times are creating less pressure on house prices in the south, where house price growth sits as low as 0.3 per cent in the South East and South West.

While a home’s presentation and local market conditions are important factors behind sales times, getting the asking price wrong for the local market can impact levels of buyer interest. Homes that need to reduce their asking price to attract more interest take, on average, 2.4 times longer to sell than those that do not need a price reduction. This extended time on the market from listing to an agreed sale is in addition to the four to six months it takes for a sale to usually complete (subject to contract).

Sellers need to be cautious in slower markets where competition is high

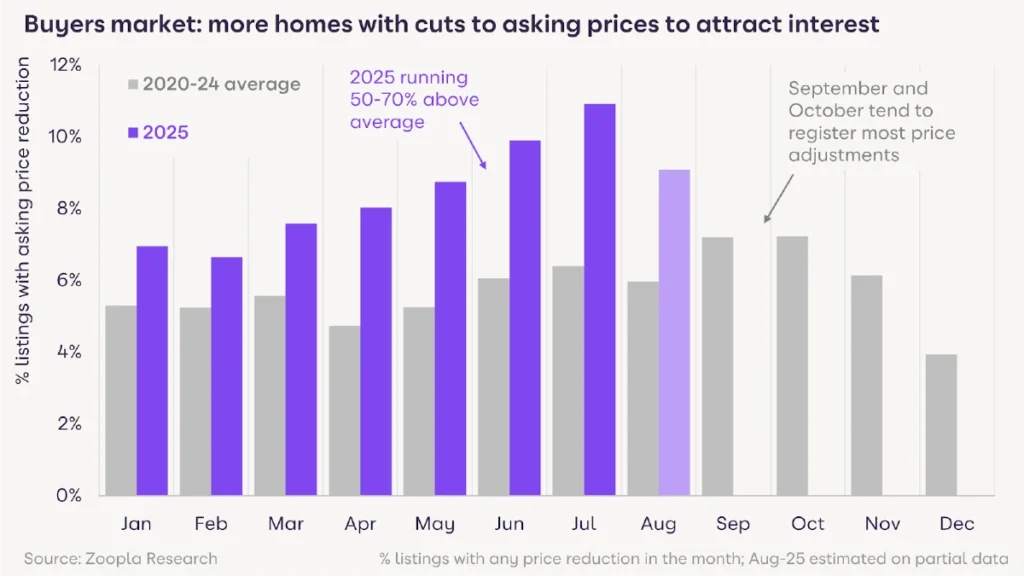

Market conditions have softened since the end of the stamp duty holiday in March. As a result, there has been a steady increase in the proportion of homes for sale with asking price reductions to try and attract buyer interest. In July, one in ten homes registered a cut to the asking price, well above the five-year average of six per cent, a further indication of why house price growth has slowed in recent months.

Table 3: Buyers market: more homes with cuts to asking prices to attract interest

Analysis of markets with the most unsold homes shows that coastal areas across southern England have the most competition among sellers. In Truro, Exeter, and Bournemouth, more than a quarter of homes for sale have been on the market for over six months, more than a third higher than the average. This increased choice, a result of a larger number of second homes for sale in response to higher council tax, is also impacting prices, which are 1.1 per cent and 1.4 per cent lower than a year ago in these markets.

Other areas with an above-average stock of unsold homes include York, Torquay, and Llandrindod Wells in Wales, markets where sellers need to be most realistic on price if they want to sell this year. In contrast, there are markets with a lack of supply, including Dundee, Wolverhampton, outer suburbs of London, and Northampton.

Commenting on the report, Richard Donnell, Executive Director at Zoopla, said: “There is plenty of demand for homes and more people are looking to move. However, buyers also have much greater choice to choose from, especially across areas of southern England. There is a clear link between buyer choice and price inflation and how long it is taking homes to sell.

“Sellers need to understand local market conditions when considering how to market their home, setting the right price and how quickly they would like to sell. The risk of being too ambitious on price is your home taking more than twice as long to find a buyer – or not selling at all.

“We expect UK house price inflation to continue in a range of 1.5-2 per cent over the rest of the year. There are signs that prices are firming in southern England but price growth is slowing across northern regions. The market continues to record seasonally strong sales as those selling their home seek to secure their next home. The market remains on track for five per cent more sales in 2025 at 1.15m.”

Stuart Bailey, head of London super-prime sales at Knight Frank, said:

“Good advice around not just pricing but strategy, from experienced professionals, has never been more important. The autumn market is about to begin and this year will be shrouded by speculation of how to decipher the government’s messaging on property tax. Either way, sentiment impacts decision making and the longer a property takes to sell (if mis-priced for example), the bigger the risk of something going wrong, as buyers become ever more hesitant, and the risk of market slow down increases.”

Nathan Emerson, CEO of Propertymark, said:

“Stable house prices within the housing market are a welcome sign for groups such as first-time buyers, who can better take advantage of a period of steadiness. Despite property transactional taxes increasing in some nations and financial and economic pressures continuing for many, there still seems to be plenty of property choice for buyers. It remains important that sellers continue to have realistic price expectations and place their property on the market accordingly to help empower an efficient sales process.

“It is also important to consider the crucial role that housing plays within the wider economy, and it is positive to see commitments from all governments across the UK to deliver much-needed new housing stock to keep pace with predicted population growth. We are also hearing of future potential proposed changes regarding Stamp Duty. However, it is vital that tax reform is conducted in a way that does not penalise aspiring homeowners with additional costs that hinder their chances of moving house.”